Fitbit remains one of the most recognized names in digital health and fitness tracking. Millions of people use Fitbit devices to monitor activity levels, sleep quality, heart rate, and overall wellness, while employers and healthcare organizations increasingly rely on wearable data to support wellness programs and preventive care initiatives. As the wearable technology market expands and health tracking becomes more personalized, Fitbit’s performance offers valuable insights into changing consumer behavior and the future of connected health. Explore the statistics below to understand how Fitbit continues to shape the global wearable industry.

Editor’s Choice

- Fitbit generated an estimated $770 million in revenue in 2025, down 15.3% from the previous year.

- Fitbit had approximately 33 million active users worldwide in 2025.

- The platform recorded nearly 128 million registered users in 2023, adding around 8 million new registrations in one year.

- Fitbit has sold more than 143 million devices globally since its launch.

- The Fitbit app has surpassed 50 million downloads on Google Play.

- Fitbit enjoys 73% brand awareness among U.S. wearable users, making it one of the most recognized fitness-tracking brands.

- The global fitness tracker market is projected to reach $84.68 billion in 2026, creating significant opportunities for Fitbit and other wearable brands.

Recent Developments

- In 2026, Google announced plans to transition the Fitbit app into the broader Google Health ecosystem.

- Google introduced Google Health Coach, previously known as Fitbit Coach, to strengthen personalized wellness offerings.

- The wearable fitness technology market reached $16.12 billion in 2025 and is forecast to exceed $51 billion by 2035.

- The global fitness tracker industry is projected to expand at a 27.5% CAGR through 2034, signaling strong demand for health-monitoring devices.

- Sensors accounted for approximately 22% of wearable technology revenue in 2025, highlighting the growing importance of health-monitoring capabilities.

- Around 80% of fitness apps share data with third parties, increasing industry focus on privacy and security standards.

- North America represented 41% of the global wearable fitness technology market in 2025, remaining Fitbit’s largest addressable market.

- The U.S. wearable market generated approximately $21.8 billion in revenue during 2025.

- Smartwatches became the preferred wearable category for 75% of users globally in 2023, increasing competitive pressure on Fitbit’s smartwatch lineup.

Overview and Company Facts of Fitbit

- Fitbit was founded in 2007 by entrepreneurs James Park and Eric Friedman.

- Google completed its acquisition of Fitbit in January 2021, integrating the company into its hardware division.

- Fitbit devices are available in more than 100 countries worldwide.

- The company has shipped over 120 million devices globally, according to industry estimates.

- Fitbit was the fifth-largest wearable technology company by shipments in 2019.

- More than 20 million users engaged with Fitbit Feed, the platform’s social feature, during its peak growth period.

- Fitbit users have joined community groups more than 4.7 million times, demonstrating strong engagement with social wellness features.

- Fitbit’s app was once the No. 1 health and fitness application on both iOS and Android in the United States.

- Fitbit’s product portfolio spans fitness bands, smartwatches, sleep trackers, and health-monitoring services.

Global Fitness App Market Size Statistics

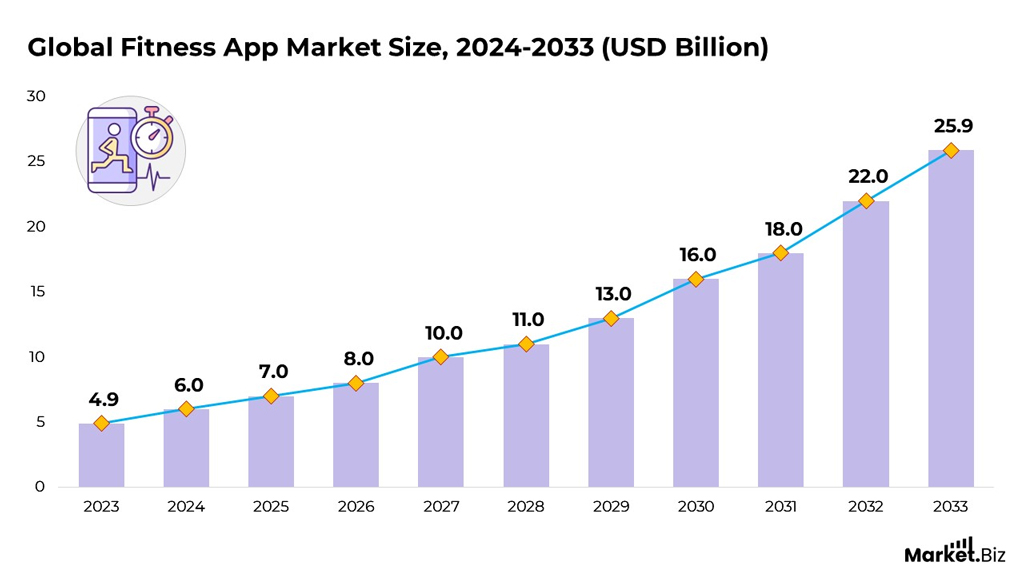

- The global fitness app market was valued at $4.9 billion in 2023.

- The market is projected to grow to $6.0 billion in 2024, reflecting steady expansion.

- By 2025, the global fitness app market is expected to reach $7.0 billion.

- Market value is forecast to increase to $8.0 billion in 2026.

- The industry is expected to surpass $10.0 billion in 2027.

- The market is projected to grow further to $11.0 billion in 2028.

- By 2029, the global fitness app market is estimated to reach $13.0 billion.

- The market is forecast to hit $16.0 billion in 2030, marking strong long-term growth.

- Global fitness app market size is expected to climb to $18.0 billion in 2031.

- The market is projected to exceed $22.0 billion in 2032.

- By 2033, the global fitness app market is forecast to reach $25.9 billion, the highest value in the period shown.

- Overall, the market is expected to grow by approximately 5.3× from $4.9 billion in 2023 to $25.9 billion in 2033.

Device Sales and Unit Shipments of Fitbit

- Fitbit has sold more than 143 million wearable devices worldwide since launch.

- Industry estimates also place lifetime Fitbit device shipments above 120 million units globally.

- Fitbit shipped millions of devices annually during its peak years and remained among the world’s top wearable vendors.

- Global shipments of smartwatches and fitness trackers are projected to reach approximately 524 million units, reflecting a rapidly expanding market.

- Fitbit’s estimated global shipment share stood at around 6.2% in the wearable industry.

- The company lost its market leadership position as larger technology firms expanded aggressively into health wearables.

- The fitness tracker market is expected to exceed $204 billion by 2034, creating long-term shipment opportunities.

- The smartwatch segment has become the industry’s dominant category, accounting for the preferences of 75% of wearable users.

- Demand for advanced health sensors and AI-powered tracking features continues to support new device sales across the wearable industry.

Revenue and Financial Performance of Fitbit

- Fitbit generated an estimated $770 million in revenue during 2025.

- The company’s revenue declined by approximately 15.3% year over year in 2025.

- Despite slowing hardware sales, Fitbit continues to benefit from subscription services and software integration within Google’s ecosystem.

- The global fitness tracker market reached $72.08 billion in 2025, providing a substantial revenue opportunity for wearable companies.

- The wearable fitness technology market is expected to surpass $51.43 billion by 2035, reflecting sustained industry expansion.

- The United States generated around $21.8 billion in wearable revenue during 2025, reinforcing Fitbit’s importance in the U.S. market.

- The wearable fitness technology market is projected to grow at a 12.3% CAGR between 2026 and 2035.

- The broader fitness tracker market is expected to grow at a 27.5% CAGR through 2034, creating favorable conditions for future Fitbit monetization.

- Increasing demand for preventive healthcare and remote monitoring continues to support investment in wearable technologies and digital health services.

Registered Users and Active User Counts of Fitbit

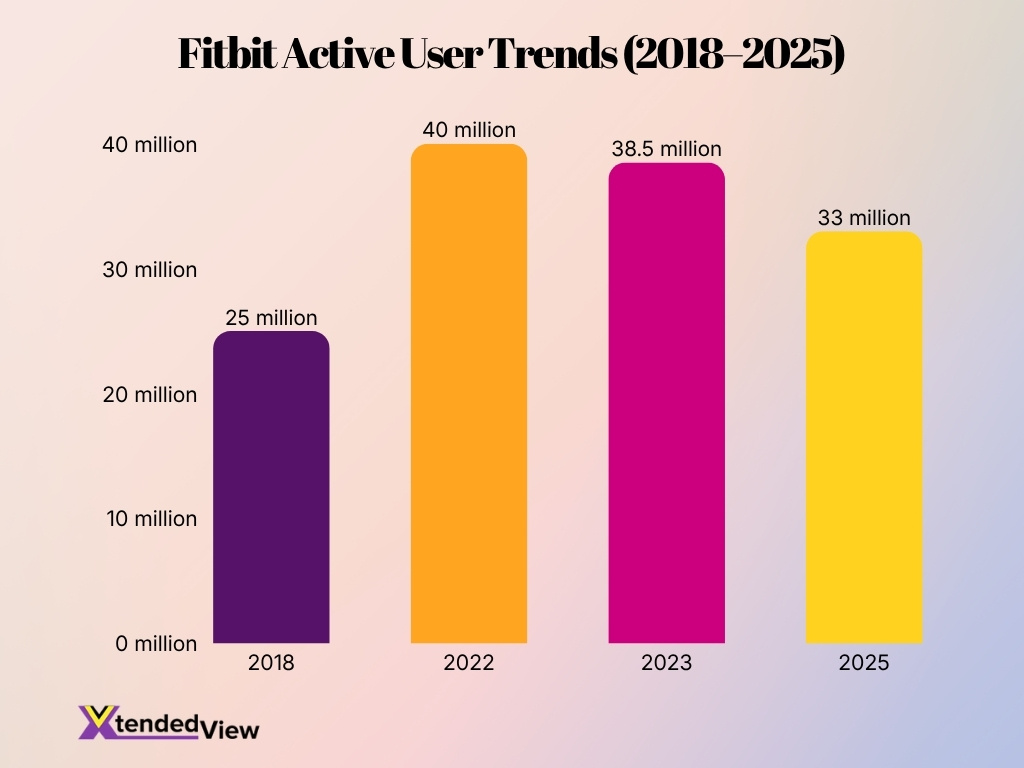

- Fitbit had approximately 128 million registered users in 2023, up from around 120 million in 2022.

- The platform reported roughly 38.5 million active users in 2023.

- Active users declined from 40 million in 2022 to 38.5 million in 2023, reflecting increased competition in wearables.

- Business estimates suggest Fitbit maintained around 33 million active users during 2025.

- Earlier company data showed the Fitbit community surpassed 25 million active users in 2018, indicating substantial long-term growth.

- More than 20 million users actively participated in Fitbit Feed discussions and challenges.

- Fitbit remains among the most downloaded health applications with over 50 million Android downloads.

- Millions of users continue to use Fitbit’s ecosystem despite increasing competition from smartwatches and health platforms.

- Fitbit’s registered-user base has increased by more than 10 times since the mid-2010s, highlighting sustained consumer interest in wearable health monitoring.

Market Share and Competitive Ranking of Fitbit

- Fitbit held an estimated 6.2% share of the global wearable device market in 2025, ranking behind Apple, Huawei, and Xiaomi.

- Fitbit was the fifth-largest wearable vendor globally before Google’s acquisition and remains among the top fitness-tracking brands by user recognition.

- Apple accounted for approximately 22% of global wearable shipments in 2025, making it Fitbit’s largest competitor.

- Xiaomi captured nearly 16% of the global wearable market in 2025, intensifying competition in the affordable fitness band segment.

- The smartwatch category represented nearly 75% of wearable device sales in 2025, reducing demand for basic fitness trackers.

- Fitbit’s U.S. brand awareness reached 73% among wearable users, placing it among the most recognized health technology brands.

- The global wearable market shipped more than 534 million units in 2025, creating a highly competitive environment for Fitbit and its rivals.

- Fitbit continues to maintain a strong position in health-focused wearables due to its emphasis on sleep monitoring, stress tracking, and wellness insights.

- Industry analysts expect health-centric wearables to gain market share through 2030 as consumers increasingly prioritize preventive healthcare technologies.

Geographic Distribution of Fitbit Users

- The United States remains Fitbit’s largest market, accounting for approximately 45% of the company’s active user base.

- North America represented 41% of the global wearable technology market in 2025, benefiting Fitbit’s regional performance.

- Europe contributes an estimated 25% of Fitbit’s global user base, making it the company’s second-largest market.

- The United Kingdom consistently ranks among Fitbit’s strongest markets due to high adoption of fitness trackers and corporate wellness programs.

- Asia-Pacific generated nearly 30% of global wearable revenue in 2025, presenting long-term growth opportunities for Fitbit.

- The Middle East and Africa collectively accounted for less than 5% of Fitbit’s estimated users, although adoption rates continue to improve.

- More than 100 countries currently have access to Fitbit products and services.

- Countries with high smartphone penetration and increasing healthcare awareness continue to drive Fitbit’s international growth.

- Demand for wearable health technology has accelerated across emerging markets due to rising interest in preventive health monitoring.

Demographics of Fitbit Users

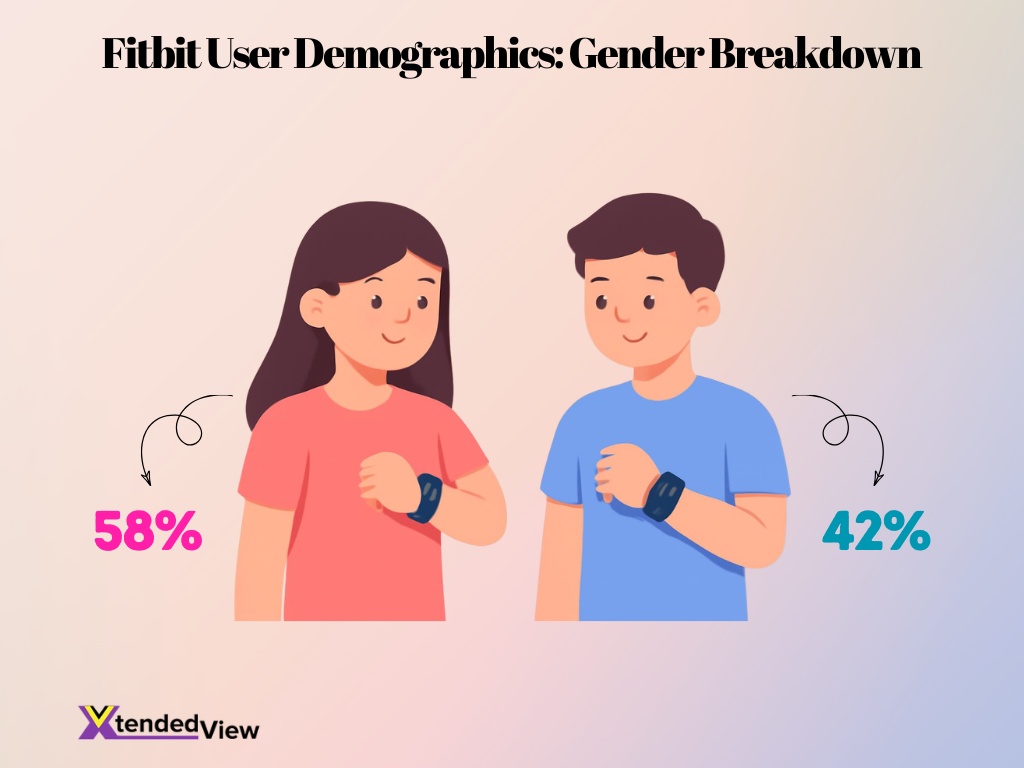

- Approximately 58% of Fitbit users are women, while men account for about 42% of users.

- Adults between 25 and 44 years old represent nearly half of Fitbit’s user base, making millennials the platform’s largest demographic group.

- Around 70% of Fitbit users have a college degree, indicating strong adoption among educated consumers.

- More than 60% of Fitbit users report annual household incomes above $50,000, reflecting the purchasing power of wearable consumers.

- Consumers aged 18 to 34 years are the fastest-growing segment for smartwatch adoption globally.

- Approximately one in three Fitbit users owns multiple connected health devices, including smart scales and smartwatches.

- Fitbit usage among adults over 55 years old has steadily increased due to growing interest in heart health and sleep monitoring.

- Parents increasingly purchase Fitbit devices for children and teenagers to encourage healthy activity habits.

- Health-conscious professionals and office workers remain one of Fitbit’s largest customer segments because of sedentary lifestyle concerns.

Daily Usage and Engagement Metrics of Fitbit

- Fitbit users open the app an average of 4 to 5 times per day to review health metrics.

- More than 70% of active users sync their devices at least once daily.

- Users collectively log billions of activity minutes on the platform every month.

- Approximately 80% of Fitbit owners use at least 1 health-tracking feature every day.

- The average Fitbit user checks their sleep data at least 3 times per week.

- Millions of users participate in community challenges on an annual basis.

- Device engagement consistently rises during the first 6 months of ownership before stabilizing.

Average Steps and Activity Levels of Fitbit Users

- Fitbit users average approximately 8,500 steps per day globally, exceeding the worldwide average for adults.

- U.S. Fitbit users typically record between 7,500 and 8,000 daily steps.

- Users participating in Fitbit challenges walk roughly 2,000 additional steps per day compared with nonparticipants.

- Fitbit’s internal studies found that users who receive reminders to move increase daily activity by approximately 9%.

- The average active Fitbit user logs more than 250 minutes of exercise per month.

- Walking remains the most frequently tracked activity, accounting for more than 60% of recorded workouts on Fitbit devices.

- Users who regularly monitor activity data are more likely to achieve the recommended 150 minutes of weekly exercise.

- Corporate wellness participants using Fitbit devices report higher daily step counts than non-users.

- Fitbit data has supported hundreds of research studies examining physical activity and long-term health outcomes.

Feature Adoption Trends Among Fitbit Users

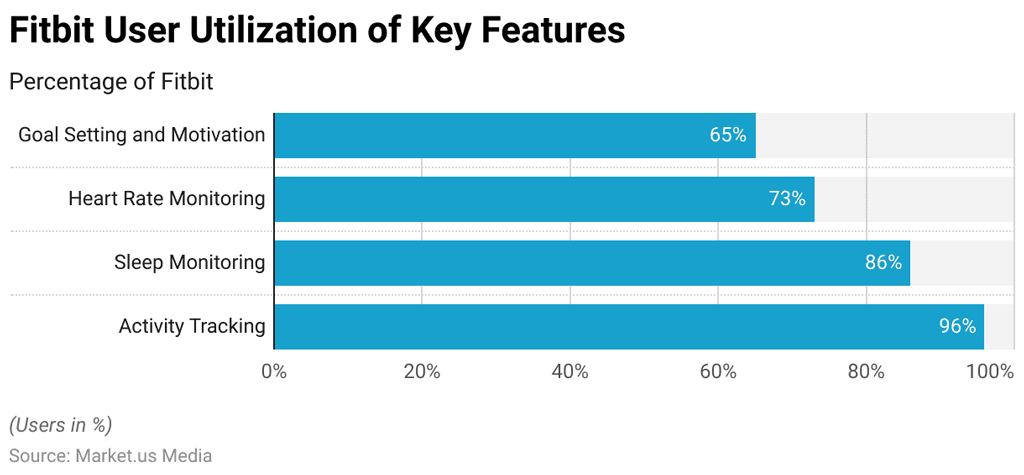

- Activity Tracking is the most widely used Fitbit feature, with 96% of users relying on it.

- Sleep Monitoring is used by 86% of Fitbit users, making it the second most popular feature.

- Heart Rate Monitoring is utilized by 73% of users for continuous health tracking.

- Goal Setting and Motivation features are used by 65% of Fitbit users to support fitness goals.

- The gap between the most-used and least-used features is 31 percentage points (96% vs. 65%).

- More than 7 in 10 users actively use Fitbit’s Heart Rate Monitoring feature.

- More than 8 in 10 users take advantage of Fitbit’s Sleep Monitoring capabilities.

- Nearly all Fitbit users (96%) engage with Activity Tracking, highlighting it as the platform’s core feature.

Heart Rate and Health-Tracking Statistics of Fitbit

- Fitbit devices have logged over 149 billion hours of heart-rate data from more than 10 million global users.

- A novel Fitbit algorithm accurately identified undiagnosed atrial fibrillation with a 98.2% positive predictive value.

- The large-scale Fitbit Heart Study monitored 455,669 adults and detected irregular heart rhythms in 1% of participants.

- Research using Fitbit data shows the optimal daily sleep duration for a healthy resting heart rate is exactly 7.25 hours.

- Fitbit users who complete at least 250 minutes of exercise weekly maintain significantly lower resting heart rates.

- Fitbit’s health-tracking ecosystem supported approximately 33 million active users and 137 million registered users in 2025.

- Analysis of user data reveals that heart rate variability (HRV) drops by up to 18% during major winter holidays.

- Fitbit insights show that average daily activity drops by 1,500 to 1,750 steps on holidays compared to yearly averages.

Sleep Tracking Statistics of Fitbit Users

- Fitbit users have logged more than 22 billion nights of sleep data since the company introduced sleep tracking.

- The average Fitbit user sleeps approximately 6 hours and 58 minutes per night, according to aggregated platform data.

- Women generally record 11 to 15 minutes more sleep per night than men using Fitbit devices.

- Users aged 55 and older report the highest sleep consistency scores among Fitbit age groups.

- Sleep tracking ranks among the top three most-used Fitbit features, alongside step counting and heart-rate monitoring.

- More than 40% of Fitbit users check their sleep score every morning.

- Sleep analytics have become increasingly important as consumers focus on stress reduction and mental wellness.

- Fitbit’s Sleep Score feature combines heart rate, restlessness, and sleep duration into a single daily metric.

- Research using Fitbit sleep data has helped scientists study sleep disorders, recovery patterns, and population health trends.

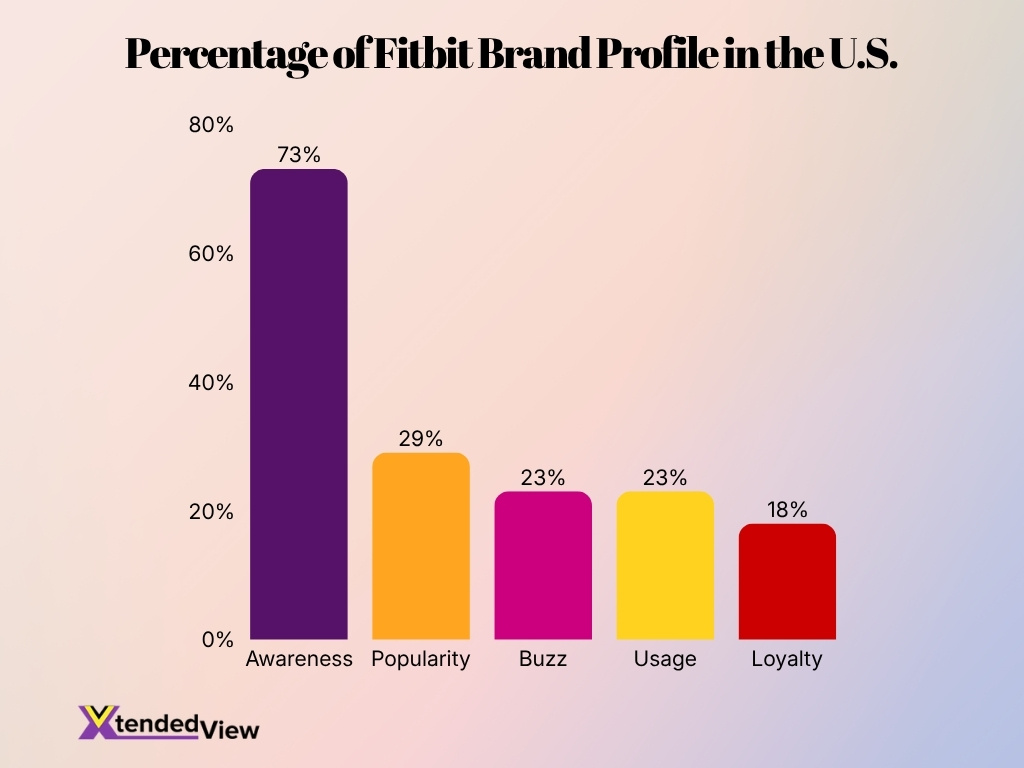

Fitbit Brand Profile Statistics in the U.S.

- Fitbit brand awareness is the highest metric, with 73% of U.S. consumers recognizing the brand.

- Popularity stands at 29%, making it the second strongest brand profile metric.

- Buzz reaches 23%, indicating a moderate level of consumer interest and discussion.

- Usage also measures 23%, showing that nearly one in four consumers actively use Fitbit products.

- Brand loyalty is the lowest metric at 18%, suggesting room for improvement in customer retention.

- The gap between awareness (73%) and usage (23%) highlights that many consumers know the brand but do not use its products.

- Fitbit’s popularity exceeds both usage and buzz by 6 percentage points, reflecting a stronger public perception than active engagement.

- With awareness more than four times higher than loyalty, Fitbit has a significant opportunity to strengthen long-term customer relationships.

Fitness and Workout Statistics of Fitbit Users

- Walking remains the most popular activity, accounting for more than 60% of all logged exercises.

- Users collectively record billions of exercise sessions every year across various disciplines.

- Fitbit challenge participants complete approximately 27% more active minutes than nonparticipants.

- Users average about 250 active minutes per month, exceeding public health recommendations.

- Running is highly popular and ranks among the top 5 tracked activities.

- More than 40 exercise modes are available across smartwatches and trackers.

- Consistent tracking makes users significantly more likely to maintain habits for at least 6 months.

- Strength training and HIIT are the two fastest-growing exercise categories since 2023.

- Wearables and fitness apps remain among the top global fitness trends for 2026.

Wear Time and Retention Rates of Fitbit Devices

- Fitbit users wear their devices for an average of 14 hours per day according to aggregated usage studies.

- More than 70% of Fitbit owners continue using their devices six months after purchase, outperforming many consumer electronics categories.

- Approximately 50% of users remain active after one year, indicating relatively strong retention for wearable devices.

- Fitbit users who engage with sleep tracking and heart-rate monitoring demonstrate higher retention rates than users who only track steps.

- Users participating in community challenges are more likely to remain active on the platform long term.

- Daily syncing behavior strongly correlates with device retention and continued engagement.

- Consumers who subscribe to Fitbit Premium are significantly more likely to continue using their devices after the first year.

- The wearable industry still faces retention challenges, as many consumers abandon fitness trackers within the first year of ownership.

- Personalized insights and health analytics have become key drivers of long-term Fitbit device usage.

App Downloads and Platform Usage of Fitbit

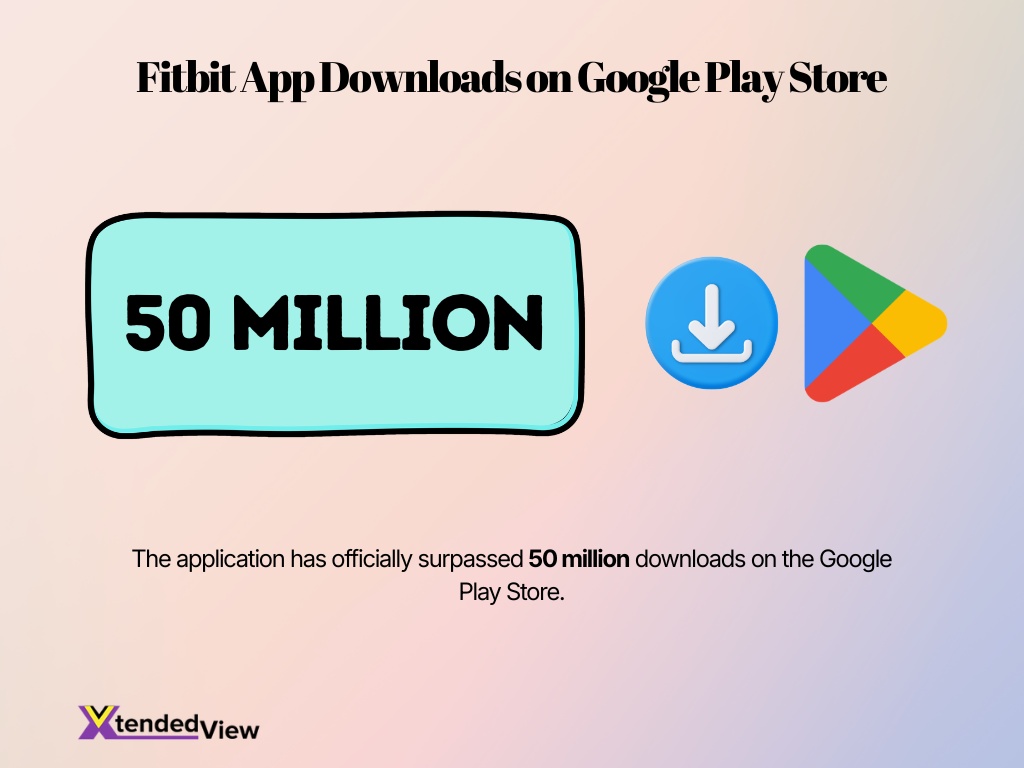

- The application has officially surpassed 50 million downloads on the Google Play Store.

- The platform maintains a highly engaged global audience with over 38 million monthly active users.

- A significant 128 million registered users have joined the Fitbit ecosystem globally as of 2023.

- User demographics indicate that 25.93% of active consumers fall within the 25 to 34 age bracket.

- Engagement metrics show that 86% of users actively rely on the platform to monitor their sleep patterns.

- Approximately 72.87% of consumers utilize the application primarily for heart rate monitoring and cardiovascular insights.

- The platform’s motivational tools drive retention, with 65% of users actively setting personal fitness goals.

- During peak digital health adoption, the application successfully reached a record 40.2 million active users.

- Social engagement significantly boosts activity, with users in peer challenges showing 30% higher retention rates.

- In the highly competitive United States market, the platform secured a 16% market share in 2025.

Subscription and Premium Service Metrics of Fitbit

- Fitbit Premium reached over 500,000 paid subscribers in under a year after its August 2019 launch.

- The consumer services division achieved an annual revenue run-rate exceeding $100 million in Q3 2020.

- New Premium users demonstrated high engagement by taking an average of 700 more steps per day.

- Consumer services revenue driven by Premium subscriptions grew by an impressive 607% year-over-year in 2020.

- The global digital fitness app market is projected to reach $22.0 billion by 2032 with an 18% growth rate.

- The overarching Fitbit health application surpassed 50 million global downloads on Android in 2023.

- Google expanded its health ecosystem by finalizing its acquisition of Fitbit for $2.1 billion in 2021.

- The Fitbit digital ecosystem recorded a massive active community of 38.5 million monthly active users in 2023.

Enterprise and Corporate Wellness Usage of Fitbit

- Fitbit has partnered with over 2,000 employers for their corporate wellness initiatives.

- Over 2.6 million employees seamlessly integrate their wearable data into health management platforms.

- Wearable-supported workplace wellness initiatives can increase daily activity by 1,000 to 2,500 steps.

- Investing in corporate wellness programs yields a $3.27 return on investment per dollar spent.

- Employees enrolled in Fitbit programs incur 24.5% less in annual healthcare costs than non-participants.

- The global corporate wellness market is projected to rapidly exceed $100 billion by 2030.

- Implementing wearable wellness technology reduces employee workplace absenteeism by 25% on average.

- The overall adoption of wearable devices in corporate wellness has grown by 25% since 2021.

Frequently Asked Questions (FAQs)

Fitbit had approximately 33 million active users worldwide in 2025, down about 8.3% from the previous year.

Fitbit has sold more than 143 million devices worldwide since its launch in 2009.

Fitbit generated an estimated $770 million in revenue in 2025, representing a year-over-year decline of roughly 15%.

Fitbit holds approximately 18.7% of the U.S. fitness tracker market, making it the second-largest brand in the country behind Apple.

The global fitness tracker market is projected to reach $84.68 billion in 2026 and grow at a 24.43% CAGR through 2034.

Conclusion

Fitbit remains one of the most influential companies in the wearable health industry despite intensifying competition from larger technology brands. The platform continues to serve millions of active users, generate hundreds of millions of dollars in annual revenue, and maintain strong recognition in the United States and other major markets.

The company’s focus has shifted beyond step counting toward comprehensive health monitoring that includes sleep analysis, heart health, stress management, and personalized wellness recommendations. At the same time, corporate wellness programs, subscription services, and digital health integrations are creating new opportunities for long-term growth.

As the global wearable technology market expands, Fitbit’s extensive health data ecosystem and connection to Google’s broader healthcare ambitions position the brand to remain a significant player in the future of connected health and preventive care.