Robotic surgery has shifted from fringe innovation to mainstream practice in hospitals worldwide. By combining surgeon expertise with machine precision, robotic-assisted procedures are reducing recovery times, lowering complication rates, and pushing the boundaries of minimally invasive care. In urology, prostatectomies increasingly use robotic platforms, and in general surgery, complex procedures are performed with enhanced control. As adoption rises sharply, the following article presents the latest statistics that define where the field stands and where it’s headed.

Editor’s Choice

- The global robotic surgical market is expected to reach around $13.7 billion in 2025.

- The market shows growth at a CAGR between 14.7% and 17.4% through 2032.

- Over 2,683,000 surgeries were performed with da Vinci systems in 2024.

- Worldwide da Vinci procedures grew by 18% year‑over‑year in 2024.

- More than 7,500 da Vinci systems are active globally.

- North America holds a leading 50%+ share of the global robotic surgery market.

- Adoption of robotic surgery in the U.S. is used in 15% of general surgeries, compared to much lower rates elsewhere.

Recent Developments

- Global procedures with robotic systems increased 18% in 2024 vs 2023.

- U.S. procedure volume grew by 19% in 2024 alone.

- International robotic procedures expanded by 23% in 2024.

- Newer‑generation systems (e.g., da Vinci 5) saw an 11% rise in placements in 2024 vs prior year.

- The rise in installations reflects broader demand for minimally invasive care.

- Emerging competitors are advancing platforms beyond da Vinci, particularly in niche specialties.

- Telehealth and remote‑guided surgery concepts are increasingly part of research agendas.

- AI‑enhanced robotic features under development aim to improve workflow efficiency.

Overview of statistics in robotic‑assisted surgery

- The robotic surgery market was roughly $11.8–$12.9 billion in 2024 and is expected to settle at $13.7 billion in 2025.

- Projections suggest growth to $38–$41 billion by 2032.

- Surgical procedures assisted by robots number in the millions annually.

- Da Vinci platforms alone have enabled over 14 million procedures to date.

- Adoption rates vary by region, with much higher penetration in the U.S. than in Europe.

- Robotic interventions span specialties including urology, gynecology, and cardiothoracic surgery.

- Hospitals report increased scheduling of robot‑assisted procedures year‑over‑year.

- Robotic options are increasingly factored into surgical planning due to lower complication risks.

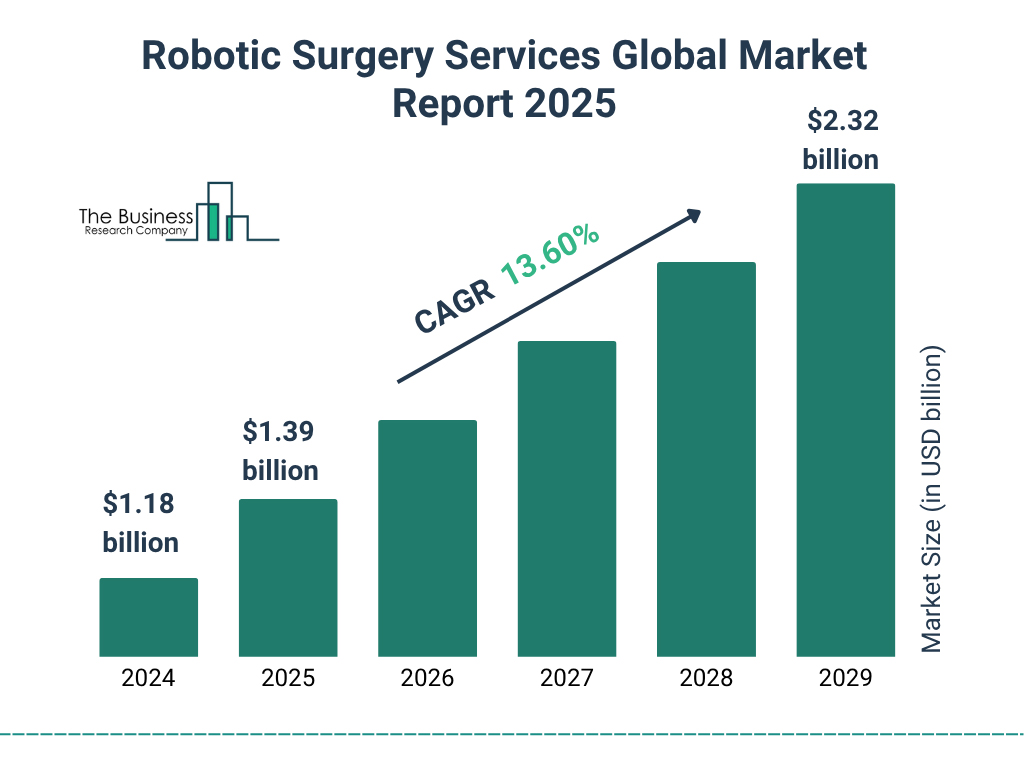

Robotic Surgery Services Global Market Growth Insights

- The global robotic surgery services market was valued at $1.18 billion in 2024, highlighting the early-stage but fast-growing nature of this healthcare segment.

- Market size increased to $1.39 billion in 2025, reflecting the rising adoption of robotic-assisted surgical procedures worldwide.

- The industry is projected to grow at a strong CAGR of 13.60% during the forecast period, indicating sustained long-term demand.

- By 2026, the market is estimated to reach approximately $1.60 billion, driven by expanding hospital investments and surgeon training programs.

- The market is expected to climb to around $1.85 billion in 2027, supported by increasing procedure volumes across multiple surgical specialties.

- In 2028, global market revenue is forecast to touch about $2.10 billion, as robotic systems become more mainstream in minimally invasive surgeries.

- The market is projected to achieve $2.32 billion by 2029, nearly doubling in value compared to 2024, underscoring robust commercial momentum.

- Continuous advancements in robotic technology, precision tools, and AI-assisted systems are key contributors to this rapid market expansion.

- Growing demand for minimally invasive procedures, shorter hospital stays, and improved patient outcomes is accelerating market growth globally.

Global trends in robotic surgical adoption

- North America dominated with over 40% of global surgical robotics revenue at $3.53 billion in 2024.

- Global da Vinci systems reached an installed base exceeding 7,500 units, with 1,526 new placements in 2024.

- U.S. robotic surgery adoption hit 15.1% of general surgical procedures across monitored hospitals.

- Europe’s robotic surgery systems market is valued at $3.76 billion in 2024, indicating 2-5% penetration.

- The Asia-Pacific robotic surgery market grew at a 19.2% CAGR from 2024, holding 23% global revenue share.

- Worldwide da Vinci procedures surged to 2.68 million in 2024, up 18% year-over-year.

- International da Vinci procedure growth outpaced the U.S. at 23% vs 19% in 2024.

- India captured 6% of the Asia-Pacific robotic surgery market share in 2024, with 71 da Vinci systems installed.

- Global robotic surgery market valued at $8.82-11.98 billion in 2024, projecting 16.54% CAGR to 2034.

- Over 73% of general surgery residencies feature formal robotic training curricula worldwide.

Growth trajectory of procedures involving robotic systems

- Worldwide da Vinci‑assisted procedures reached 2,683,000 in 2024.

- Procedure volume grew 18% in 2024 compared to 2023.

- The U.S. saw a 19% rise in its robotic surgery procedures in 2024.

- International operations increased by 23% in 2024.

- Forecasts suggest continued 13–16% growth in procedures in 2025.

- Ongoing expansion into specialties like colorectal and orthopedic procedures adds volume.

- The overall trend tracks toward doubling robotic‑assisted surgeries in the next 5–7 years.

- Implementation in community hospitals is increasing as training spreads.

Global Surgical Robotics Market by Procedure Type (2025)

- General Surgery leads the market with a dominant 34% share, highlighting its widespread adoption for minimally invasive and complex procedures.

- Orthopedic Surgery accounts for 28% of the market, driven by strong demand for robot-assisted joint replacements and spinal surgeries.

- Abdominal and Pelvic Surgery represents 18%, reflecting the growing use of robotics in colorectal, gynecologic, and laparoscopic procedures.

- Urologic Surgery holds a 11% share, supported by continued adoption in prostate, kidney, and bladder surgeries.

- Other Surgeries contribute the remaining 9%, indicating expanding robotic use across specialty and emerging surgical applications.

- Overall, the data shows that over 62% of the surgical robotics market is concentrated in general and orthopedic procedures, underlining their commercial and clinical importance in 2025.

- The distribution highlights a clear shift toward precision-driven, robot-assisted surgeries, reinforcing robotics as a core technology in modern operating rooms.

Utilization rates across surgical specialties using robotics

- Robotic surgery accounts for roughly 15% of all surgical procedures in high‑adoption regions such as the U.S. in 2025.

- Urology leads adoption with rates near 25% robotic procedures in current practice.

- Gynecology also shows high utilization, with around 22% of procedures being robotic‑assisted.

- General surgery adoption is roughly 18% of cases in markets with advanced robotics penetration.

- Robotic techniques are increasingly used in colorectal, thoracic, and bariatric procedures, with utilization rising annually.

- Specialty programs report high robotic utilization in prostate and hysterectomy procedures, often exceeding national averages.

- Training programs in urology report >85% use of robots in residency curricula in major medical centers.

- Complex surgical fields like cardiothoracic and head and neck surgery are showing gradual utilization increases, though from lower baselines.

Leading vendors and surgical systems in the robotics field

- Intuitive Surgical holds nearly 60% market share in global surgical robotics.

- Over 10,763 da Vinci systems installed worldwide as of Q3 2025.

- Da Vinci platforms enabled ~2.68 million procedures in 2024.

- 427 da Vinci systems placed in Q3 2025, including 240 da Vinci 5.

- CMR Versius completed over 40,000 procedures globally outside the U.S.

- Versius systems are used in 30+ countries across multiple specialties.

- Medtronic Hugo RAS performed tens of thousands of procedures in 30+ countries.

- Stryker Mako surpassed 1 million procedures worldwide with 1,000+ systems.

- North America dominates with ~39-50% of the global robotic surgery market.

Adoption of Robotic Surgery by Hospital Type

- Teaching hospitals dominate robotic surgery adoption, with an impressive 85% adoption rate, highlighting their role as early adopters of advanced surgical technologies.

- Hospitals with fewer than 200 beds show notable uptake, reporting a 42% adoption rate, indicating growing penetration of robotic systems beyond large academic centers.

- Hospitals with more than 500 beds lag in adoption, with only 15% using robotic surgery, suggesting higher operational complexity and cost barriers.

- The data shows a strong correlation between teaching status and technology adoption, as training, research funding, and surgeon expertise accelerate robotic surgery use.

- Smaller and mid-sized hospitals are emerging growth drivers, as robotic platforms become more accessible and cost-efficient.

- The adoption gap between teaching and non-teaching hospitals highlights unequal access to robotic surgery technologies across healthcare institutions.

Key statistics on the Da Vinci Surgical System

- Over 14 million cumulative procedures have been performed using da Vinci systems.

- More than 2.68 million procedures were completed in 2024 alone using da Vinci platforms.

- Da Vinci systems are installed in about 69 countries worldwide.

- Roughly 11–13% annual growth in da Vinci system placements was reported in recent years.

- U.S. installations dominate placements, followed by Europe and Asia‑Pacific markets.

- Da Vinci system revenue showed notable increases in recent reporting periods, reflecting high clinical demand.

- Newer models (e.g., da Vinci 5) accounted for a major share of robotic system rollouts.

- Intuitive projects continued 13–16% growth in procedures into 2025.

Clinical outcomes associated with robotic‑assisted procedures

- Robotic procedures often show lower complication rates compared with open surgery in many specialties, as reflected in procedural metrics.

- AI‑assisted robotic systems have been linked to 30% fewer intraoperative complications in some studies.

- Robotic‑assisted interventions can reduce operative time by 25% versus some manual methods.

- Many robotic surgeries result in shorter hospital stays and rapid recovery compared to traditional techniques.

- Some specialties record significant reductions in readmission rates with robotics.

- Large procedure volumes help refine clinical protocols and improve outcomes.

- Patient satisfaction in minimally invasive robotic procedures trends high due to reduced trauma.

- Long‑term efficacy of robotic interventions continues to be evaluated in ongoing clinical research.

Success and survival rates in robotic‑guided surgeries

- Robotic prostatectomy achieves a 5-year biochemical recurrence-free survival of 84.9%.

- Robotic hysterectomy reports success rates of 95-97% across studies with 300-750 patients.

- High-volume robotic centers show 98% survival in 400 cardiac surgeries.

- Robotic low anterior resection yields 92.8% 5-year overall survival comparable to laparoscopic.

- Robotic cardiac bypass surgery demonstrates >90% 5-year survival and graft patency.

- Learning curve for robotic cystectomy requires 9-50 cases for improved success rates.

- AI-assisted robotic surgeries reduce complications by 30% versus manual methods.

- Robotic endometrial staging matches open with 92% 5-year overall survival.

- High-volume robotic colectomy is linked to lower major adverse events.

Global Surgical Robot Units Growth

- In 2016, there were 713 surgical robot units installed worldwide, marking the early stages of large-scale robotic surgery adoption.

- By 2017, the global count increased to 826 units, reflecting a year-over-year rise of 113 units.

- This represents an approximate 15.8% growth in just one year, showing accelerating interest from hospitals and surgical centers.

- Looking ahead, the number of surgical robot units worldwide is forecast to reach 2,112 units by 2025.

- The 2025 projection is nearly 3× higher than 2016 levels, highlighting strong long-term market expansion.

- This rapid growth is driven by advancements in surgical precision, minimally invasive procedures, and rising demand for better patient outcomes.

- Increasing investments by healthcare providers signal that robot-assisted surgery is becoming a standard surgical approach globally.

Complication and conversion metrics in robotic interventions

- A meta‑analysis across robotic abdominal surgeries found significantly lower open conversion risk with robotics compared with traditional laparoscopy in many procedures.

- Robotic surgery was associated with significantly lower 30‑day postoperative complications (13.2% vs 23.7%) in some comparative studies.

- Robotic procedures can reduce blood loss and intraoperative injuries compared with conventional laparoscopic surgery.

- Laparoscopic approaches typically exhibit higher conversion to open surgery rates than robotic methods in key studies.

- Some robotic procedures show higher early postoperative complications, likely linked to longer operative times and learning curves.

- Meta‑analyses note variable outcomes across specialties, underscoring the need for high‑quality randomized evidence.

- Overall conversion rates to open surgery tend to be lower with robotics in complex cases involving pelvic and abdominal approaches.

- Interventional teams with extensive robotic experience often report better complication profiles than centers in early adoption phases.

Statistics on operating time and hospital stay reductions

- Robotic surgery often extends operating times by 20–55 minutes compared to laparoscopy across procedures like gastrectomy and colorectal resection.

- AI-assisted robotics reduces operative time by 25% and intraoperative complications by 30% versus manual techniques.

- Hospital stays shorten by 20% (from 10 to 8 days) with robotics versus open cystectomy.

- Robotic procedures cut 90-day readmissions by 52% (21% vs 32%) compared to open surgery.

- RAS lengthens operative time by 55.76 minutes (95% CI -74 to -37.5 min) over laparoscopy in meta-analyses.

- Patient recovery times decrease by 15% with AI-enhanced robotic surgery.

- In colorectal resections, robotics reduces conversion rates (3.6–6.1% vs 9.4–11.1%) and shortens hospital stays by <1 day.

- Robotic bariatric revisional surgery achieves shorter stays despite longer times (165 vs 122 min).

- AI robotics improves precision by 40%, aiding shorter stays (1–3 days) in systematic reviews.

Economic implications and cost factors of robotic operations

- Robotic‑assisted surgeries cost an average of $3,279 more in total hospitalization than laparoscopy per meta-analyses.

- Disposable instruments in robotic cholecystectomy cost $1,309 vs $534 for laparoscopic.

- Robotic procedures average $12,340 total cost vs $10,227 for laparoscopic.

- The Da Vinci robot’s purchase price reaches up to $2.5 million, with $100,000 annual maintenance.

- Robotic colectomy incurs $745 more per case than laparoscopy societally.

- Robotic operations completed cost $16,949 vs $15,250 payments for laparoscopic.

- Operating theatre costs are higher for robotic at €7,532 vs €3,351 for open ventral hernia.

- Robotic hysterectomy shows the lowest cost increase vs laparoscopic among procedures.

- Annual maintenance fees for robotic systems range from $100,000 to $200,000.

Surgical Robots Market by Region

- North America leads the surgical robots market due to its advanced healthcare infrastructure, high hospital spending, and early adoption of robot-assisted surgical systems.

- The region benefits from strong reimbursement frameworks and a high concentration of leading medical technology companies.

- Europe is witnessing rapid growth, with the U.K. emerging as the fastest-growing country in the regional surgical robotics market.

- Growth in Europe is supported by increasing adoption of minimally invasive surgeries and rising investments in robotic surgery training programs.

- APAC (Asia-Pacific) is becoming a major growth hub as top players intensify investments in R&D activities to develop next-generation surgical robots.

- Countries in APAC are focusing on cost-effective robotic solutions, local manufacturing, and technological innovation.

- Overall, the global surgical robots market shows region-specific growth dynamics, driven by infrastructure strength in North America, rapid adoption in Europe, and innovation-led expansion in APAC.

Comparison of outcomes: robotic vs open and laparoscopic techniques

- Robotic colorectal surgery shows 9.86% conversion to open vs 29.27% in laparoscopic.

- Robotic rectal cancer surgery has 7.01% severe postoperative complications (C-D III-V) vs 10.13% in laparoscopic.

- Rectal cancer robotic achieves 87.3% 3-year disease-free survival vs 83.6%laparoscopic.

- Robotic surgery yields an 8-day average hospital stay vs 10-day average in open procedures.

- Laparoscopic rectal surgery operative time is 41.48 minutes shorter than robotic on average.

- Robotic cholecystectomy conversion to open is 2.3% with 93.2% success rate.

- Robotic vs laparoscopic rectal cancer: conversion OR 0.27, major complications OR 0.70.

- Robotic IPAA shortens hospital stay by 1.1 days vs laparoscopic.

- Robotic rectal resection harvested 23.2 lymph nodes vs 24.1laparoscopic, comparable margins.

AI integration and automation trends in surgical robotics

- AI-assisted robotic surgeries achieve a 25% reduction in operative time compared to manual methods.

- Surgical precision improves by 40% in AI-enhanced robotic tumor resections and placements.

- Intraoperative complications drop by 30% with AI integration in robotic systems.

- Patient recovery times shorten by an average 15% using AI-capable surgical robots.

- Autonomous cutting tasks in robots reach an 85% success rate at 5.10 seconds per action.

- Automatic suturing achieves 90% success in needle grasping and 92% instrument positioning accuracy.

- AI-driven analytics boost surgeon workflow efficiency by 20% in robotic procedures.

- Healthcare costs are reduced by 10% through AI robotics adoption in surgeries.

- The AI-based surgical robots market grows at 18.5% CAGR from 2024 to 2029.

- Real-time tissue and instrument recognition hits 89% accuracy in AI surgical systems.

Forecasts and future directions in robotic surgical technology

- The global robotic surgery market is projected to grow from $12.8 billion in 2025 to $38.2 billion by 2032, with a CAGR of 16.9%.

- Some projections see medical robot markets reaching $39 billion by 2034.

- Increased adoption in general surgery and minimally invasive sectors is expected to drive volume growth.

- AI capabilities and automation features are poised to further expand the clinical scope of robotic platforms.

- Broader integration of robotics in community and mid‑tier hospitals is anticipated as costs moderate and training spreads.

- Innovations in haptic feedback and ergonomic designs may enhance surgeon performance.

- Tele‑presence and remote surgery concepts could redefine access to specialized care globally.

- Expansion into AI‑assisted decision support systems represents a major research and investment frontier.

Frequently Asked Questions (FAQs)

The global robotic surgical procedures market is forecast to reach approximately $13.32 billion in 2025.

The market is expected to grow at a CAGR of about 17.9% between 2025 and 2032.

Robotic surgery is used in roughly 15% of surgical procedures, according to recent adoption estimates.

North America accounted for a market share of about 74.7% in 2024.

There were 22,700 robot‑assisted procedures in Q1 2024, representing a 45% increase compared with the same period in 2023.

Conclusion

Robotic surgery continues its rise as a pivotal force in modern surgical care. Data show measurable advantages in reduced conversions, shorter stays, and promising AI integration, even as costs and operative times remain focal points for improvement. With markets forecast to triple in size by 2032, the technology’s reach will expand across specialties and regions, reshaping how surgeons operate and patients recover. As research evolves and automation deepens, stakeholders will watch closely how robotics balances safety, cost, and outcomes in next‑generation healthcare.