Cloud gaming has shifted from a niche technology to a mainstream gaming model. Players can now stream high-end games on smartphones, smart TVs, laptops, and tablets without investing in expensive gaming hardware. This shift is influencing subscription services, telecom infrastructure, and digital entertainment ecosystems worldwide.

Businesses use cloud gaming to expand game accessibility, while telecom providers leverage it to drive 5G adoption and network upgrades. As platform competition intensifies and user demand grows, cloud gaming continues to reshape how games are distributed and consumed. Explore the latest statistics to understand the industry’s growth trajectory.

Editor’s Choice

- The global cloud gaming market is estimated at $6.23 billion in 2026, with forecasts indicating growth to $21.62 billion by 2031.

- Cloud gaming users worldwide reached approximately 395.9 million in 2024, creating a strong foundation for continued growth through 2026.

- The cloud gaming market is projected to grow at a 28.25% CAGR between 2026 and 2031.

- Asia-Pacific accounted for roughly 46% of the global cloud gaming market share in 2024.

- Some market forecasts estimate cloud gaming revenue could exceed $28 billion in 2026, reflecting rapid platform expansion.

- North America represented about 43% of global cloud gaming revenue in 2025, making it the largest regional market.

- Increasing 5G deployment and edge computing infrastructure remain the two biggest drivers behind cloud gaming adoption worldwide.

Recent Developments

- Major smart TV manufacturers introduced native cloud gaming support, reducing the need for dedicated consoles in 2026.

- Native 4K 120Hz cloud gaming support appeared in premium televisions during 2026 product launches.

- Cloud infrastructure investment is expected to increase by 27% in 2026, supporting gaming and AI workloads.

- Global cloud spending reached $399.6 billion in 2025, reflecting stronger backend infrastructure for cloud gaming services.

- Several providers expanded cloud gaming availability to streaming devices and smart TV ecosystems during 2025 and 2026.

- Rising GPU and hardware costs are pushing more gamers toward streaming-based gaming alternatives.

- Microsoft reportedly tested an ad-supported cloud gaming tier to broaden accessibility among casual users.

- Cloud gaming services increasingly support owned game libraries instead of requiring separate platform purchases.

- Network operators are developing real-time cloud gaming quality monitoring systems to improve user experiences.

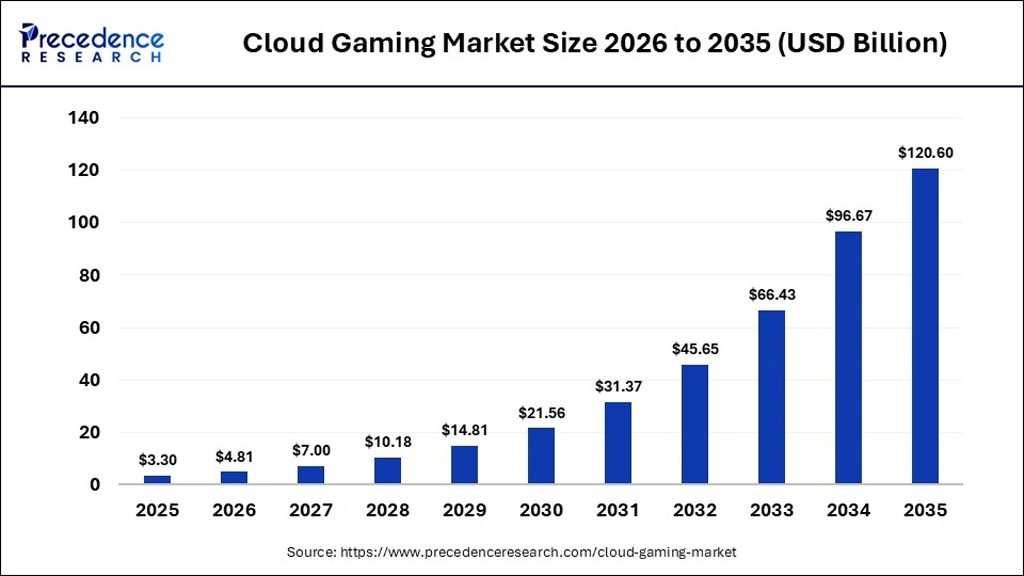

Global Market Size of Cloud Gaming Statistics

- Cloud gaming market size is projected to grow from $3.30 billion in 2025 to $120.60 billion by 2035.

- The industry is expected to expand by 36.5x over the 2025–2035 forecast period.

- Market value is forecast to surpass $10 billion for the first time in 2028, reaching $10.18 billion.

- The cloud gaming market is expected to exceed $45.65 billion by 2032, highlighting rapid adoption.

- Revenue is projected to climb from $66.43 billion in 2033 to $96.67 billion in 2034, adding over $30 billion in one year.

- By 2035, the market is forecast to cross the $120 billion milestone, reaching $120.60 billion.

- Between 2030 and 2031, the market size is expected to increase from $21.56 billion to $31.37 billion, a gain of 45.5%.

- The market is projected to nearly double from $45.65 billion in 2032 to $96.67 billion in 2034.

- Annual market value is forecast to remain above $20 billion from 2030 onward.

- The largest absolute increase is expected between 2034 and 2035, with revenue rising by $23.93 billion.

Revenue Generated by Cloud Gaming Statistics

- The cloud gaming market generated approximately $2.27 billion in revenue during 2024.

- Industry revenue is projected to reach between $4.8 billion and $6.8 billion in 2026, depending on market definitions.

- One forecast suggests cloud gaming revenue will rise from $19.29 billion in 2025 to $28.29 billion in 2026.

- Market analysts expect annual revenue growth rates above 25% through the early 2030s.

- The industry could generate more than $120 billion annually by 2035 under aggressive adoption scenarios.

- Subscription-based monetization remains the dominant revenue model across major cloud gaming platforms.

- Premium cloud tiers offering RTX-powered graphics and 4K streaming command higher monthly revenue per user.

- Cross-device gaming ecosystems continue to increase customer lifetime value for platform operators.

- Revenue growth is increasingly tied to smart TV adoption and connected living-room experiences.

Demographic Trends in Cloud Gaming

- Casual gamers are expected to contribute a massive 78.8% of the overall cloud gaming market share by 2026.

- Smartphones dominated the cloud gaming device sector, holding a substantial 46.12% of the global market share in 2025.

- The Asia-Pacific region accounted for the largest cloud gaming user base, capturing over 47.9% of the global market in 2025.

- Subscription-based gaming tiers captured a dominant 64.83% of the total industry revenue throughout 2025.

- Over 68% of surveyed cloud gamers ranked low-latency streaming as the most critical factor for a satisfactory experience in 2025.

- The laptops and tablets segment is projected to account for a significant 32.14% share of the cloud gaming market in 2026.

- The total number of active cloud gaming users is projected to reach an estimated 455.4 million globally by 2025.

- Over one-third of the 140 million streaming hours logged by major platforms in 2025 came from lower-powered, non-console devices.

- The global cloud gaming market is projected to surge to an impressive $23.79 billion in total valuation by 2026.

Cloud Gaming Market Share

- NVIDIA Corporation leads the cloud gaming market with a dominant 21% market share, making it the largest player in the industry.

- Intel Corporation holds the second-largest position with 16%, strengthening its influence in cloud gaming infrastructure.

- Microsoft Corporation captures 14% of the market, driven by its expanding cloud gaming ecosystem.

- Google Inc. accounts for 11% of the cloud gaming market, maintaining a strong presence among major technology providers.

- Amazon Inc. secures 10% market share, highlighting its growing role in cloud-based gaming services.

- IBM Corporation represents 9% of the market, supported by its enterprise cloud capabilities.

- Apple Inc. holds 8% market share, reflecting its involvement in gaming-related cloud technologies.

- Electronic Arts, Inc. contributes 7% to the market, demonstrating the importance of game publishers in the cloud gaming sector.

- The combined share of Other Key Players stands at 4%, indicating a highly concentrated market among leading companies.

- The top three companies, NVIDIA, Intel, and Microsoft, collectively control 51% of the cloud gaming market.

Device Usage Trends in Cloud Gaming

- Smartphones account for the largest share of cloud gaming sessions globally, capturing over 55% of total market revenue.

- Mobile devices represented more than 50% of cloud gaming usage across several major markets during 2025.

- Smart TV cloud gaming adoption accelerated significantly, supported by a broader smart television market worth $274.1 billion.

- Gaming laptops and tablets remain popular among users, projected to account for a 32.14% market share by 2026.

- Video streaming devices have broadened living-room access, dominating the cloud gaming sector with a 57% share in 2025.

- Cross-device gaming enables over 395 million active users to seamlessly switch platforms without downloading game files.

- Browser-based gaming remains a preferred instant-access option, seamlessly delivering 1080p resolution at 60 frames per second.

- Gaming consoles continue to hold significant relevance in the cloud space, maintaining a robust 49% device market share.

- Growth in connected TV and cloud gaming is expected to outpace traditional methods, reaching $159.26 billion by 2034.

Regional Analysis of Cloud Gaming Statistics

- Asia-Pacific accounted for approximately 46% of the global cloud gaming market share in 2024.

- North America generated around 43% of the global cloud gaming revenue in the year 2025.

- The United States remains a mature market, holding over 87% of its regional cloud gaming share in 2024.

- China continues to drive significant growth supported by a massive base of over 700 million mobile gamers.

- Japan and South Korea rank among the leading markets, leveraging advanced networks with over 90% 5G penetration.

- Europe continues expanding its broadband infrastructure and is projected to grow at a 43% CAGR through 2030.

- Latin America is emerging as a high-growth region projected to reach $932.1 million in market revenue by 2030.

- The Middle East is experiencing rapid adoption and tracking as a fast-growing market with a 29.35% CAGR into 2031.

- India represents a massive opportunity as its mobile-first 5G subscriber base expands to 700 million by 2028.

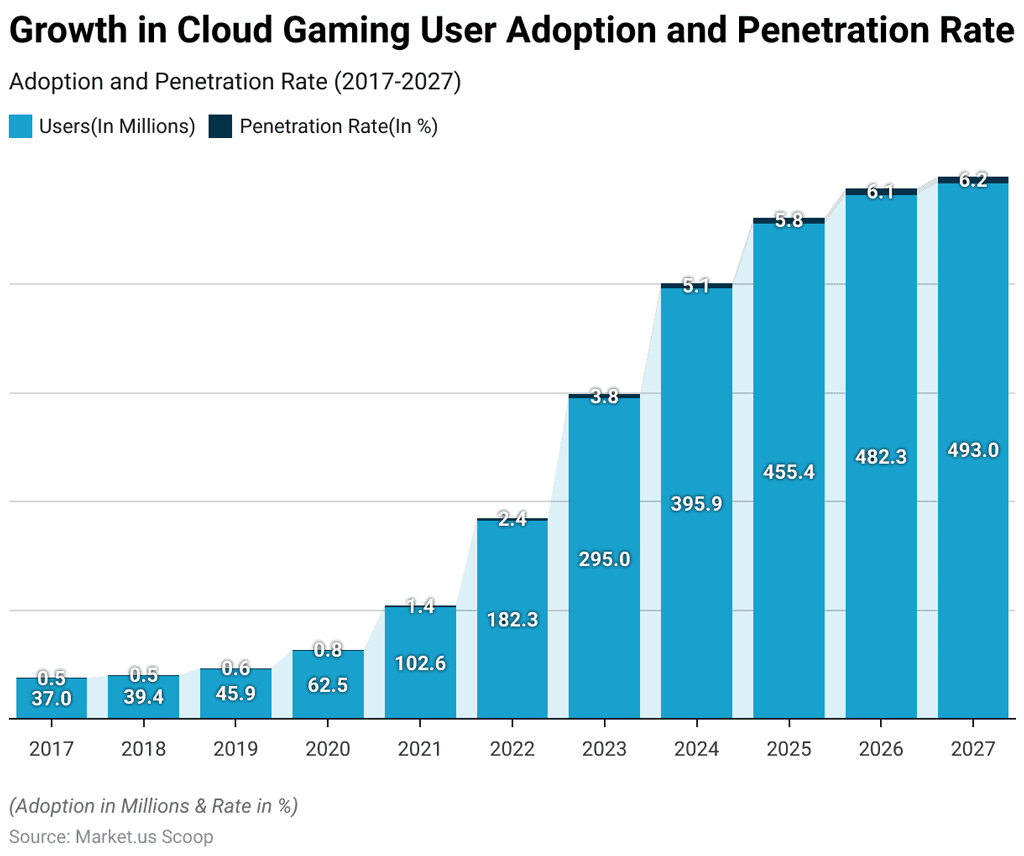

Cloud Gaming Adoption Growth

- Cloud gaming users surged from 37.0 million in 2017 to 493.0 million in 2027, representing more than a 13x increase over the decade.

- The penetration rate climbed from 0.5% in 2017 to 6.2% in 2027, highlighting the industry’s expanding global reach.

- Between 2021 and 2022, the user base jumped from 102.6 million to 182.3 million, an increase of nearly 77.7%.

- 2023 marked a major milestone, with cloud gaming adoption reaching 295.0 million users and a 3.8% penetration rate.

- The market added over 100 million new users between 2023 and 2024, rising from 295.0 million to 395.9 million.

- By 2025, cloud gaming penetration reached 5.8%, while the user base expanded to 455.4 million worldwide.

- User growth remained strong in 2026, with adoption increasing to 482.3 million users and penetration reaching 6.1%.

- The highest recorded adoption in the forecast period is 493.0 million users in 2027, accompanied by a 6.2% penetration rate.

- Cloud gaming adoption crossed the 100 million user mark in 2021 and nearly quadrupled by 2027.

- The data indicates that 2021–2024 was the fastest growth phase, with users increasing from 102.6 million to 395.9 million in just three years.

Subscription Trends in Cloud Gaming

- The global cloud gaming market is projected to reach an estimated $23.79 billion in 2026.

- Xbox Game Pass officially surpassed 34 million subscribers across its service tiers by early 2024.

- Video streaming subscription models are expected to dominate with a 59.8% market share in 2026.

- The premium Xbox Game Pass Ultimate tier accounts for an impressive 68% of all active platform subscriptions.

- Casual gamers drive multi-device adoption, making up 78.8% of the cloud gaming subscriber base in 2026.

- The overarching cloud gaming industry is forecast to expand at a rapid CAGR of 50.2% from 2026 to 2033.

- North America remains the dominant region for subscription revenue, expected to generate $10.2 billion in 2026.

- Mobile-first subscriptions are rising, with smartphones capturing a 38.7% device market share in 2026.

- The shift toward subscription models is heavily supported by a massive audience of 227 million active gamers in the US.

Consumer Behavior in Cloud Gaming

- Over 40% of gamers cite expensive hardware as their primary reason for trying cloud gaming.

- Approximately 65% of active users prefer subscription-based access over individual game purchases.

- Nearly 70% of consumers treat cloud streaming as a complement to traditional consoles.

- Casual players account for more than 60% of the total cloud gaming audience globally.

- A massive 85% of subscribers demand cross-platform progression and cloud save functionality.

- More than 75% of consumers are likely to adopt a service if a free trial is offered.

- Gen Z and Millennials drive the market by making up nearly 80% of all cloud gaming adoption.

- About 55% of users rank game availability as their top purchasing factor.

- Exactly 33% of players highlight zero hardware maintenance as a definitive driver for subscriptions.

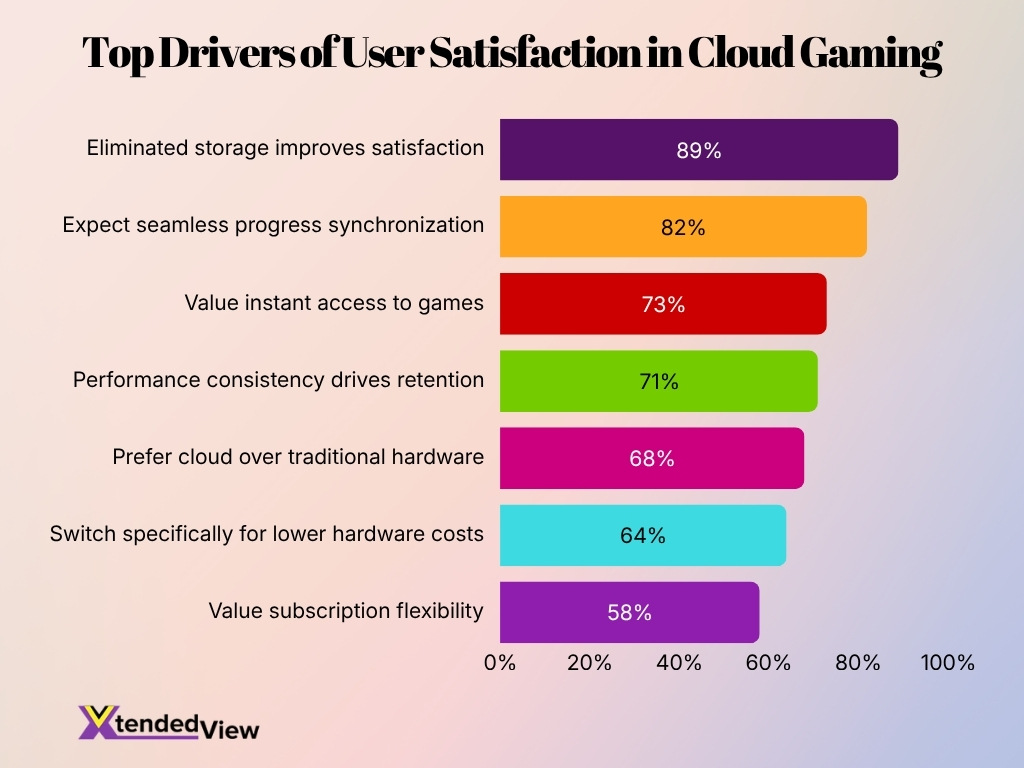

User Satisfaction and Preferences in Cloud Gaming

- 68% of users prefer cloud gaming over traditional hardware purely for unmatched convenience.

- 73% of gamers rank instant access to games as their most valued platform feature.

- 58% of casual players value subscription flexibility more than high-end hardware specifications.

- Platform satisfaction is 85% higher when users can access games across multiple devices.

- 64% of budget-conscious gamers switch to cloud ecosystems specifically for lower hardware costs.

- 71% of subscribers cite performance consistency as the single most important driver of customer retention.

- A game library exceeding 400 titles actively increases overall subscription renewal rates by 27%.

- 82% of players now expect seamless progress synchronization and cloud saves across all screens.

- 89% of surveyed users say that eliminating storage requirements drastically improves their platform satisfaction.

Performance and Latency in Cloud Gaming

- A minimum download speed of 15 to 25 Mbps is required for a stable 1080p cloud gaming session.

- Competitive multiplayer titles strictly demand a latency below 20 milliseconds to ensure real-time action synchronization.

- Visible input lag and gameplay degradation become highly prominent once latency crosses the 80 milliseconds mark.

- Streaming cloud games at 4K resolution consistently consumes a massive 35 to 50 Mbps of active bandwidth.

- Transmitting real-time controller inputs to the cloud server requires a continuous upload speed of 3 to 5 Mbps.

- Experiencing network packet loss above 1% directly triggers frequent disconnections and severe frame drops.

- Heavy cloud gaming sessions can rapidly consume between 5 GB and 20 GB of network data per hour.

- Upgrading to a direct Ethernet connection minimizes network interference and can stabilize ping under 5 milliseconds.

Impact of 5G on Cloud Gaming Growth

- The global cloud gaming market is projected to surge from $23.79 billion in 2026 to $159.26 billion by 2034 alongside 5G expansion.

- 5G adoption is expected to drive the cloud gaming industry at a massive compound annual growth rate (CAGR) of 44.3% through 2030.

- Smartphones are forecast to capture a 38.7% market share by 2026 as 5G enables console-quality gaming on mobile devices.

- The Asia-Pacific region holds over 45% of the cloud gaming market due to early and aggressive 5G infrastructure investments.

- 5G networks reduce transmission latency to under 20 milliseconds, effectively eliminating the input lag that traditionally hindered cloud gaming.

- The video streaming segment dominates with over a 54% market share as faster 5G speeds bypass the need for physical game downloads.

- The global base of active cloud gaming users is projected to exceed 87 million as stable 5G connectivity reaches wider audiences.

- The U.S. cloud gaming market is anticipated to hit $8.24 billion by 2026, fueled by rapid 5G deployment and consumer demand.

- Modern 5G networks easily surpass the strict 10 Mbps transmission baseline required for uninterrupted high-definition cloud gaming.

- Casual gamers will account for up to 78.8% of the market by 2026, leveraging the instant accessibility provided by 5G cloud platforms.

Xbox Cloud Gaming Statistics

- Xbox Game Pass surpassed 34 million subscribers, providing a massive built-in user base for cloud streaming.

- By early 2022, the cloud service officially reached a milestone of 25 million active subscribers.

- The gaming platform generated overall revenue exceeding $450 million during the 2021 fiscal year.

- Over 10 million people globally had streamed games via Xbox Cloud Gaming by mid-2022.

- Players across 26 countries have accessed the platform using over 6,000 different device types.

- Standard gameplay streaming at 1080p and 60fps consumes between 5 GB and 9 GB of data per hour.

- The premium 1440p resolution tier utilizes up to 14 GB of data per hour for supported titles.

- More than 125 developers have optimized over 350 catalog games specifically for cloud performance.

NVIDIA GeForce NOW Statistics

- NVIDIA GeForce NOW surpassed 25 million registered users worldwide.

- The platform supports more than 2,000 games, making it one of the industry’s largest cloud gaming libraries.

- GeForce NOW allows users to stream games they already own from supported digital storefronts.

- Premium membership tiers offer RTX-enabled ray tracing and advanced graphics capabilities.

- Ultimate subscribers can access streaming resolutions up to 4K on supported devices.

- GeForce NOW operates data centers across North America, Europe, and Asia-Pacific regions.

- The service supports PCs, Macs, Chromebooks, smartphones, tablets, smart TVs, and browsers.

- NVIDIA continues expanding publisher partnerships to increase available game content.

- GeForce NOW is widely viewed as a leading option for PC gamers seeking high-end cloud gaming performance.

Infrastructure and Technology Trends in Cloud Gaming

- The global cloud gaming market size is projected to grow to $23.79 billion in 2026 and reach $159.26 billion by 2034.

- Edge computing processes data directly near the source to cut network latency down to an ultra-low 1–10 milliseconds.

- The file streaming segment for cloud platforms is anticipated to secure a massive 52.54% global market share in 2026.

- Expanding 5G networks are built to maintain an end-to-end network latency of 20–30 milliseconds for fast-paced multiplayer interactions.

- Approximately 75% of enterprise data is anticipated to be processed at the edge by 2025, a massive leap from just 10% historically.

- Implementing modern cloud-native frameworks has allowed gaming operators to achieve up to a 25% reduction in server deployment times.

- The shift toward cloud gaming services successfully expands the addressable market by an estimated 30% in regions lacking console penetration.

- North America maintained its dominance in the cloud gaming infrastructure market, accounting for a massive 43.00% revenue share in 2025.

- Relying on local edge processing can successfully cut data transfer latency by up to 90% when compared to standard 4G centralized cloud systems.

- The laptops and tablets segment is forecasted to heavily lead device usage in cloud gaming by holding a 32.14% share in 2026.

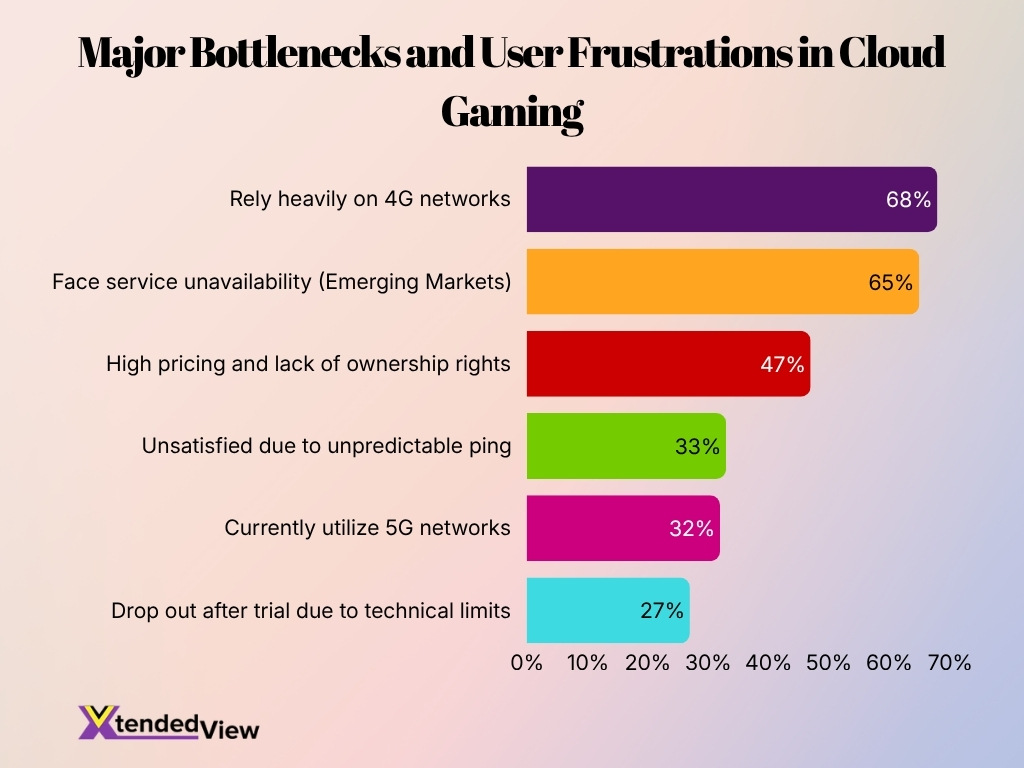

Challenges and Limitations of Cloud Gaming

- A significant 27% of users drop out after trials due to technical limitations like network latency.

- Approximately 68% of players rely on 4G networks, risking deteriorated quality during periods of congestion.

- Heavy cloud gaming can consume up to 250 GB of data monthly, burdening users with limited broadband plans.

- Nearly 33% of regular cloud gamers remain unsatisfied due to unpredictable ping compared to local hardware.

- Over 65% of potential users in emerging markets face service unavailability due to severe infrastructure constraints.

- Operating heavy cloud servers generates 0.44 kilograms of CO2 per hour, pressuring provider profitability and sustainability.

- Cloud platforms currently capture just 38% of the online market owing to strict publisher content licensing limitations.

- Only 32% of cloud gamers currently utilize 5G networks, leaving many rural users with inconsistent performance.

- Almost 47% of former users cited high pricing and lack of ownership rights as major barriers to adoption.

Future Projections for the Cloud Gaming Industry

- The global cloud gaming market is forecast to reach approximately $21.62 billion by 2031.

- Some forecasts estimate the market could exceed $33.7 billion by 2033.

- Aggressive growth scenarios suggest cloud gaming revenue could surpass $78 billion by 2034.

- Industry growth rates are expected to remain above 20% annually throughout much of the next decade.

- Smart TVs are projected to become one of the fastest-growing cloud gaming access points.

- Subscription models are expected to remain the dominant revenue source across the industry.

- Improved 5G coverage will significantly expand mobile cloud gaming opportunities worldwide.

- AI-driven optimization technologies are expected to improve streaming quality and reduce infrastructure costs.

- Continued investment from major technology companies is likely to accelerate innovation and mainstream adoption.

Frequently Asked Questions (FAQs)

The global cloud gaming market is valued at $6.23 billion in 2026 and is projected to reach $21.62 billion by 2031, growing at a 28.25% CAGR.

The global cloud gaming user base reached approximately 395.87 million users in 2024 and is projected to continue growing over the next several years.

North America accounted for approximately 43% of global cloud gaming revenue in 2025, making it the largest regional market.

Industry forecasts estimate cloud gaming will grow at a CAGR ranging from 25.7% to 44.3%, depending on the forecast period and methodology used.

NVIDIA GeForce NOW has surpassed 25 million registered users worldwide, making it one of the largest dedicated cloud gaming platforms.

Conclusion

Cloud gaming continues to evolve from a niche innovation into a mainstream segment of the gaming industry. Advancements in cloud infrastructure, broader 5G availability, and the growth of subscription-based gaming ecosystems have accelerated user adoption across North America, Asia-Pacific, and Europe.

The statistics show that major providers are investing heavily in content libraries, cloud infrastructure, and device compatibility. At the same time, smart TVs, smartphones, and browser-based gaming are making cloud gaming more accessible than ever before. Although latency, infrastructure costs, and content licensing remain challenges, long-term forecasts indicate sustained double-digit growth through the next decade.

As connectivity improves and hardware barriers decline, cloud gaming is positioned to become a central pillar of the global gaming ecosystem.