The world of smartphones remains dominated by the iPhone ecosystem, and understanding its performance offers rich insight into consumer behaviour, technological shifts, and market dynamics. For instance, enterprises deploying mobile apps are adapting to changes in the iPhone user base to optimise monetisation strategies, while telecom carriers tailor upgrade plans based on iPhone replacement cycles. In this article, we explore up‑to‑date statistics around the iPhone’s global footprint, share volume, and market share, inviting you to dig deeper into each dimension.

Editor’s Choice

Here are the key statistics at a glance:

- 1.56 billion active iPhone users worldwide are projected in 2025.

- More than 3 billion iPhones have been sold since 2007.

- Global mobile OS market share for iOS is at ≈ 24.4% in 2025.

- iPhone shipments by Apple Inc. grew 10% year‑over‑year in Q2 2025.

- iPhone ASP (average selling price) reached ≈ $987 in 2025.

- U.S. smartphone market share for iOS is at ≈ 58% in 2025.

- Emerging markets such as India saw iPhone growth of 34% YoY in 2025.

Recent Developments

- Apple introduced the iPhone 17 Pro and iPhone 17 Pro Max in September 2025, featuring the A19 Pro chip and advanced camera modules.

- The new standard model, iPhone 17, also launched with upgraded specs, including a 48‑MP dual‑fusion camera and 120 Hz display.

- Apple’s global shipments of iPhones rose about 10% YoY in Q2 2025, marking a June‑quarter record.

- In 2025, the U.S. smartphone market is expected to grow by 3.6%, and the Middle East & Africa by 6.5%, helping offset declines in China.

- The total iPhone user base is forecast to reach approximately 1.56 billion by 2025.

- The average selling price (ASP) of an iPhone climbed to about $987, signalling strong demand for premium models.

- Apple’s milestone of 3 billion iPhones sold since launch underscores sustained global appeal.

- The new iPhone models increasingly integrate on‑device AI and advanced connectivity, shifting enterprise and consumer expectations.

- In late 2025, Apple emphasised enhanced trade‑in offers and carrier‑upgrade strategies to maintain retention against economic headwinds.

- Increased regulatory and supply‑chain pressures (tariffs, component shortages) remain a backdrop to recent developments in the iPhone business.

Global iPhone User Statistics

- Active iPhone users worldwide are projected to be ≈ 1.56 billion in 2025.

- In 2024, the user base was estimated at 1.46 billion, implying growth of about 7% year‑over‑year.

- In the United States, there were 135.97 million iPhone users (≈ 40% of the U.S. population) as of the latest data.

- Global smartphone users reached about 4.88 billion in 2024 (60% of the world population).

- If 1.56 billion users represent 20% of the global population in 2025, that reinforces iPhone’s position in the premium segment.

- The global share of iPhone users rose from 17.03% in 2023 to 19.08% in 2025.

- In developing regions, rising middle‑class incomes and 5G rollout contribute to iPhone user growth.

- The pace of user growth is decelerating in mature markets (U.S., Western Europe) but remains robust in Asia and MEA regions.

- The installed base of Apple devices (all types) reached 2.35 billion in early 2025.

- User retention and ecosystem lock‑in remain high for iPhone users, supporting the large renewal base for Apple.

iPhone Sales Volume and Trends

- More than 3 billion iPhones have been sold since the first launch in 2007.

- In 2023, global iPhone shipments totalled 231.8 million units.

- For the twelve months ending June 30, 2025, Apple’s total revenue was $408.6 billion (≈ 5.97% increase YoY).

- Google Trends data shows a spike for “iPhone sales” in August 2025, aligning with launch cycles.

- Premium models (e.g., iPhone 15 Pro Max) contributed over $38 billion to H1 2025 iPhone revenue.

- The base model transition (entry‑level vs. Pro) is accelerating, with more buyers opting for higher‑spec versions.

- Unit volume in mature markets is slower, growth increasingly driven by replacement cycles and expansions in emerging markets.

- The COVID‑era surge in sales has given way to more steady growth rates in 2025, suggesting market saturation in some regions.

- Apple’s trade‑in and carrier financing programmes are influencing sales volume more than pure unit growth.

- Seasonal peaks remain around launches (September) and holiday quarters, with varying regional demand shifts.

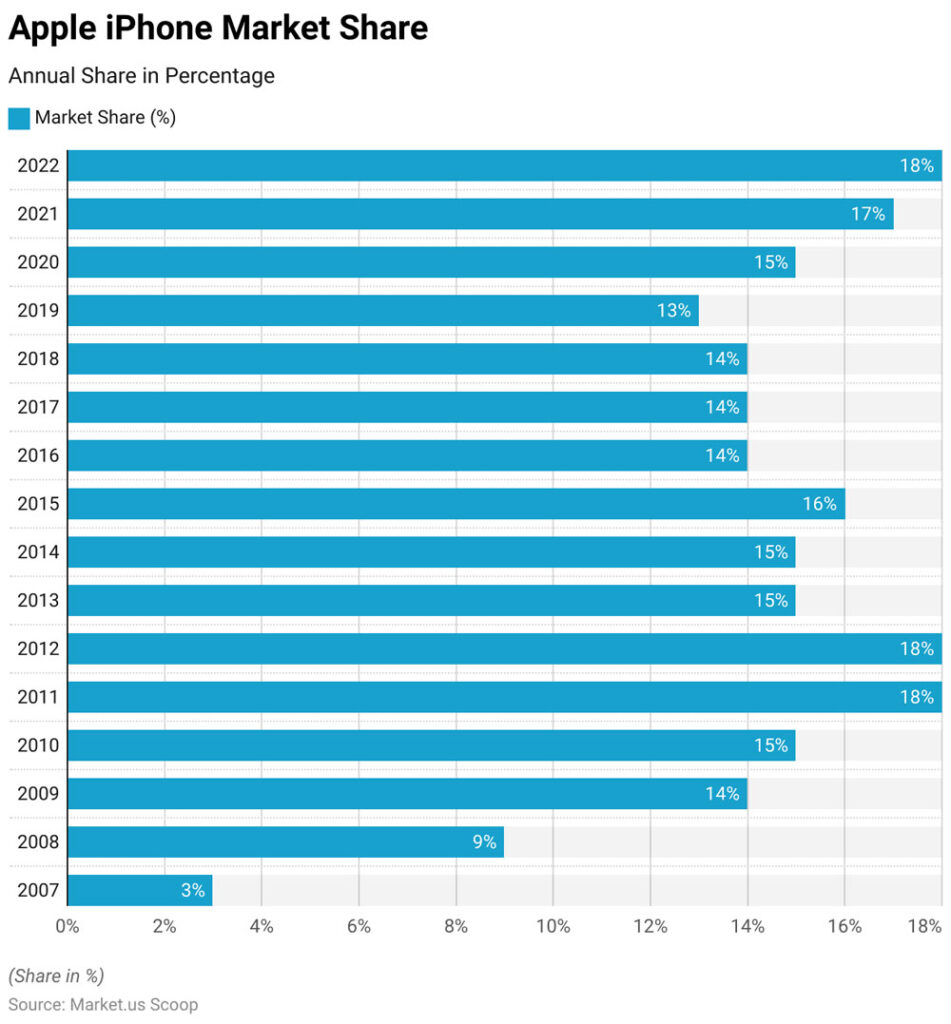

iPhone Market Share Worldwide

- Apple’s iPhone market share has fluctuated between 3% and 18% over the years.

- The highest recorded market share was 18%, achieved in 2011, 2012, and 2022.

- The lowest share was 3% in 2007, the year the first iPhone launched.

- 2008 saw significant growth, rising to 9%, tripling its debut figure.

- From 2009 to 2016, Apple maintained a steady range between 14% and 16%.

- 2020–2022 marked a consistent upward trend, from 15% in 2020 to 18% in 2022, showing strong recovery and growth post-pandemic.

- Between 2017 and 2019, the share remained relatively flat at 13–14%, indicating market stabilisation during that period.

iPhone Market Share by Country/Region

- In the U.S., about 58.1% of mobile phone users are on iPhones.

- In Canada, iPhone market share is 60.47%.

- In Denmark, iPhone enjoys 65.75% share of mobile devices.

- In Japan, iOS usage is 68.75% of all mobile devices.

- In India, iOS share remains modest (3.11%) while Android dominates (96.67%).

- The Middle East & Africa regions are growing faster (≈ 6.5% in 2025), though the absolute iPhone share remains lower.

- China presents a challenging market, and Android holds 77.44% vs. iOS 21.81% in 2025.

- In markets with strong carrier financing, adoption of iPhones tends to be higher due to upgrade incentives.

- Regional variation reflects income levels, device pricing, and local brand preferences, meaning share gains aren’t uniform globally.

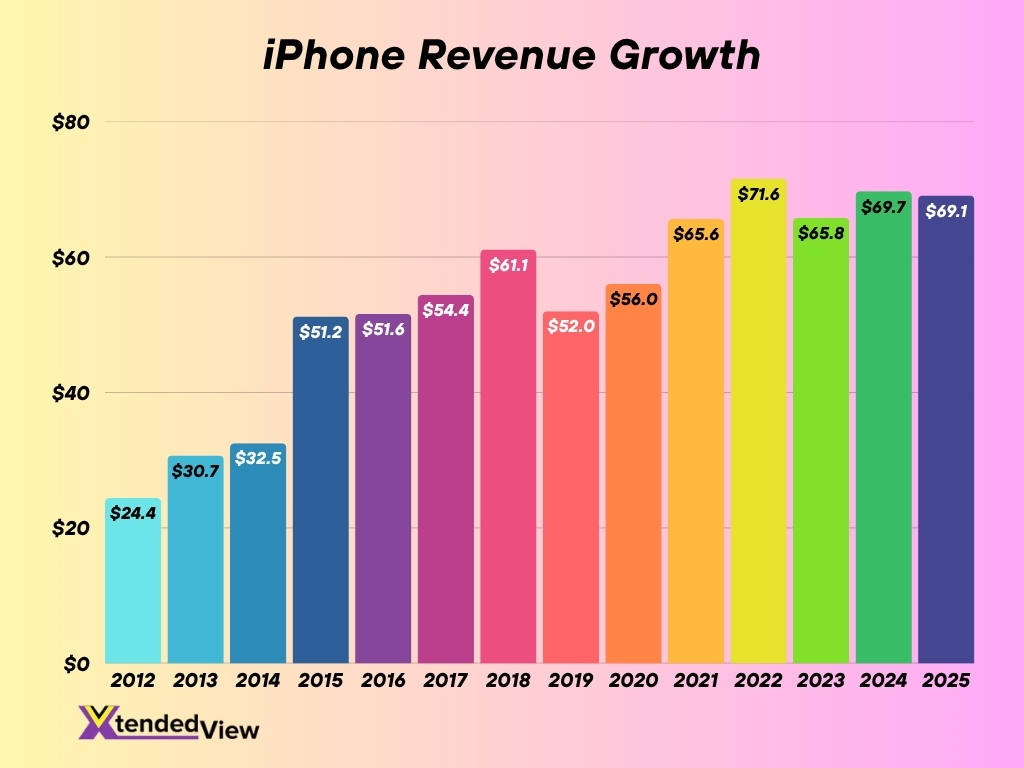

iPhone Revenue Growth

- Apple’s Q1 iPhone revenue has shown a strong upward trend from $24.4 billion in 2012 to $69.1 billion in 2025.

- Between 2012 and 2015, revenue more than doubled, jumping from $24.4B to $51.2B, marking the iPhone’s early explosive growth phase.

- Revenue peaked significantly at $61.1B in 2018, reflecting the iPhone X launch impact and high consumer demand.

- After a slight dip to $52B in 2019, Apple rebounded with $56B in 2020, showing steady recovery.

- The company achieved record-breaking Q1 revenue of $71.6B in 2022, the highest in the dataset, driven by strong iPhone 13 sales and global demand resilience.

- The following years remained stable and high, with $69.7B in 2023, $69.7B in 2024, and a slight dip to $69.1B in 2025, suggesting market maturity.

- From 2012 to 2025, Apple’s Q1 revenue grew by over 180%, underscoring its sustained dominance in the premium smartphone market.

iPhone User Demographics

- The active iPhone user base worldwide is estimated at ≈ 1.561 billion in 2025, up from 1.462 billion in 2024.

- In the U.S., around 150.7 million users are on iPhones as of 2025.

- Among iPhone users globally, about 43% are aged 18‑34 years, while older age brackets represent smaller shares.

- Surveys suggest the average income of an iPhone user is higher than that of comparable Android users; one estimate points to US $85,000 vs US $61,000.

- Brand loyalty remains strong, and iPhone user retention often exceeds 90% when owners upgrade within Apple’s ecosystem.

- In the U.S., among the 25‑34 age group, approximately 63.3% of smartphone users use iPhones, significantly above the national average of 48.2%.

- Female users globally show a slightly higher adoption of iPhones compared to male users; one data point indicates 31% female vs 28% male among certain age brackets.

- In 2024, around 83% of U.S. teens reportedly owned an iPhone.

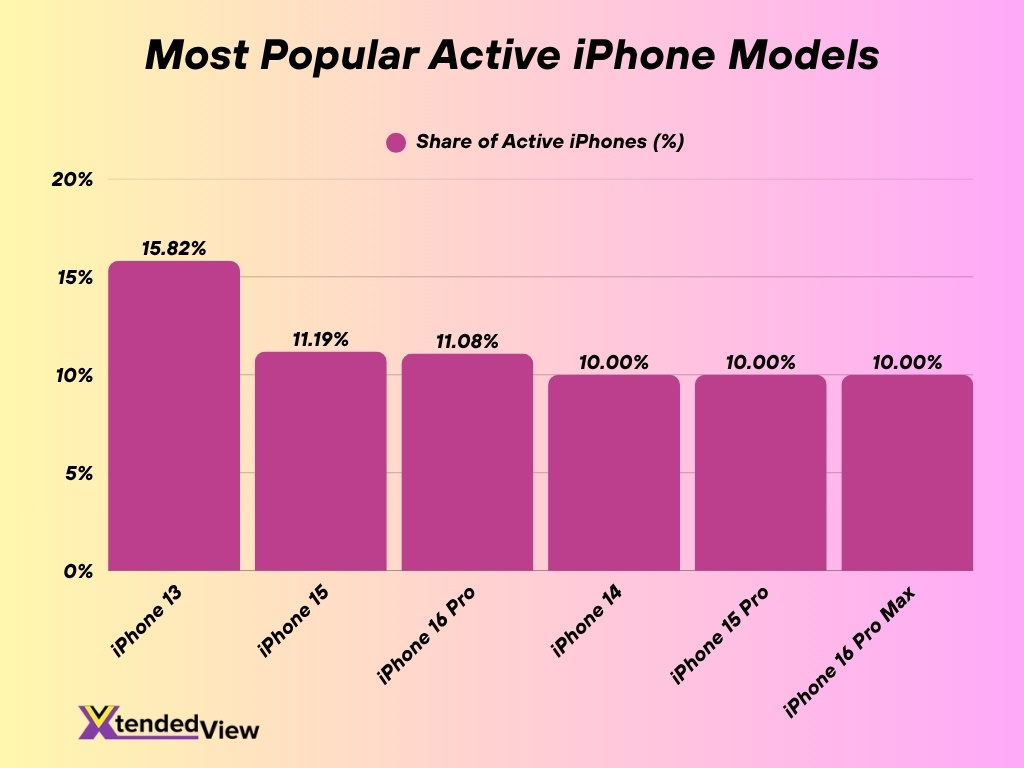

Most Popular iPhone Models

- According to a usage survey in September 2025, the iPhone 13 accounted for approximately 15.82% of all active iPhones.

- The iPhone 15 and iPhone 16 Pro each held around 11.19% and 11.08%, respectively, of usage share as of late‑September 2025.

- Models such as the iPhone 14, iPhone 15 Pro, and iPhone 16 Pro Max lagged slightly below 10% usage share each in the same period.

- The trend suggests that older models (e.g., iPhone 13 and 14) continue to maintain a substantial installed base even after newer releases.

- Premium “Pro” variants are gaining ground but still represent a smaller fraction of the total active base compared to mainstream models.

- The popularity of specific models aligns with trade‑in and carrier upgrade incentives present in many markets.

- Model popularity varies regionally; in cost‑sensitive regions, older or lower‑tier models maintain a stronger market presence.

- Model diversity also reflects longer upgrade cycles and users keeping devices longer before migrating to the latest release.

iPhone Usage Patterns

- In 2024, the App Store ecosystem (serving iPhone users) facilitated nearly US $1.295 trillion in billings and sales globally.

- Day 1 retention rate for iOS apps averaged roughly 27%, dropping to approximately 13% at Day 7 and 7% by Day 30.

- iPhone users tend to launch a relatively small number of apps weekly; historical studies found 14‑18 apps regularly engaged by most users.

- A survey of U.S. iPhone owners found 51% said they were “extremely likely” to upgrade their device in the next 12 months.

- Among iPhone users, 80% remained loyal to Apple’s ecosystem after their first device, with just 8% making a permanent switch to another platform.

- Global app‑store downloads continue to grow, driven by increased mobile commerce, streaming, gaming, and productivity usage on iPhones.

- Emerging markets show rising usage intensity, and iPhone users in those regions demonstrate higher engagement in digital services, not just device ownership.

- The increasing shift toward services (e.g., streaming, mobile payments) via iPhones underscores a transition from simple device use to broader ecosystem interaction.

iPhone Upgrade and Retention Rates

- Apple’s iPhone owner retention rate often exceeds 90%, meaning most users stay within the Apple ecosystem when they upgrade.

- In 2025, smartphone loyalty in general was estimated at ≈ 89%, with Apple outpacing many rivals.

- Trade‑in programs show that approximately 74.6% of iPhone trade‑in users stayed within Apple’s ecosystem at upgrade time.

- Studies indicate that only 18% of iPhone upgraders reported doing so because of new features, with most citing phone age or functional issues.

- In the U.S., 60% of surveyed iPhone users reported their current device was over three years old, indicating longer use cycles.

- Surveys show 84% of iPhone owners intend to purchase another Apple device the next time they upgrade.

- While global upgrade rates vary by region, the consistent factor is high ecosystem retention; carriers and retailers often leverage this in upgrade offers.

- Analysts view the strong retention/upgrade dynamics as a strategic asset for Apple, enabling predictable replacement cycles and recurring revenue in services.

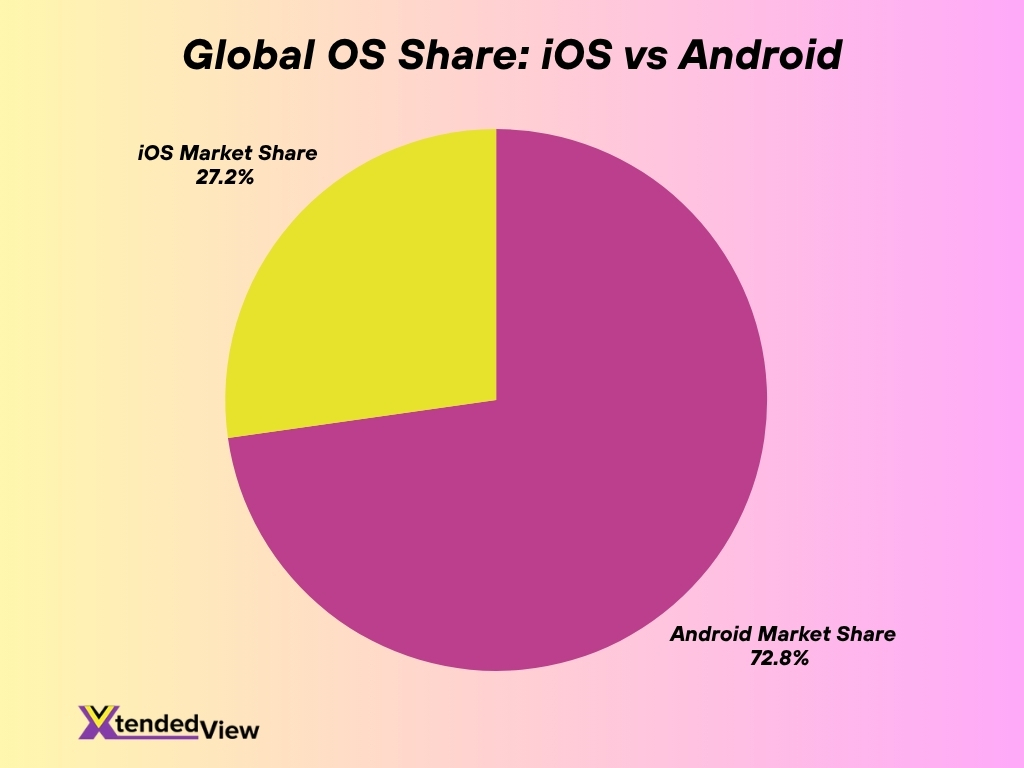

iOS vs Android Statistics

- Globally in 2025, the Android operating system holds approximately 72.47% of the smartphone market, while iOS holds around 27.11%.

- In the U.S., iOS leads with around 57.97% market share in 2025, compared to Android.

- One source estimates iPhone users globally will represent 19.08% of all smartphone users in 2025.

- Surveys show younger generations (e.g., Gen Z, Millennials) are more likely to own iPhones, while older generations are more evenly split or lean toward Android.

- Retention rates, Android users reportedly show 89‑91% loyalty, while iPhone users’ loyalty ranges 85‑88% in some studies.

- Approximately 47% of former Android users cited the iPhone as offering a “better user experience”.

- Affordability remains a key factor; 29% of former iPhone users switched to Android, citing cost.

- From a developer and app revenue perspective, iOS users generate higher average spend per user than Android users, a driver for businesses targeting iPhone users.

iPhone App Store Statistics

- The App Store ecosystem on iPhones facilitated nearly US $1.295 trillion in global billings and sales in 2024.

- Users are projected to download over 92 billion apps from the App Store in 2025, up from about 35.4 billion in 2024.

- The App Store is expected to generate $138 billion in revenue globally in 2025, representing 16.9% growth year‑over‑year.

- As of 2025, there are approximately 2,026,580 apps available on the App Store.

- Of those apps, around 1,931,115 (≈ 95.35%) are free, and 94,204 (≈ 4.65%) are paid.

- The daily publication rate, an average of 1,647 new apps are introduced to the App Store each day.

- The United States accounts for 42% of App Store revenue, with about 35% coming from the U.S. alone.

- In‑app advertising on iOS devices grew by 131% from 2019 to 2024 within the App Store ecosystem.

- Over the last five years (2019‑2024), the App Store ecosystem more than doubled in size (+150%+), driven by growth in digital goods, services, and m‑commerce.

- Of all billings & sales in the App Store in 2024, ≈ 78% (US $1,014 billion) came from physical goods and services, 10% (US $131 billion) from digital goods/services.

Why it matters: For businesses developing for iPhones, this means the App Store remains a major revenue channel, with free apps dominating installs but paid/subscription models and physical‑goods integrations driving value.

iPhone Price Trends

- In the U.S. in 2025, the top‑tier model (iPhone 16 Pro) was priced at US $1,079.

- In many other countries, equivalent models cost significantly more when adjusted for currency and taxes, yielding wide global variation in pricing.

- In India in 2025, the launch price for the iPhone 17 Pro Max stood at Rs 1,49,900.

- The resale‑value retention for older flagship iPhones remains strong, e.g., the iPhone 13 Pro retained 69% of its new value in Q1 2025.

- Price slashes for previous‑generation models are already seen ahead of the iPhone 17 launch, indicating downward pressure on older models.

- The “premium” smartphone segment (above US $700) is growing fastest, enhancing pricing power for iPhones, which operate largely in that tier.

- Discounting of older iPhones, particularly in emerging markets, is supporting volume growth, even as premium launch prices remain elevated.

- Some markets now pay 20‑30% more for the same model compared to U.S. pricing, due to local taxes, tariffs, and exchange rates.

- Despite a global economic slowdown, average selling prices (ASPs) for iPhones remain stable or rising, reflecting a focus on premium upgrades.

- For consumers and resellers, timing matters, launch windows, trade‑in offers, and regional pricing differences shape the cost of ownership.

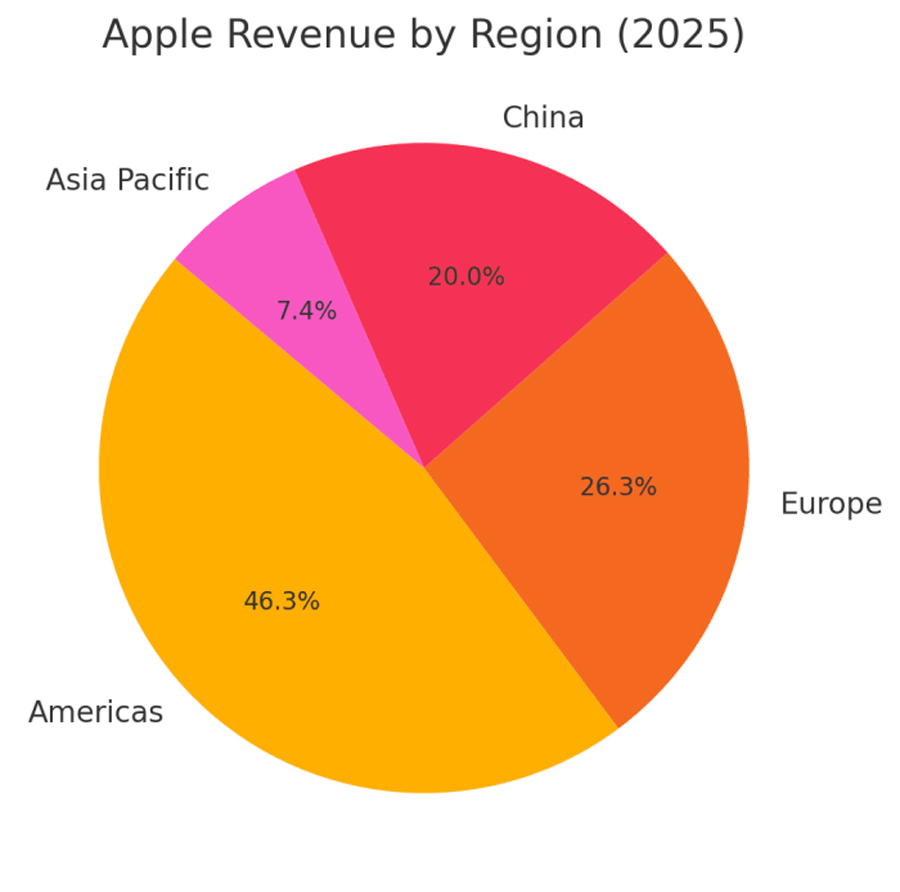

Regional Market Highlights

- The Americas lead Apple’s revenue distribution with a dominant 46.3% share, highlighting the region as the company’s largest and most profitable market.

- Europe follows with 26.3%, underscoring Apple’s strong presence in developed markets such as the UK, Germany, and France.

- China accounts for 20.0% of Apple’s total revenue, reflecting its strategic importance as both a consumer hub and production base.

- The Asia Pacific region contributes 7.4%, representing emerging markets with potential for future growth.

- Combined, the Americas and Europe make up over 72% of Apple’s 2025 revenue, emphasising the company’s continued strength in Western markets.

Software & iOS Version Adoption

- As of August 2025, iOS 18 held 68.7% of all iPhones worldwide by version share.

- By late October 2025, the combined usage share of newer versions (iOS 26 / iOS 19) has reached 35.39%.

- Over 80% of iPhone and iPad users update to the latest release within the first few months.

- Devices introduced in the last four years show 88% running iOS 18 as of mid‑2025.

- Support changes, iOS 26 drops feature‑update support for models such as the iPhone XS, XS Max, and XR.

- Rapid adoption of new versions provides app developers a uniform baseline, reducing fragmentation risk relative to Android.

- Enterprise deployments benefit from high iOS version adoption, and fewer legacy versions increase security and feature uniformity.

- Feature upgrades such as Apple Intelligence and system‑wide enhancements are key motivators for users to update.

- High adoption also favors services monetisation since users are on recent OS versions.

- For global device‑fleet management, iOS version maturity simplifies app support and reduces development cost.

Environmental Impact and Recycling Statistics

- According to Apple Inc. In the Environmental Progress Report (2025), the company has cut overall greenhouse‑gas emissions by over 60% since 2015.

- 24% of materials shipped in Apple products in 2024 were from recycled or renewable sources.

- The iPhone 17 Pro Max achieved a 67% reduction in carbon footprint (compared to a prior model) by switching back to aluminium from titanium.

- For the iPhone 17 manufacturing line, 35% of the manufacturing electricity was sourced from renewable energy.

- Apple’s “Zero Waste Programme” has diverted 3.6 million tonnes of supplier facility waste from landfills.

- 99% of cobalt used in Apple‑designed batteries is now sourced from recycled material.

- Apple’s suppliers’ Clean Energy Programme avoided 21.8 million tonnes CO₂e emissions in 2024.

- Challenges remain; only an estimated 4.7 million iPhones were recycled out of tens of millions scrapped in a given year.

- Apple aims for a carbon‑neutral product lifecycle by 2030, meaning manufacturing, use‑phase, and end‑of‑life will be fully accounted for.

- For consumers, trade‑in programmes, extended use cycles, and certified recycling help reduce individual device environmental impact, relevant when comparing upgrade strategies.

Market Challenges & Competitive Landscape

- The global smartphone market grew only 3% YoY in Q3 2025 (≈ 320.1 million units shipped).

- Though Apple grew 4% in that quarter, the modest growth highlights a saturated market and intense competition.

- Premium handset competition remains fierce, rivals such as Samsung, Xiaomi, and others push aggressive value propositions in emerging markets.

- Supply‑chain headwinds, tariffs, and rising component costs exert pressure on margins, particularly for premium devices.

- In some markets, Android brands remain highly competitive in price tiers relevant to Apple’s expansion ambitions, especially outside the U.S./Europe.

- Regulation risk, the App Store model is under scrutiny (e.g., EU antitrust scrutiny), which could affect software and services revenue streams.

- Slowing upgrade cycles and longer device lifespans (especially in mature markets) reduce unit growth potential for new iPhones.

- Currency fluctuations and regional cost differences risk making flagship pricing less viable in key markets without adaptation.

- Maintaining growth will increasingly depend on services, ecosystem lock‑in, and emerging market penetration rather than sheer unit volume.

- Strategic responses, manufacturer innovation (foldables, AR), financing/partner offers, and local manufacturing are becoming critical rather than purely hardware differentiation.

Frequently Asked Questions (FAQs)

1.561 billion users.

27.93% of the global smartphone OS market.

19% of shipments, with 55 million units shipped.

58.03% of the U.S. smartphone market is iOS.

15.82% of all active iPhones were iPhone 13 models.

Conclusion

The landscape for the iPhone remains one of strength, nuance, and strategic complexity. From the dominant role of the App Store in global digital commerce to premium pricing trends, high software‑version adoption, and notable environmental strides, the ecosystem continues to evolve. Yet, the challenges are real: slower unit growth, intense competition, and regulatory headwinds demand adaptive strategies.

For businesses, consumers, and analysts alike, the key takeaway is clear: it’s no longer just about selling devices, it’s about sustaining the ecosystem. Dive into the full article to explore each of these statistics and their implications in depth.