Mobile banking has transformed from a convenience into a global necessity. With billions managing accounts, paying bills, and investing directly from their phones, it’s redefining how people interact with money. From major U.S. banks offering AI-powered mobile features to fintech startups driving inclusion across emerging markets, the growth is rapid and revolutionary. In this data-driven report on Mobile Banking Statistics. We explore how technology, consumer behavior, and innovation are shaping the next era of digital finance.

Editor’s Choice

Here are some of the key statistics that stand out:

- Globally, the mobile banking market reached an estimated $1.92 trillion in 2025, growing about 28% year-on-year.

- In the U.S., 72% of adults use mobile banking apps in 2025, up from 65% in 2022 and 52% in 2019.

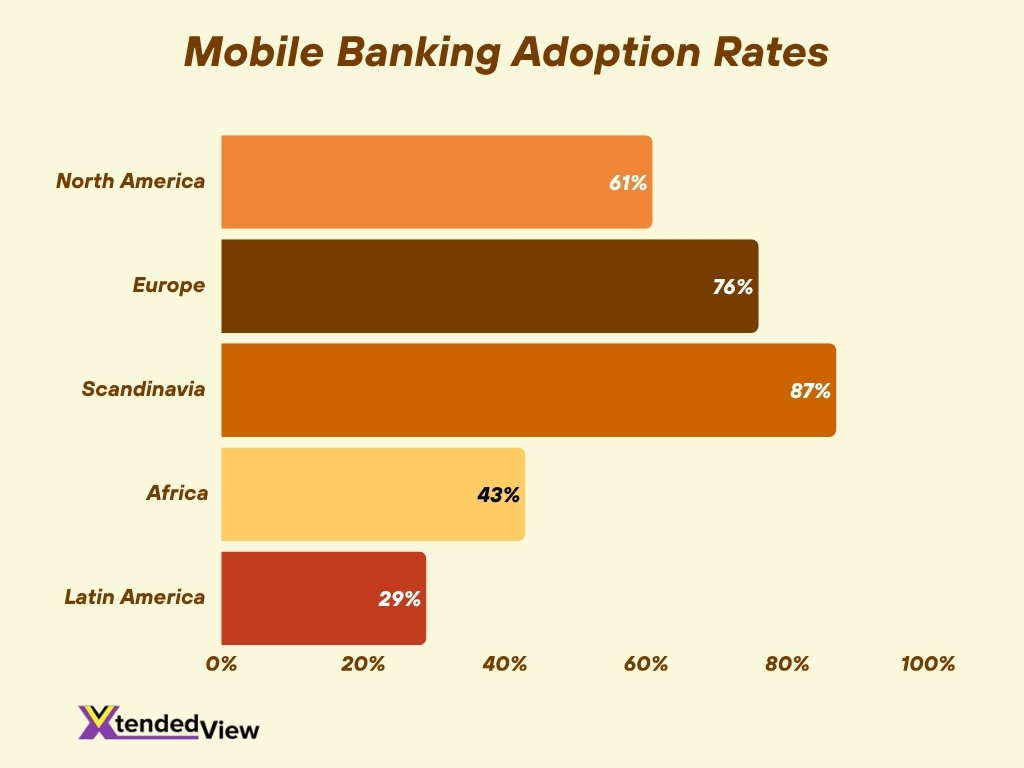

- Mobile banking penetration in North America is at 61% in 2025.

- In Europe, adoption reached 76% in 2025, while top markets like Scandinavia exceeded 87%.

- From the Global Findex Database 2025, 79% of adults globally have an account in formal financial services.

- In 2025, digital banking, including mobile, is projected to generate net interest income of about US $1.61 trillion globally.

- According to McKinsey & Company, mobile is now the most widely used banking channel and will accelerate further.

Recent Developments

- In 2025, digital banks worldwide are projected to generate net interest income of approximately $1.61 trillion, up from prior years.

- Mobile banking has become the most widely used channel in banking and will continue to gain as generative AI is embedded in financial services.

- Banking apps are resolving a growing share of routine interactions end-to-end, reducing reliance on branches and call centers.

- The global digital banking sector, including mobile, is undergoing transformation via 5G connectivity, open-banking APIs, and super-app integrations.

- In the U.S., mobile banking has overtaken branches as the primary access point. In 2024, 55% of consumers said mobile was their main channel.

- Offline and hybrid banking models are being reconsidered, while branches remain for complex services, many banks are shifting resources toward mobile channels.

- Regulatory and compliance pressures are increasing, especially around mobile-banking security, data privacy, and platform interoperability.

- Emerging markets are accelerating mobile banking adoption in response to financial inclusion goals and smartphone penetration growth.

Global Mobile Banking Adoption Rates

- An estimated 66% of the world’s population had access to mobile banking in 2025.

- According to the Global Findex 2025, 79% of adults globally hold an account at a financial institution, enabling mobile access for many.

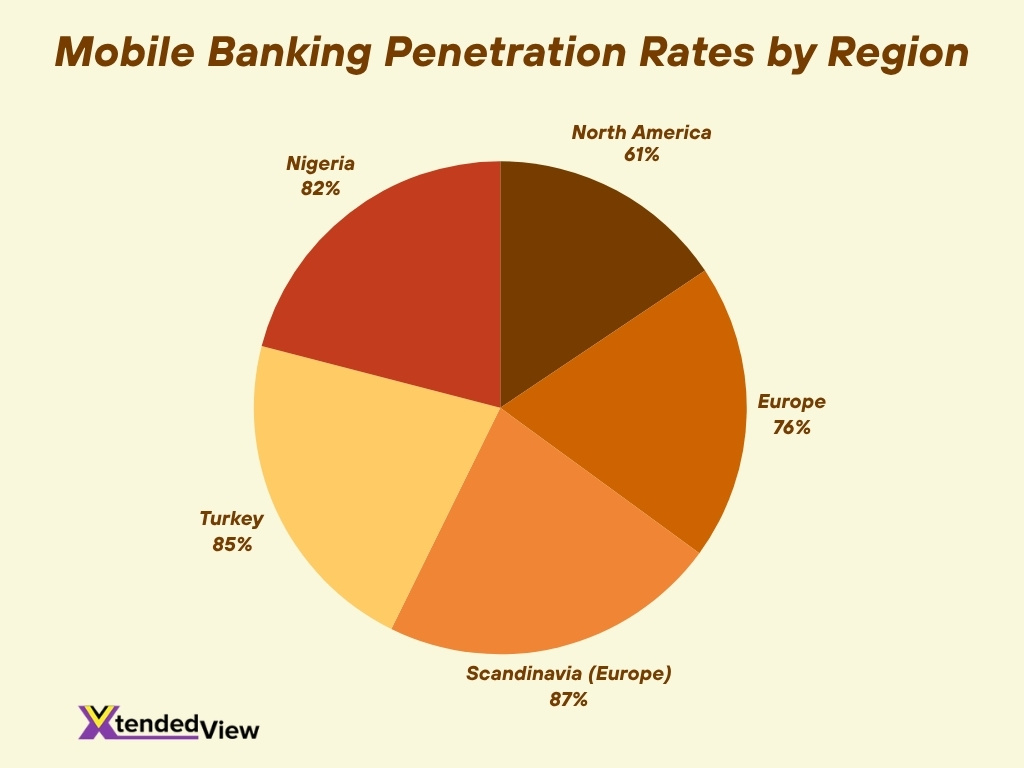

- In developed economies such as North America, mobile banking penetration stands at 61% in 2025.

- Europe reports a 76% adoption rate in 2025, with some markets, for example, Scandinavia, exceeding 87%.

- Africa’s digital banking share, including mobile, increased significantly. In 2025, digital banking penetration rose by +43% in some regions.

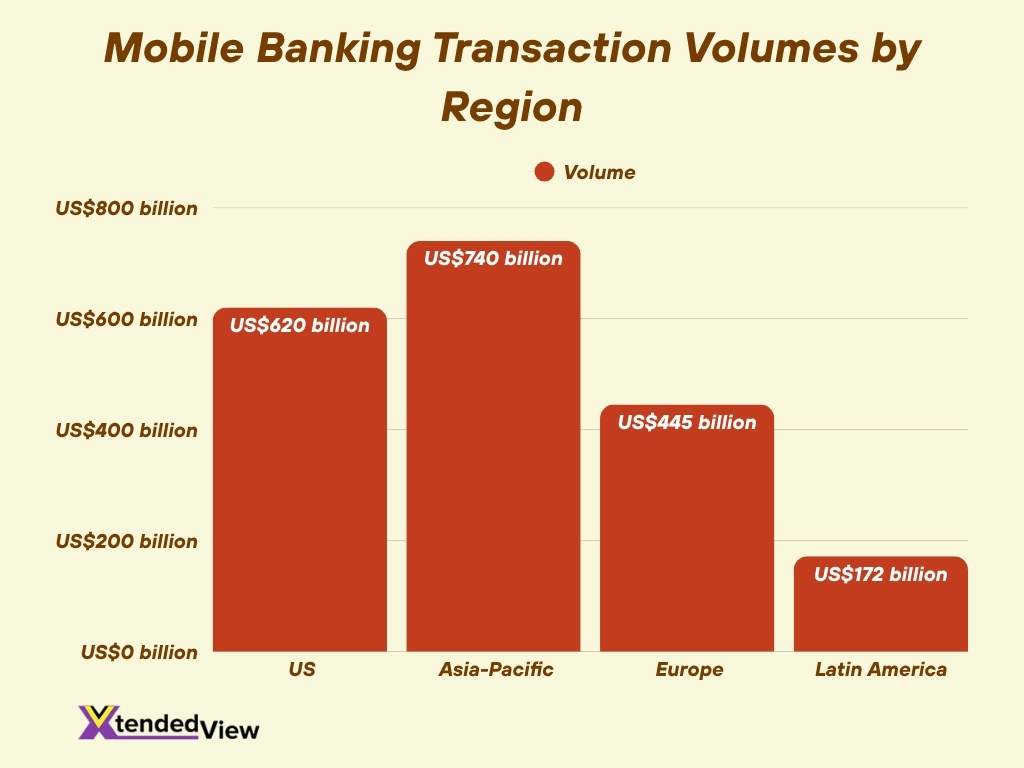

- Asia-Pacific leads large-scale adoption, for example, the Asia-Pacific mobile banking market exceeded $740 billion in revenue in 2025.

- Latin America’s mobile banking market grew by 29% year-on-year in 2025, reaching around US $172 billion in revenue.

- The fact that mobile banking apps will be launched by 89% of banks globally by 2025 signals broad institutional readiness.

Mobile Banking Usage by Country

- In the U.S., 72% of adults use mobile banking apps in 2025, up from 65% in 2022 and 52% in 2019.

- China has approximately 860 million mobile banking users in 2025, making it one of the largest national user bases.

- Turkey reports one of the highest national penetration rates at around 85% in 2025.

- Nigeria’s mobile banking uptake is around 82% in 2025, reflecting strong growth in the West Africa region.

- In India, the Unified Payments Interface (UPI) processed over 20 billion transactions in a month in 2025, demonstrating deep mobile usage.

- Brazil’s mobile payments ecosystem, via channels such as Pix, reported over 2.677 trillion reais in transactions by April 2025.

- In developed Western markets, mobile banking apps are now used by more than two-thirds of adults, for example, 72% in the U.S. and more than 80% in some Scandinavian countries.

Growth of Mobile Banking Over Time

- From 2020 to 2025, global mobile banking users increased by around 35%, reaching an estimated 2.17 billion people.

- In the U.S., mobile banking app downloads rose by approximately 22% in 2025, as demand for mobile banking surged.

- Between 2017 and 2023, global mobile banking usage reportedly tripled in many territories.

- In the Asia-Pacific region, transaction volumes associated with mobile banking grew by 34% in 2025, driven by e-commerce and real-time payments.

- Mobile banking in the U.S. became the primary account access mode by 2024, when 55% of consumers reported using mobile banking as their main banking channel.

- The mobile banking market value was estimated at around US $1.82 trillion in 2024 and is projected to continue strong growth through 2035.

- Banks are reallocating resources from branches to mobile channels, and branch counts in the U.S. have declined as mobile becomes dominant.

Smartphone Penetration and Impact on Mobile Banking

- Globally, there are approximately 7.3 billion smartphones in active circulation in 2025.

- In developed nations, smartphone adoption among adults has crossed 95%, enabling near-universal mobile access.

- In 2025, smartphone app usage time has increased by about 25% in the U.S. since 2019, signalling more time available for mobile banking.

- In India, 85.5% of households possess at least one smartphone, paving the way for mobile banking growth.

- The mobile economy report projects 6.5 billion unique mobile subscribers by 2030, showing how the smartphone base continues expanding.

- With rising smartphone penetration, the share of people able to access mobile banking services has increased; for instance, global mobile banking access was estimated at 66% of the population in 2025.

- Faster mobile networks, for example, 5G, and affordable smartphones are cited as key enablers of mobile banking uptake, especially in emerging markets.

- On a global scale, 87% of mobile handsets in use were smartphones at the start of 2025, indicating that basic phone usage is rapidly diminishing.

- The implication, as smartphone ownership and capabilities grow, mobile banking stands to reach deeper into previously underserved populations and geographies.

Usage of Online and Mobile Banking by Age Group

- Younger users (15–24 years) show a strong preference for mobile banking, with 74.1% primarily using mobile apps and only 6.3% relying on online banking.

- The 25–34 age group continues this trend, 69.4% prefer mobile banking, while 12.9% use online banking, making it the most digitally active group overall (82.3%).

- Among 35–44-year-olds, mobile banking usage begins to decline (60.5%), while online banking grows to 18.4%, signaling a gradual shift in preferences.

- For 45–54-year-olds, the gap narrows, 49.1% use mobile banking, and 22.8% use online banking, indicating a more balanced approach between the two.

- In the 55–64 age group, online banking (27.3%) overtakes mobile banking (33.2%), showing that older adults may favor traditional interfaces over mobile apps.

- Among seniors (65+), the preference clearly shifts, 28.2% use online banking compared to only 15.3% who use mobile banking.

- Overall, digital banking usage declines with age, dropping from 80.4% among youth to just 43.5% among seniors.

- The data highlights a generational divide: younger users value mobility and convenience, while older users prioritize familiarity and accessibility through online platforms.

Key Drivers of Mobile Banking Adoption

- Smartphone availability + affordable connectivity drive accessibility.

- Convenience and 24/7 access motivate users to bank on their own schedule.

- Emergence of fintech and neobanks accelerates adoption via mobile-first banking.

- Shift from branch to mobile channels, digital banking users in the U.S. are projected to reach about 216.8 million by 2025.

- Younger generations are leading change, with Gen Z and millennials driving innovation.

- Regulatory and inclusion pushes promote adoption in emerging markets.

- Features beyond transactions, like budgeting, savings goals, and rewards, increase engagement.

- Trust and digital security improvements through biometrics reduce concerns.

- Cost savings for banks, mobile channels reduce overhead, enhancing provider appeal.

Mobile Banking Transaction Volume

- The global mobile banking market size is estimated at US $1.92 trillion in 2025, a 28% year-on-year increase.

- The U.S. mobile banking sector processed over US $620 billion in transactions in 2025, up from US $500 billion in 2023.

- In the Asia-Pacific region, transaction volume grew by 34% in 2025, driven by e-commerce and QR payments.

- In India, real-time payments via IMPS reached 441 million transactions in December 2024.

- The Asia-Pacific mobile banking market surpassed $740 billion in 2025 revenue.

- Europe’s mobile banking revenue rose to $445 billion in 2025.

- Mobile payments account for approximately 49% of all digital banking transactions globally in 2025.

- The market for digital banking is net interest income of US $1.61 trillion in 2025.

- The implication, mobile banking transactions are not just growing, they are rapidly becoming the core channel for many institutions.

Popular Features of Mobile Banking Apps

- The top mobile banking apps now offer real-time balance updates, transaction categorization, P2P payments, and budgeting tools.

- Biometric authentication is used by over 80% of global mobile banking users in 2025.

- AI-powered fraud detection blocked or flagged approximately 78% of fraudulent mobile transactions in 2025.

- Mobile apps shortened transaction times; average mobile banking transactions are now 68% faster than branch services.

- Super-app functionality, combining banking, payments, savings, and investments, is becoming standard.

- Instant transfers and real-time settlement are key user expectations globally.

- In the U.S., app downloads increased by 22% in 2025, driven by feature demand.

- Apps for older adults emphasize simplified interfaces and offline functionality.

- Mobile banking apps are evolving from “view your balance” to full financial management platforms.

Leading Mobile Banking Apps by User Base

- Revolut reported roughly 60 million global users in 2025.

- In the UK, Monzo had 11 million users, and Revolut about 10.5 million.

- Globally, 89% of banks had launched mobile banking apps by the end of 2025.

- China had 860 million mobile banking users in 2025.

- Turkey, 85%, and Nigeria, 82%, hold the highest national penetration rates.

- Banks are shifting to mobile-first strategies as these customers deliver higher lifetime value.

- Despite adoption, many apps still lack full-service tools like loans and investments.

- The mobile banking ecosystem is expanding both in user base and service maturity.

Security and Privacy in Mobile Banking

- More than 60% of cyberattacks in 2025 target mobile banking apps, making app security a top concern.

- Mobile banking platforms now employ hardware-based protection, biometrics, and real-time fraud risk analysis.

- Digital banking still faces significant fraud risks, prompting proactive frameworks.

- AI-driven tools are projected to reduce fraud by up to 50% by 2025.

- 84% of adults in low- and middle-income countries own a mobile phone, increasing exposure to risk.

- Multi-factor authentication and biometrics are now standard across leading apps.

- User trust remains fragile; many users worry about data use and storage.

- Expanding app features increases the attack surface, requiring a balance between usability and protection.

Mobile Banking for Financial Inclusion

- 79% of adults globally now have a formal financial account, up from 74% in 2021.

- In low- and middle-income countries, 84% of adults own a mobile phone, driving inclusion.

- India’s financial inclusion index rose to 67.0 in 2025, up from 64.2.

- Mobile banking enables access to credit, insurance, and savings without physical branches.

- Digital platforms are lowering account opening costs in remote regions.

- In developing economies, mobile banking is leapfrogging traditional channels.

- Gender and income gaps persist; women and lower-income adults use mobile banking less often.

- Adults with access to emergency funds rose to 56% in 2025.

Regional Trends in Mobile Banking

- North America reached 61% penetration in 2025.

- Europe achieved 76% adoption, with Scandinavian countries exceeding 87%.

- Turkey and Nigeria lead with around 85% and 82% adoption, respectively.

- Asia-Pacific transaction volumes grew by 34% in 2025.

- Latin America grew 29% year-on-year in 2025.

- By 2025, 89% of banks globally had mobile apps.

- Regions with strong 5G and smartphone infrastructure are advancing fastest.

Mobile Wallets and Contactless Payments

- Mobile wallets are projected to serve 5.6 billion users worldwide by 2025.

- In the U.S., 60% of in-store transactions are expected to be contactless.

- Digital wallets account for over 50% of global e-commerce payments by 2025.

- The contactless payments market was valued at USD 57.85 billion in 2024 and is forecast to reach USD 70.08 billion in 2025.

- Super-apps combining mobile banking and wallets are emerging in Asia.

- India’s UPI continues to expand mobile wallet adoption.

- NFC and QR payment systems are expanding to rural markets.

- Cross-border mobile wallet transactions still face regulatory challenges.

Customer Preferences in Mobile Banking

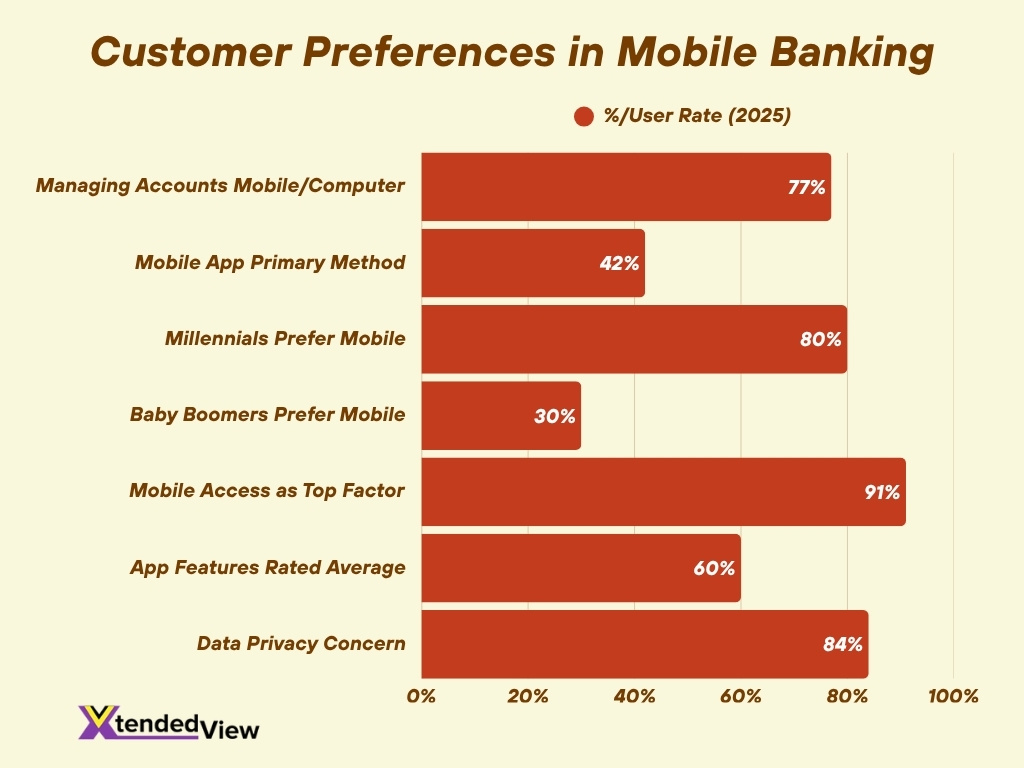

- 77% of consumers prefer managing accounts via mobile or computer in 2025.

- 42% of consumers cite mobile apps as their primary banking method.

- Among Millennials, 80% use mobile banking as their main channel, compared to 30% of baby boomers.

- 91% of consumers rank mobile access as a top factor in choosing a bank.

- Only 48% feel banks resolve mobile queries quickly.

- 60% of users rate app features as average, expecting improvement.

- 84% of consumers worry about data privacy and transparency.

Digital vs. Traditional Banking Usage

- U.S. digital banking users are projected to reach 216.8 million by 2025.

- 78% of consumers rely on mobile or online banking, and only 18% prefer branches.

- Convenience is the main driver, while branches handle complex needs.

- Mobile-first users provide banks with higher lifetime value.

- Branches remain relevant for account setup and loans.

- Digital banking reduces bank operating expenses by 20-40%.

- Hybrid banking models combining branch and digital are emerging.

Future Trends in Mobile Banking

- Integration of AI, conversational banking, and embedded finance will redefine mobile banking.

- Real-time payments, open APIs, and super-apps will expand services beyond balance checking.

- Banks and fintechs will integrate savings, investments, loans, and crypto within mobile apps.

- Hardware-based and behavioral biometrics will strengthen security.

- Mobile banking will deepen financial inclusion in underserved regions.

- Mobile wallets and contactless payments may soon dominate transactions worldwide.

Frequently Asked Questions (FAQs)

Approximately 2.17 billion people globally used mobile banking services by the end of 2025.

Around 72% of U.S. adults reported using mobile banking apps in 2025.

The global mobile banking market was valued at roughly US $1.92 trillion in 2025, growing about 28% year-on-year.

Europe’s mobile banking penetration reached about 76% in 2025, with top markets such as Norway, Denmark, and Sweden exceeding 87%.

About 89% of banks globally had launched mobile banking apps by the end of 2025.

Conclusion

The data clearly shows that mobile banking is no longer a peripheral channel; it is central to how consumers manage money globally. With broad adoption, mobile banking is enabling financial inclusion, redefining how banks deliver services, and reshaping consumer expectations. Yet, the surge in usage brings added responsibilities, from security architecture and data privacy to usability and reliability.

For banks and fintechs alike, the question is no longer whether to invest in mobile, but how to make mobile banking secure, inclusive, and future-ready. Dive deeper into each of the sections above to uncover the full scope, regional nuance,s and implications of the mobile banking wave.