The cyber insurance sector has become a critical pillar of risk strategy as organizations confront escalating digital threats. In recent years, businesses across industries, from finance and healthcare to manufacturing, have turned to specialized coverage to mitigate the impacts of data breaches and ransomware attacks. For example, a multinational bank used cyber liability insurance to cover legal, forensic, and notification costs after a phishing attack, and a regional hospital leveraged coverage to reimburse patient‑notification and system‑recovery costs following a malware incident.

Editor’s Choice

- Global cyber insurance premiums are projected at around $16.3 billion in 2025.

- CAGR of 14.2% forecast for the industry from 2025 to 2030, reaching $32.2 billion by 2030.

- Only 47% of eligible organizations currently hold cyber‑insurance policies, indicating a large coverage gap.

- Premiums in the U.S. dropped by about 7% in Q1 2025, marking the 10th consecutive quarterly decline.

- SME market penetration remains extremely low, below 10% in many regions in 2025.

- The share of global premiums from North America stands at around 70%, with Europe at 19% and APAC at 8%.

- Underwriting trends show increased use of AI and predictive analytics by cyber‑insurers in 2025.

Recent Developments

- Cyber insurance rates declined 5-15% in early 2025 amid softening market conditions.

- Global cyber insurance premiums are expected to reach $15.6 billion in 2025.

- 85% of cyber insurers use AI for real-time risk assessment in 2025 underwriting.

- Contingent business interruption accounted for 15% of large cyber claims (>€1mn) in H1 2025.

- SME cyber insurance adoption surged 52% driven by AI risk tools in 2025.

- 64% of cyber policies now include AI-based clauses for continuous monitoring in 2025.

- Cyber insurance market projected to grow 15% in 2026 amid AI threats.

- Bundled cyber services like MDR and phishing simulations are increasingly offered by carriers in 2025.

- Parametric cyber products using AI enable 65% faster claims processing in 2025.

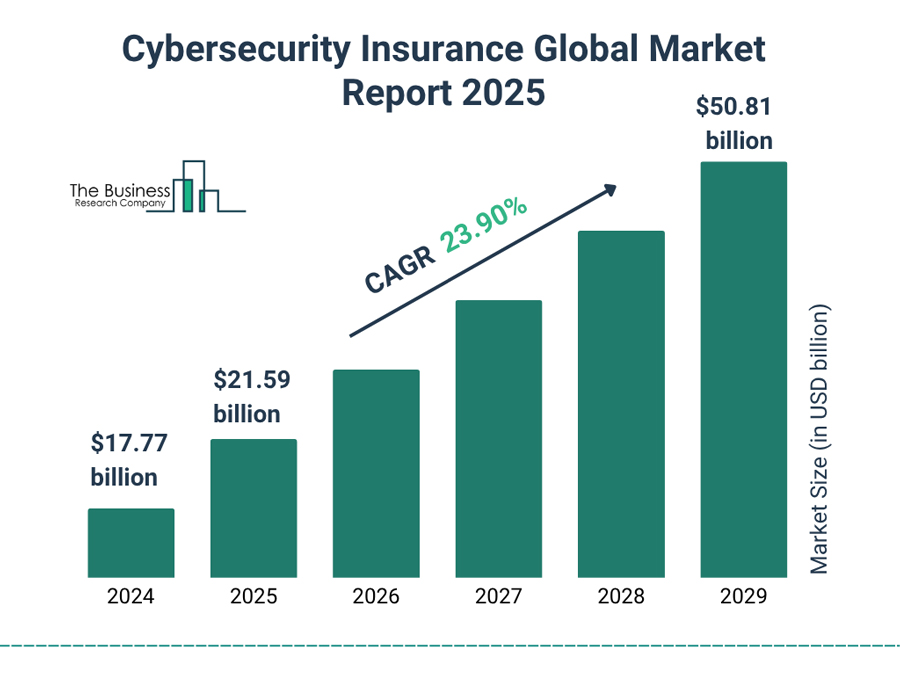

Cyber Insurance Market Overview

- The global cyber insurance market is expected to have gross premiums of about $16.3 billion in 2025.

- According to one projection, the sector will more than double from $16.54 billion in 2025 to $32.19 billion by 2030 (CAGR 14.2 %).

- Some analysts estimate the global market could reach as much as $19.97 billion in 2025, climbing to $106.4 billion by 2035 (CAGR 18.2 %).

- The U.S. remains the dominant region, accounting for roughly 70% of global premiums in 2025.

- Europe follows with approximately 19% of global cyber insurance premiums, and Asia–Pacific about 8%.

- Despite growth, cyber insurance still represents less than 1% of total global property/casualty insurance premium volumes.

- Market observers describe the industry as early‑stage but maturing, with infrastructure and underwriting models gaining sophistication.

- A large protection gap remains; many organizations exposed to cyber risk remain uninsured or underinsured.

Market Size and Growth Trends

- In 2024, the global cyber insurance market was estimated at $15.3 billion.

- Growth projections suggest the premium volume will reach $16.3 billion in 2025, representing year‑on‑year growth of 6.5%.

- One forecast puts the market size in 2025 at $16.54 billion, remarking the doubling to $32.19 billion by 2030.

- The sector has seen a compound annual growth rate (CAGR) of over 10% in recent years, according to some reports.

- Some estimates from 2020 suggested growth from $7.8 billion (in 2020) to $20.4 billion by 2025 (CAGR 21%).

- The growth trajectory is driven by increasing digitalization, more frequent cyberattacks, and regulatory pressure.

- Regional growth differs markedly Asia Asia-Pacific is expected to post higher growth rates than North America in the forecast period.

- The decade‑long horizon may see the market reaching $60 billion by 2040 in some scenarios.

Cyber Insurance Adoption Rates

- A recent study found that only around 47% of eligible organizations currently hold a cyber insurance policy.

- Among smaller businesses (SMBs), the penetration is far lower; many regions report below 10% coverage.

- In the U.S., one statistic states that 65% of businesses now have cyber insurance by 2025.

- However, in earlier years, only 21% of small businesses had a policy; this shows adoption is uneven.

- A 2025 UK commercial‑insurance broker survey found 60.8% of SMEs in the UK do not hold cyber cover.

- A lack of clarity is another barrier; only 25% of senior technology leaders said policy terms were “very clear” in their firms.

- Many organizations cite that they believe “they will not be a target” (40.5% of SMEs in one UK survey) as a reason for not adopting coverage.

- One article states that adoption rates have grown significantly across industries but still lag in many sectors.

Premium Trends and Costs

- In the U.S., cyber insurance pricing dropped about 7% in Q1 2025, marking the 10th consecutive quarter of rate declines.

- For 2024, the U.S. cyber insurance market saw premiums written decline 2.3% to $7.075 billion.

- Some projections forecast premiums growing from $15.1 billion in 2024 to $27 billion by 2030.

- While rate competition persists, insurers warn that emerging risks (such as AI‑related attack vectors) may pressure pricing upward.

- In 2025, many market watchers describe conditions as “buyer‑friendly” with ample capacity and downward pressure on rates.

- Industry data shows broader commercial‑insurance rate averages fell 3% in Q1 2025, following a 2% decline in Q4 2024.

- Some sectors are seeing selective rate increases (for example, after ransomware exposure) despite the overall downward trend.

Common Types of Cyber Insurance Coverage

- Data breach response coverage, legal, notification, forensic, and public‑relations costs.

- Business interruption coverage tied to cyber incidents and system outages.

- Cyber extortion/ransomware coverage, including payments, negotiator fees, and recovery costs.

- Network liability coverage for liabilities to third parties (for example, the data of customers).

- Privacy & regulatory fines coverage, especially with evolving regulations (e.g., GDPR, NIS2).

- Reputational harm and crisis management services are often included in modern policies.

- First‑party property damage/system restoration following malicious attack or failure.

- Supply‑chain risk / contingent business interruption coverage is becoming more common as attacks cascade across vendors.

Cyber Insurance Claims Statistics

- The U.S. cyber insurance market recorded 33,561 claims in 2024.

- In 2024, third‑party related attacks accounted for 31% of all cyber claims and 24% of material losses.

- Loss severity remains significant; global insured losses per claim are typically US$115,000 or more.

- In the first half of 2025, around 60% of the value of large cyber claims in Europe stemmed from ransomware events.

- Data exfiltration now appears in 40% of large‑loss cyber claims in H1 2025, up from 25% in 2024.

- A claims study by NetDiligence covered over 10,000 cyber insurance claims (2020‑2024).

- In the 2013‑2019 period, around 73% of claims were for breach response and crisis management.

- Approximately 27% of data breach claims and 24% of first‑party claims across that earlier period had exclusions or partial non‑payouts.

Key Drivers of Cyber Insurance Demand

- The average global cost of a data breach in 2024 reached US$4.9 million, marking a 10% year‑on‑year increase.

- 45% of organizations expect significant supply‑chain cyber‑attacks by 2025.

- Regulatory pressure and compliance obligations are pushing firms to buy cover.

- Growing digitalization and remote‑work practices increase exposure and thus demand.

- Insurers now often require improved cybersecurity controls as a condition of coverage.

- The protection gap for small and mid‑sized enterprises remains a primary driver of new interest.

- News of high‑profile losses promotes insurance uptake among peer organizations.

Ransomware and Cyberattack Trends

- 38% of global ransomware attacks targeted the United States in 2025.

- The average cost of a data breach globally in 2025 is US$4.67 million, with the U.S. average at US$9.6 million.

- Ransomware payouts in 2025 have averaged US$1.76 million per incident.

- 91% of successful attacks in 2025 started with a phishing email.

- The cost of software supply‑chain attacks is anticipated to reach US$138 billion by 2031.

- 40% of large‑loss claims in H1 2025 included data theft/exfiltration.

- 78% of organizations worldwide reported at least one cybersecurity incident in the past 12 months.

- 29% of micro‑businesses experienced ransomware attacks.

Sector‑wise Adoption (SMBs, Enterprises, Industries)

- In 2025, only 17% of small businesses have cyber insurance coverage.

- Among U.S. businesses, 65% reported having cyber insurance policies.

- 94% of enterprises (1,000+ employees) now carry cyber insurance, compared to 66% of SMBs.

- SMEs account for only 30% of cyber insurance premiums.

- Healthcare, finance, and manufacturing represent over 60% of the market growth.

- California holds approximately 11% of total cyber policies, followed by Texas (9%) and New York (8.5%).

- Telehealth and cloud services providers saw premium increases of 22% in 2025.

- 33% of new policies in 2025 were bundled with security services.

Regional Insights and Global Penetration

- In 2025, global cyber insurance premiums reach about US$15.6 billion, with North America at 66%, Europe at 21%, and Asia‑Pacific at 10%.

- Asia‑Pacific is expected to post the highest regional CAGR in the mid‑term.

- SME cyber insurance penetration in Australia is below 10%.

- The global market will more than double from US$16.54 billion in 2025 to US$32.19 billion by 2030.

- Emerging markets remain underpenetrated but are gaining traction.

- Global cyber insurance rates fell by 6% in Q4 2024.

- Europe’s share is expected to increase from 21% in 2024 to around 24% by 2027.

Regulatory and Compliance Impact

- U.S. laws like CIRCIA contributed to a 20% growth in policy adoption in 2025.

- GDPR fines exceeded €1.6 billion in 2025, spurring interest in cyber policies.

- 36 countries now have mandatory cyber incident reporting laws.

- 48% of enterprise cyber policies in 2025 include regulatory-tech integration.

- 81% of companies cited data‑privacy laws as a key reason for insurance adoption.

- Underwriters now enforce controls tied to regulatory benchmarks.

- Regulatory changes in Australia triggered a 41% increase in mid‑2025 policy uptake.

Cybercrime Statistics Linked to Insurance

- Global cybercrime cost projected at $10.5 trillion in 2025.

- 63 % of organizations lacked a formal AI governance policy at the time of breach.

- 97 % of AI-related breaches lacked proper AI access controls.

- 53 % of breaches involved customer PII.

- The average breach lifecycle in 2025 was 241 days, the shortest in nine years.

- 30 % of large-loss events involved multi-environment data.

- Small firms without robust controls spent 13.4 % more on breach management.

- BEC and FTF now account for 60 % of insurance claims.

Cost of Data Breaches and Financial Impact

- Global average breach cost in 2025 fell to $4.44 million.

- U.S. average breach cost hit $10.22 million.

- Public sector average breach cost rose to $2.86 million.

- Organizations with automation/AI saved $1.9 million on breach costs.

- Multi-environment breaches averaged $5.05 million.

- The industrial sector breach cost was $5.56 million in 2024.

- Breaches taking over 200 days cost $5.46 million vs $4.07 million.

- Indirect breach costs continue to drive high impact even as averages fall.

Most Common Claims and Loss Events

- Ransomware claims dropped 7 % but retained high severity.

- BEC and FTF drive 60 % of claims.

- The average ransomware attack cost in 2025 is $5.5–6 million.

- Business interruption losses among SMEs up 72 %.

- Litigation settlements for SMEs up 74 %.

- Third‑party vendor incidents surged.

- 83 % of denied claims were due to unpatched vulnerabilities.

- Most attacks now use stolen credentials, not system hacks.

Cyber Insurance Underwriting Trends

- 48 % of underwriters expect premium increases in 2025.

- Insurers require MFA, EDR/MDR, and vendor risk hygiene.

- Higher limits are more accessible than in prior years.

- Underwriters now assess vendor concentrations.

- Risk-control services are increasingly bundled in policies.

- Systemic risk from vendor aggregation is now monitored.

- Healthcare and infrastructure sectors may face hardened rates.

Exclusions and Limitations in Coverage

- 91 % of cyber policies exclude nation-state attacks.

- 83 % of denied claims are linked to unpatched vulnerabilities.

- 49 % exclude social-media defamation.

- 41 % of industrial-sector plans exclude IoT-related risks.

- Only 38 % include privacy-related fine coverage.

- 59 % restrict policy stacking.

- Ransom sub-limits are often half the policy total.

- Non-compliance with controls may void coverage.

Challenges Facing the Cyber Insurance Market

- Modeling accumulation and contagion risk remains difficult.

- Many SMBs remain uninsured.

- New AI threats challenge underwriting accuracy.

- Standardizing policy terms may reduce flexibility.

- Loss data is fragmented and scarce.

- Systemic risk in SaaS environments is poorly priced.

- Policy misunderstanding causes disputes.

- Rate softness competes with the need for proper pricing.

Frequently Asked Questions (FAQs)

The global cyber insurance market is expected to reach $16.3 billion in 2025.

The market is forecast to grow at a 14.2% CAGR from 2025 to 2030.

North America accounts for approximately 70% of global cyber insurance premiums.

Only 25% of senior technology leaders report that their cyber insurance policy terms are very clear.

The penetration of cyber insurance among SMEs remains below 10% in many markets in 2025.

Conclusion

As the cyber insurance market enters, the industry finds itself at a crossroads. The average cost of data breaches has slipped slightly, yet the scale and complexity of cyber threats continue to climb. While insurers are offering more favourable rate conditions and increased capacity, organisations must remain alert to the coverage gaps, exclusions, and underwriting conditions that can significantly alter outcomes when a breach happens. For businesses of all sizes, but especially SMBs, the window to evaluate coverage, strengthen controls, and understand their policy terms has never been more critical.