The media and entertainment sector is in the midst of a significant transition, driven by changing consumer habits, technological innovation, and expanding global reach. Businesses are leveraging streaming platforms, digital advertising, and data‑driven content to reach audiences in new ways, for example, a film studio launching direct‑to‑consumer offerings, and an ad agency reallocating budget toward social video over traditional television. In this article, we’ll explore key statistics that define today’s industry landscape and invite you to dig deeper into what’s shaping the future.

Editor’s Choice

- Global entertainment & media (E&M) industry revenue reached approximately $2.9 trillion in 2024..

- The industry is projected to grow to about $3.5 trillion by 2029 at a CAGR of roughly 3.7%.

- Digital formats accounted for about 72% of global ad revenue in 2024, with a projection to rise to 80% by 2029.

- In the U.S., advertising revenue in the media sector grew by 14.9% year‑on‑year to $258.6 billion in 2024.

- The overall global media market size is forecast to reach about $2.87 trillion in 2025, up from $2.67 trillion in 2024 (CAGR ~7.5%).

- U.S. adults averaged six hours per day of entertainment time in 2025, per Deloitte’s survey.

- In 2025, advertising on social‑video platforms in the U.S. is expected to grow by around 20%, and this category is now the largest segment of digital advertising.

Recent Developments

- Generative AI and hyper‑personalisation in media are increasingly influencing how content is produced and delivered.

- Traditional pay‑TV subscriber numbers in the U.S. are predicted to drop below 50 million in 2025, which is less than half the number from a decade earlier.

- The influence of trade disputes and global supply‑chain stress is creating indirect headwinds in the media industry, especially in advertising and production.

- In the U.S., the market for immersive technologies (such as mobile AR) brought in $12.7 billion in 2024, a 15.7% increase year‑on‑year.

- The shift of major sports rights and live‑event content from linear TV to direct‑to‑consumer (DTC) and streaming models is accelerating.

- Advertisers in the U.S. will allocate over half of their $413.55 billion ad spend to media and entertainment platforms in 2025.

- Short‑form and vertical video formats are gaining traction as audience attention spans fragment and mobile usage rises.

- Live events and cinema, though challenged, remain significant contributors to overall spending, underscoring a hybrid future of digital + experiential formats.

Media & Entertainment Industry Overview

- The U.S. remains the largest national media and entertainment market, valued at approximately $649 billion, out of a global market of $2.8 trillion.

- Live entertainment events (music, theatre) and box office growth in 2023 rose by 26% and 30.4%, respectively, supporting the recovery.

- The global E&M industry is forecast to post a compound annual growth rate (CAGR) of ~3.7% through 2029.

- Outside mature markets, growth is often higher due to mobile penetration, streaming uptake, and social media reach.

- Consumer behaviour is shifting with more time spent on digital platforms, mobile devices, and connected‑TV (CTV) viewing.

- Advertising is now the dominant revenue engine for many media firms, overtaking some subscription and consumer‑spend models.

- Regulatory, economic, and macro uncertainties, such as inflation and consumer discretionary spending pressure, pose risks to growth.

Market Size & Growth Rates

- Market Growth Projection:

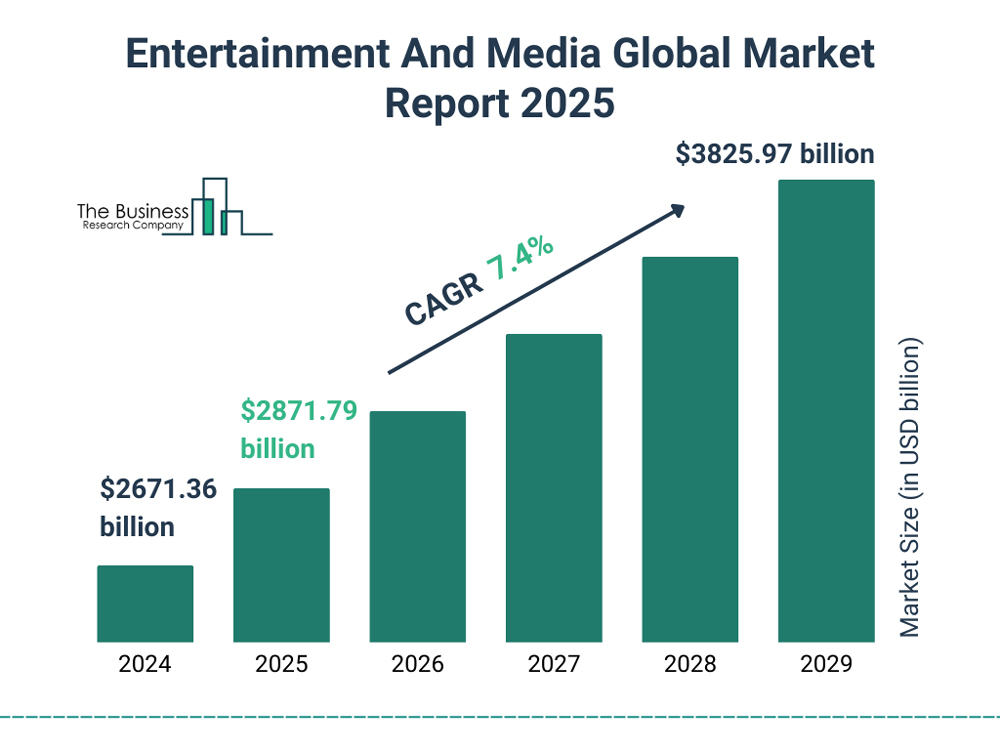

The global Entertainment and Media Market is projected to grow from $2,671.36 billion in 2024 to $3,825.97 billion by 2029. - Compound Annual Growth Rate (CAGR):

The market is expected to expand at a CAGR of 7.4% between 2025 and 2029, highlighting steady and robust growth in the sector. - Short-Term Growth (2024–2025):

The market is predicted to rise from $2,671.36 billion to $2,871.79 billion within just one year, an increase of about $200 billion. - Steady Upward Trend:

Each year from 2025 through 2029 shows continuous market expansion, reflecting consistent investment and demand across entertainment and media segments. - Long-Term Outlook:

By 2029, the market size is projected to reach nearly $3.83 trillion, signalling strong global confidence in entertainment technologies, digital media, and consumer engagement platforms.

Global Media & Entertainment Revenue

- According to PwC, the global E&M industry revenue “edged towards $3 trillion in 2024.”.

- PwC forecasts the industry will reach $3.5 trillion by 2029.

- Advertising is the fastest‑growing revenue stream, retail advertising at ~15% growth annually, social & mobile on‑stream video advertising ~15%, and connected‑TV in‑stream internet advertising ~14%.

- Offline consumer spending categories (live events, cinema) still account for 61% of spending in 2024, despite strong digital growth.

- Within the U.S., the advertising market reached $258.6 billion in 2024.

- Connectivity revenue (e.g., mobile internet access) remains the largest category, projected to reach about $1.3 trillion by 2029.

- The global video‑games segment is expected to grow from $224 billion in 2024 to nearly $300 billion in 2029.

- Digital formats are forecast to represent a growing share of total industry revenue, consistent with global shifts.

Regional Breakdown (North America, Europe, Asia‑Pacific, etc.)

- North America remains the largest region in the media & entertainment market as of 2024.

- In one forecast, for 2025, North America’s share of the global entertainment & media revenue is estimated at ~39.3% ($1,094.94 billion of $2,786.1 billion).

- Asia‑Pacific is the fastest‑growing region, forecast to reach $710 billion in 2025, with India and Southeast Asia showing strong acceleration.

- For 2024, the U.S. mobile AR market was $12.7 billion, showing growth driven by North American tech adoption.

- Europe continues to hold a substantial portion of global media revenue, though growth is slower than in emerging regions.

- According to a global report, Asia‑Pacific’s entertainment‑media industry grew to ~$9,600.59 billion in 2025 (in a specific dataset) from $6,605.2 billion in 2021.

- Middle East and Africa, while smaller in absolute size, are registering higher year‑on‑year percentage growth compared with mature markets.

- The U.S. ad market’s growth (14.9% in 2024) reflects regional momentum despite global uncertainty.

Segment Performance Overview

- The global media & entertainment industry revenue rose by 5.5% in 2024 to about $2.9 trillion from $2.8 trillion in 2023.

- Forecasts estimate a CAGR of ~3.7% through 2029, reaching around $3.5 trillion.

- One report projects the total E&M market at $3.04 trillion in 2025, growing to $3.66 trillion by 2030.

- In 2025, digital media revenue is estimated to cross $1.08 trillion, making up nearly 40% of total industry income.

- The gaming segment is expected to lead with an estimated $282 billion in revenue in 2025, showing strong growth.

- Traditional print media and broadcasting segments continue to decline, with print projected negative CAGR.

- Advertising‑driven revenue expansion is expected to account for ~55% of industry revenue growth over the next five years.

- Regions with the highest growth potential extend beyond developed markets, and many developing markets show CAGRs above 7.5%.

- Content consumption behaviour is fragmented across streaming, gaming, social media, and digital audio platforms.

Television Industry Statistics

- In May 2025, streaming platforms reached a record 44.8% share of total TV usage in the U.S., surpassing broadcast (20.1%) and cable (24.1%) combined.

- Globally, internet users spend on average 3 hours 13 minutes per day watching television across all formats.

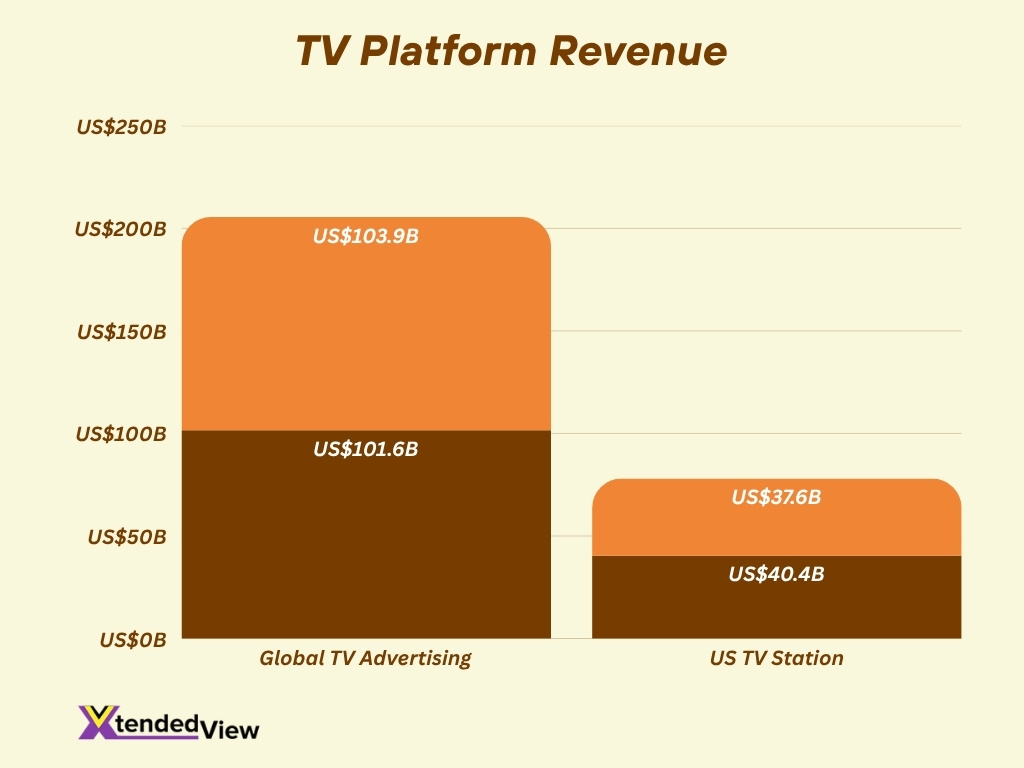

- In 2025, the global TV advertising market is projected to grow from $101.6 billion in 2024 to around $103.92 billion.

- One study estimates U.S. TV station revenue will decline 6.9% in 2025 to $37.6 billion, from $40.4 billion in 2024.

- The global television hardware market is forecast to grow from $160.65 billion in 2024 to about $164.6 billion in 2025 (CAGR ~2.5%).

- In the U.S., 71% of marketers say they are increasing their Performance TV budgets in 2025, up from 35% last year.

- The shift to connected‑TV (CTV) advertising is strong, with U.S. CTV ad spend projected at about $32.57 billion in 2025.

- 72% of adults still engage monthly with broadcast or cable TV, but younger demographics shift faster toward streaming.

- Global viewership habits indicate that while streaming grows, linear TV remains significant, with 89% of consumers watching broadcast daily and 76% watching online TV or streaming daily.

Film/Movies Industry Statistics

- The global film industry generated about $106 billion in 2025, including theatrical and digital‑first releases.

- The segment is estimated to grow at a CAGR of ~7.94% between 2025 and 2033, from roughly $101.33 billion in 2024 to $201.55 billion in 2033.

- The recovery of live theatrical revenue and global content expansion are key drivers for growth.

- Digital‑first releases, streaming windows, and hybrid release models are redefining traditional distribution chains.

- In several markets, production budgets are being maintained or increased even as distribution models evolve.

- Global film industry growth is aided by rising demand in emerging markets, especially the Asia‑Pacific, where local content and OTT platforms gain traction.

- Production costs and supply chain disruptions remain headwinds for the film segment.

- Cinema viewership patterns are shifting, with hybrid consumer behaviour combining in‑theatre and at‑home viewing now mainstream.

Music Industry Statistics

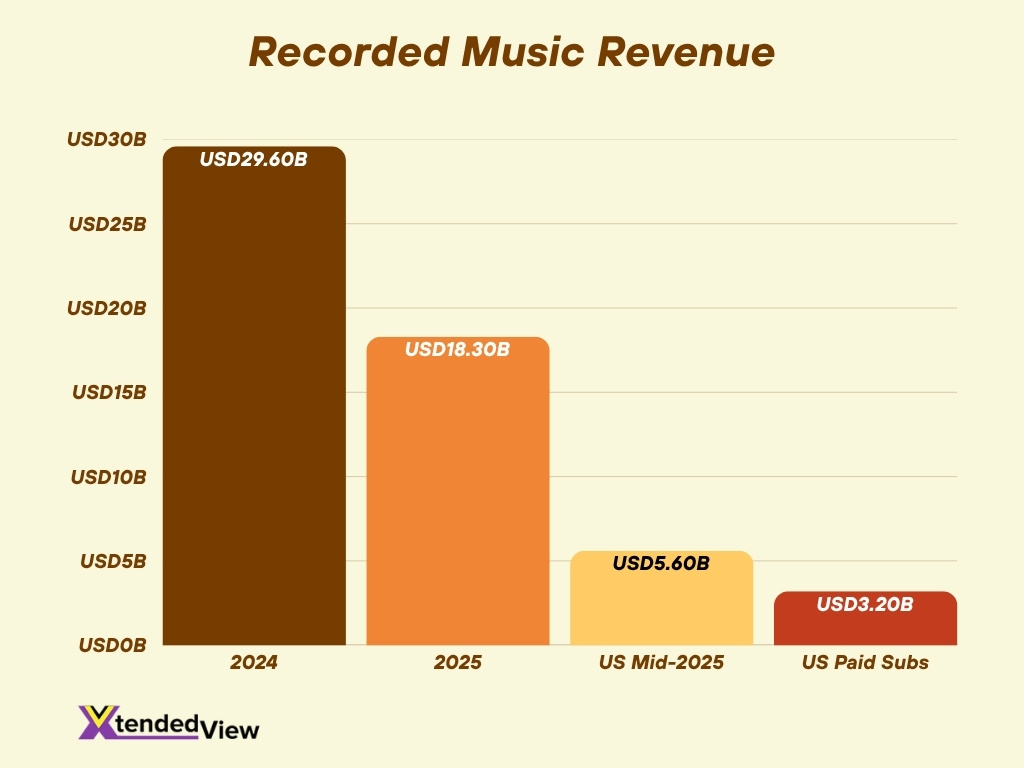

- Global recorded music revenues for 2024 reached $29.6 billion, up 4.8% from the previous year.

- In H1 2025, global recorded music revenues grew to $18.3 billion, up 5.9% year‑on‑year.

- Paid subscription streaming drove growth, increasing ~9.5%, while ad‑supported formats rose ~1.2%.

- Physical music formats declined in 2024, down 3.1% globally; vinyl continued to grow (up 4.6%).

- Music publishing revenue is forecast to grow faster than recorded music over the next five years, expected to surpass $10 billion.

- The U.S. mid‑year 2025 report showed revenue across all formats hit $5.6 billion, with paid subscriptions $3.2 billion.

- Streaming comprises the majority of recorded‑music revenue globally.

- Regional growth came from the Middle East & North Africa (+22.8%), Sub‑Saharan Africa (+22.6%), and Latin America (+22.5%).

Radio Industry Statistics

- Traditional radio listening is gradually declining in younger age groups as streaming audio and podcasts gain share.

- Advertising spend for radio is under pressure due to the migration of ad dollars to digital audio and programmatic formats.

- Some mature markets report flattening or slight declines in terrestrial radio revenues.

- Radio continues to play a strong role in local advertising, especially in smaller markets.

- Radio is integrating digital‑audio streaming and connected‑car audio to maintain relevance.

- Hybrid radio models (broadcast + streaming) are emerging to capture multiplatform audio consumption.

- Partnerships between radio networks and podcast platforms are increasing.

Print Media Statistics

- Print media (newspapers + consumer magazines) is projected to experience a –1% CAGR in revenue in 2025.

- Print media still contributed $61 billion in 2025, despite an overall decline.

- E‑books and audiobooks make up 37% of total book‑publishing sales.

- The shift from print‑based news to digital subscriptions continues as paywalls grow.

- Advertising in print formats is contracting as budgets move to digital channels.

- Print circulation is supported by niche, premium, and local‑language segments.

- Legacy publishers are investing in content‑tech, immersive formats, and community‑engagement models.

- The value of print as a licensing and archival platform remains relevant.

Digital Media Statistics

- U.S. adults average about six hours per day of media & entertainment time across formats.

- Social video platforms are increasingly challenging traditional video entertainment channels.

- Digital media revenue is projected at $1.08 trillion in 2025, nearly 40% of total industry revenue.

- 49% of U.S. consumers have a cable or satellite TV subscription, down from 63% three years ago.

- Average spending for four paid streaming services was reported at $69 per month, compared with $125 for cable/satellite.

- Digital audio, podcasts, and user‑generated content are growing strongly.

- Programmatic advertising now accounts for ~84% of all digital display ad spend in 2025.

- Over 74% of U.S. digital‑media consumption occurs via mobile apps.

- AI‑integrated content platforms generate about $86 billion in new revenue in 2025.

Streaming Services Statistics

- In May 2025, streaming services accounted for 44.8% of total US television usage, surpassing both broadcast and cable combined.

- About 83% of U.S. adults say they watch streaming services; only 36% subscribe to cable or satellite TV.

- By 2025, global streaming subscriptions are projected to surpass 1.1 billion households.

- In the U.S., approximately 88% of households have at least one video‑streaming subscription; 53% have at least four.

- The global video streaming market is estimated at $674.25 billion in 2025.

- In the U.S., consumers spend roughly $109 per month on video subscriptions and have nearly six subscriptions.

- Amazon Prime Video holds 22% of the market share, and Netflix 21%.

- Disney+ had over 126 million subscribers as of mid‑2025.

- About 28.5% of all internet users worldwide watch live streams weekly.

Social Media & Influencer Statistics

- In the U.S., 86% of marketers plan to partner with influencers in 2025.

- Influencer‑marketing spending in the U.S. will reach $10.52 billion in 2025, up about 23.7%.

- The global influencer‑marketing industry will grow by about 35.6% between 2024 and 2025.

- 80% of brands maintained or increased influencer marketing budgets; 47% raised them by 11% or more.

- About 63% of brands plan to increase influencer marketing budgets in 2025.

- Social‑media ad spend is projected to reach $276.7 billion in 2025.

- Social video platforms’ ad revenue will grow ~20% in 2025, becoming the largest digital‑ad category.

- Nearly 32% of marketers identify measuring creator performance as their largest roadblock.

- Micro‑ and nano‑influencers have the highest engagement rates.

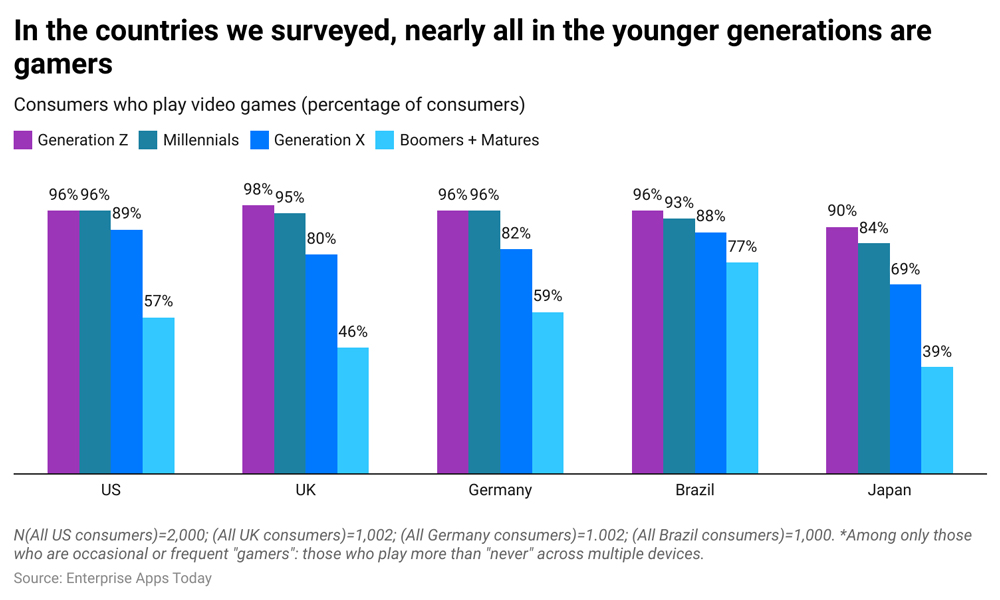

Gaming Popularity Across Generations and Countries

- Widespread Gaming Among Youth:

Across all surveyed countries, Generation Z and Millennials show near-universal gaming participation, with rates around 95–98%. - United States:

- 96% of Gen Z and Millennials play video games.

- 89% of Gen X and 57% of Boomers + Matures are also gamers.

- United Kingdom:

- 98% (Gen Z) and 95% (Millennials) actively game.

- Participation declines among Gen X (80%) and Boomers + Matures (46%).

- Germany:

- 96% of both Gen Z and Millennials are gamers.

- Drops to 82% (Gen X) and 59% (Boomers + Matures).

- Brazil:

- 96% (Gen Z) and 93% (Millennials) play games.

- Older generations remain engaged: 88% (Gen X) and 77% (Boomers + Matures).

- Japan:

- Slightly lower rates overall: 90% (Gen Z) and 84% (Millennials).

- Gen X at 69% and Boomers + Matures at 39%.

- Key Insight:

The data highlights a global generational divide; gaming is nearly universal among younger generations, while participation declines with age, though older demographics still represent a significant portion of the gaming audience.

Advertising Revenue Statistics

- Global advertising spending in 2025 is expected to grow ~7.4%, reaching about $1.17 trillion.

- Digital formats represented about 72% of overall ad revenue in 2024, with a forecast to rise to ~80% by 2029.

- Advertising is projected to account for ~55% of revenue expansion in the media & entertainment industry over the next five years.

- Advertising on social video platforms will see ~20% growth in 2025, becoming the largest digital‑ad category.

- In the U.S., major brands will allocate over 50% of ad spend to media & entertainment platforms in 2025.

- For 2024, US digital advertising revenue reached around $259 billion, up about 15% year‑on‑year.

- Traditional television advertising growth is muted; TV ad revenue is forecast to grow only ~1% in 2025 in some analyses.

- Connected TV (CTV) ad revenue jumped from 5.9% of broadcast‑TV ad revenue in 2020 to about 22% in 2024.

Consumer Spending and Behaviour

- U.S. adults spend, on average, about six hours per day on media & entertainment content in 2025.

- The digital media revenue segment is projected to cross $1.08 trillion in 2025, making up nearly 40% of the entire media & entertainment industry.

- Consumers increasingly select mobile and connected‑device access; over 74% of digital‑media consumption in the U.S. occurs via mobile apps.

- Brand trust plays a major role; about 81% of consumers indicate they need to trust a brand before making a purchase.

- In the U.S., four‑paid‑subscription bundle households pay ~$69/month, versus ~$125/month for cable/satellite alternatives.

- Many consumers now use social media as a discovery engine; the majority of Gen Z and millennials say they get content recommendations from social platforms, not just TV.

- In 2025, the majority of consumer media spending growth is filtered through advertising‑supported models rather than higher subscription fees.

- Subscription fatigue is increasing; over 52% of U.S. TV watchers feel streaming subscriptions are getting too expensive.

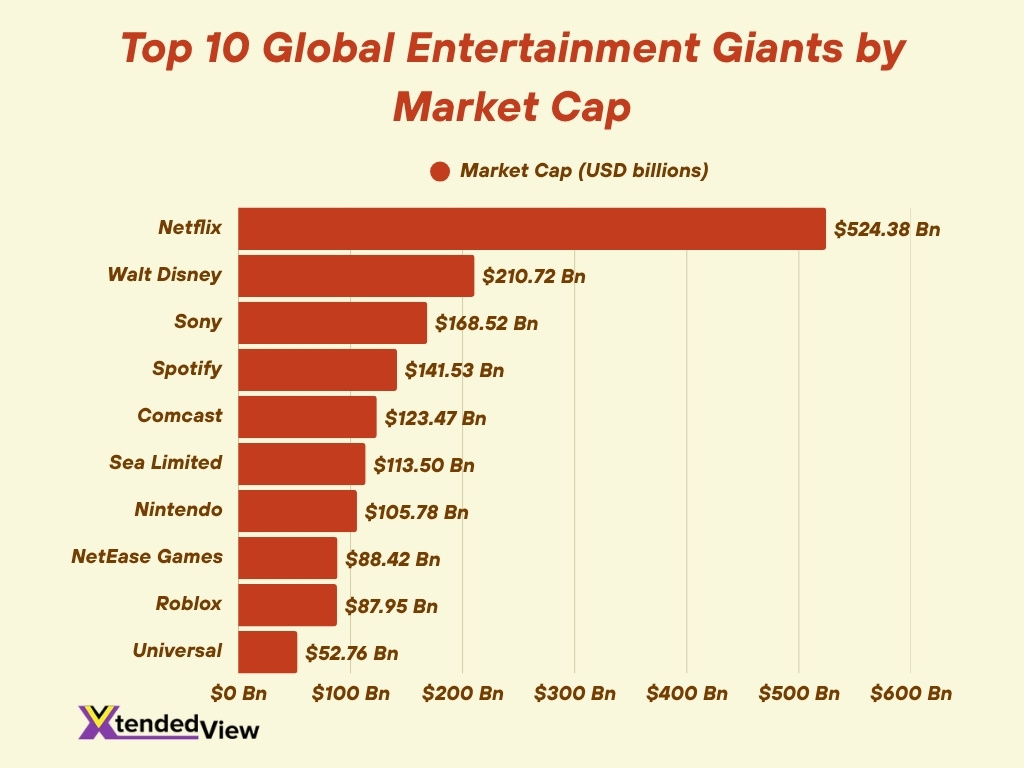

Top 10 Global Entertainment Giants by Market Cap in 2025

- Netflix leads the global entertainment industry with a staggering market cap of $524.38 billion, positioning itself far ahead of all competitors.

- Walt Disney holds the second spot at $210.72 billion, maintaining its dominance through diversified media, film, and theme park ventures.

- Sony ranks third with $168.52 billion, driven by strong performance in gaming (PlayStation), music, and entertainment technologies.

- Spotify, valued at $141.53 billion, stands as the top European company, emphasising the rise of digital music streaming platforms.

- Comcast continues to be a major U.S. player with $123.47 billion, combining traditional broadcasting with modern streaming investments.

- Sea Limited from Singapore reaches $113.5 billion, reflecting Asia’s growing influence in digital entertainment and gaming ecosystems.

- Nintendo remains a powerhouse in gaming with $105.78 billion, showcasing enduring global appeal across generations.

- NetEase Games, a key Chinese gaming company, records a market cap of $88.42 billion, highlighting China’s strong role in global gaming.

- Roblox, valued at $87.95 billion, exemplifies the growth of interactive entertainment and metaverse experiences among younger audiences.

- Universal from the Netherlands completes the top 10 with $52.76 billion, maintaining relevance through its music and film divisions.

Innovation & Technology Adoption

- Artificial intelligence (AI) is expected to transform advertising models and contribute significantly to revenue growth in the media & entertainment industry.

- Connected TV (CTV) advertising is becoming a dominant format, enhancing targeting, measurement, and ad‑personalisation across devices.

- Live‑streaming formats continue to evolve with interactive features; the live streaming industry saw growth in audience engagement and session lengths in 2025.

- Generative AI, virtual reality (VR), augmented reality (AR), and immersive experiences are increasingly adopted by media companies to enhance consumer engagement and monetisation.

- The creator economy is supported by advanced analytics and platform tools that help brands identify, manage, and measure influencer campaigns.

- Programmatic advertising and real‑time bidding in digital media are accelerating, pushing more ad spend into algorithmic models.

- Blockchain, NFTs, and tokenised fan‑engagement models are emerging in gaming and live entertainment as new revenue streams.

- Subscription models are being hybridised with ad‑supported tiers, creator‑led monetisation, and bundled services to cater to changing consumer behaviours.

Future Trends & Forecasts

- The global entertainment & media (E&M) industry is projected to grow from ~$2.9 trillion in 2024 to $3.5 trillion by 2029 (CAGR ~3.7%).

- The eSports market is forecasted to grow at a CAGR of up to ~23.3% from 2025 through 2033.

- Digital media (including streaming, gaming, and social) is expected to account for an increasing share of total industry revenue, approaching 40% by 2025.

- Advertising‑driven revenue continues as the primary growth engine; for example, retail advertising and social/mobile “on‑stream” video advertising are forecast to grow at ~15% annually.

- Streaming services are likely to face consolidation and churn pressures, forecasts suggest global SVOD & AVOD revenues to surpass $165 billion in 2025 amid fragmentation.

- Consumer‑spend growth remains constrained in mature markets (~2% CAGR for consumer categories) as subscription fatigue grows.

- Brands will increasingly prioritise micro‑moments, personalised content, and creator‑driven distribution rather than mass broadcast models.

- Regional growth hotspots include Asia‑Pacific for streaming and eSports, while mature markets shift to ad‑supported models and immersive experiences as primary growth vectors.

Frequently Asked Questions (FAQs)

The industry edged towards $3 trillion in 2024.

It is projected to grow at a compound annual growth rate (CAGR) of 3.7% until 2029.

Digital media revenue share has risen to 39.5% in 2025.

In 2024, the U.S. ad market reached $258.6 billion, with a projected value of $389.1 billion by 2029.

The market size was forecast to grow from $2,671.36 billion in 2024 to $2,871.79 billion in 2025 (CAGR ~7.5%).

Conclusion

The media and entertainment industry stands at a pivotal moment. Streaming services have overtaken traditional television in viewership. Social media and influencer marketing budgets are accelerating. eSports and gaming are scaling into major commercial channels. Advertising, especially digital and AI‑powered formats, is emerging as the fuel for future growth. Meanwhile, consumer behaviour is more fragmented, digital‑first, and value‑driven than ever.

Companies that balance innovation, precise targeting, and operational agility are best positioned to thrive. As you dive further into the data and implications, you’ll uncover how these shifts are reshaping global media dynamics.