Antivirus software remains one of the most widely used cybersecurity tools for protecting devices, networks, and sensitive data from malware, ransomware, phishing attacks, and other digital threats. Businesses rely on antivirus solutions to secure employee endpoints, while consumers use them to protect online banking, shopping, and personal information. As cybercriminals adopt AI-driven attack methods and target both mobile and desktop devices, antivirus technology continues to evolve. The statistics below highlight the latest trends, market growth, adoption rates, and industry developments shaping the antivirus landscape.

Editor’s Choice

- 66% of U.S. adults used antivirus software in 2025, while 34% operated without antivirus protection.

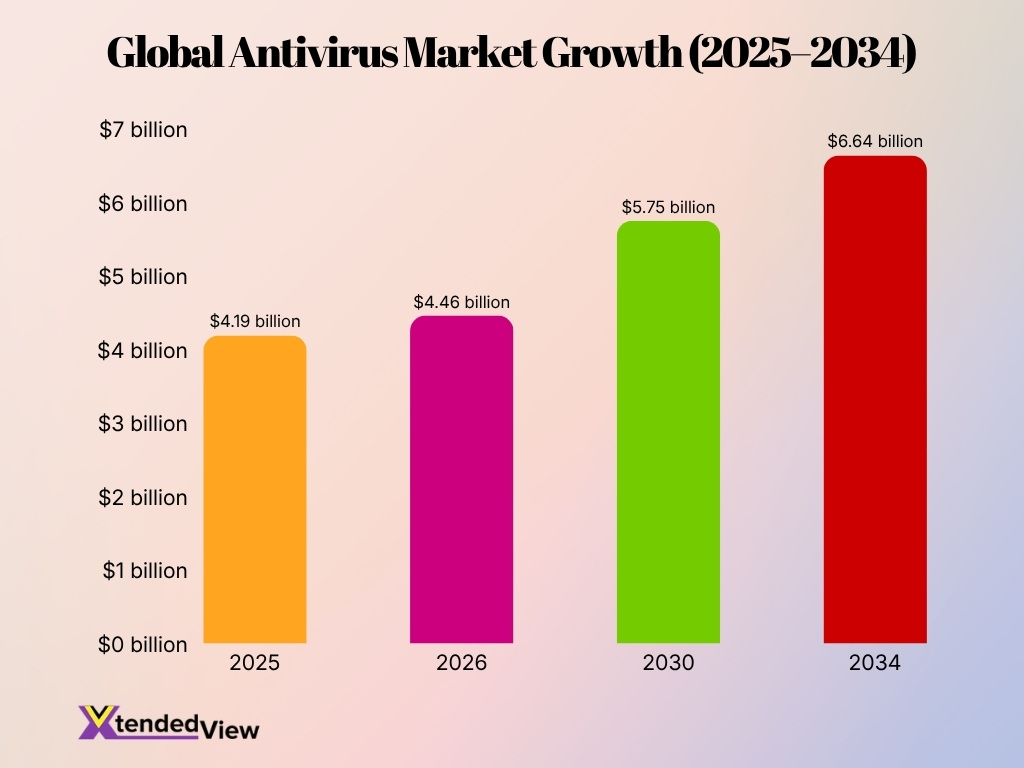

- The global antivirus software market reached approximately $4.46 billion in 2026, up from $4.19 billion in 2025.

- The antivirus software market is projected to surpass $5.75 billion by 2030.

- More than 282,000 new malware samples are detected daily worldwide.

- The global endpoint security market is expected to grow from $27.46 billion in 2025 to $38.28 billion by 2030.

- Only 18% of smartphone users pay for third-party antivirus protection on mobile devices.

- North America accounted for roughly 48% of the global antivirus software package market in 2025.

- Gen Digital projected fiscal 2026 revenue between $4.7 billion and $4.8 billion, reflecting strong cybersecurity demand.

Recent Developments

- AI-powered threat detection has become a major product focus across leading antivirus vendors in 2025 and 2026.

- Security providers increasingly integrate antivirus, VPNs, password managers, and identity monitoring into a single subscription package.

- Gen Digital forecasted up to $4.8 billion in fiscal 2026 revenue due to strong demand for cybersecurity products.

- Businesses continue increasing cybersecurity budgets as AI-assisted cyberattacks become more sophisticated.

- Cloud-based endpoint protection adoption accelerated due to remote and hybrid work environments.

- Antivirus vendors increasingly emphasize ransomware protection and identity theft prevention as core features.

- Market forecasts show antivirus software revenue continuing to grow through 2030 and beyond despite the rise of integrated security suites.

- Mobile security remains underpenetrated, creating a major opportunity for vendors targeting smartphone users.

- Advanced machine learning models now help antivirus products detect zero-day threats more effectively than signature-only methods.

General Antivirus Statistics

- Approximately two-thirds of Americans (66%) actively use antivirus software.

- About 34% of U.S. adults still operate devices without antivirus protection.

- Among antivirus users, 41% use protection exclusively on personal devices.

- Another 25% use antivirus software on both business and personal devices.

- Security researchers detect roughly 282,000 new malware programs every day.

- More than 1 trillion malware instances are estimated to exist across the internet ecosystem.

- Roughly 95% of cyberattacks have financial motives, making malware protection a critical business requirement.

- Antivirus adoption remains relatively stable year over year, despite growing cyber threats.

- Many users now rely on built-in security solutions instead of standalone antivirus products.

Global Antivirus Market Size and Revenue

- The global antivirus software market reached approximately $4.19 billion in 2025.

- Market revenue is expected to increase to $4.46 billion in 2026.

- Industry forecasts project the market value of $5.75 billion by 2030.

- Another forecast estimates antivirus software revenue at $4.88 billion in 2026.

- Long-term projections suggest the market could exceed $6.64 billion by 2034.

- One market analysis valued the antivirus industry at $4.72 billion in 2025.

- Forecast models indicate a CAGR of approximately 6% between 2026 and 2034.

- Some analysts project antivirus software spending to surpass $8.45 billion by 2034.

- North America remains the largest contributor to antivirus software revenue globally.

Global Antivirus Adoption Statistics

- 66% of U.S. adults used antivirus software in 2025.

- Around 54% of users globally rely on built-in protection or default security tools rather than dedicated antivirus products.

- Only 18% of mobile users purchase third-party antivirus solutions.

- Approximately 14% of smartphone users report having no cybersecurity protection tools installed.

- About 16% of smartphone users cannot identify what security software protects their devices.

- Paid antivirus adoption on desktop and laptop computers increased to 41% among surveyed users.

- Antivirus adoption remains strongest among users who conduct online banking and financial transactions regularly.

- Remote work expansion continues to drive enterprise endpoint security deployments.

- Organizations increasingly deploy antivirus alongside broader endpoint protection platforms rather than as standalone products.

Free vs. Paid Antivirus Software Statistics

- Free antivirus usage recently surged to 61%, while paid software subscriptions dropped to 36%.

- The paid antivirus segment still dominates global industry revenue with a massive 62.9% market share.

- Around 63% of PC owners currently rely on real-time antivirus software, a steep decline from 83% in 2022.

- Only 1 in 4 smartphone users currently choose to install dedicated mobile antivirus protection on their devices.

- A significant 77% of the total market share belongs to traditional desktop antivirus software installations.

- Just 25% of active consumers rate their current antivirus security solutions as being very effective.

- Roughly 63% of internet users believe that safe browsing habits protect them better than antivirus software.

- Antivirus software adoption among users aged 60 and older sits at 73%, compared to just 51% for ages 18 to 29.

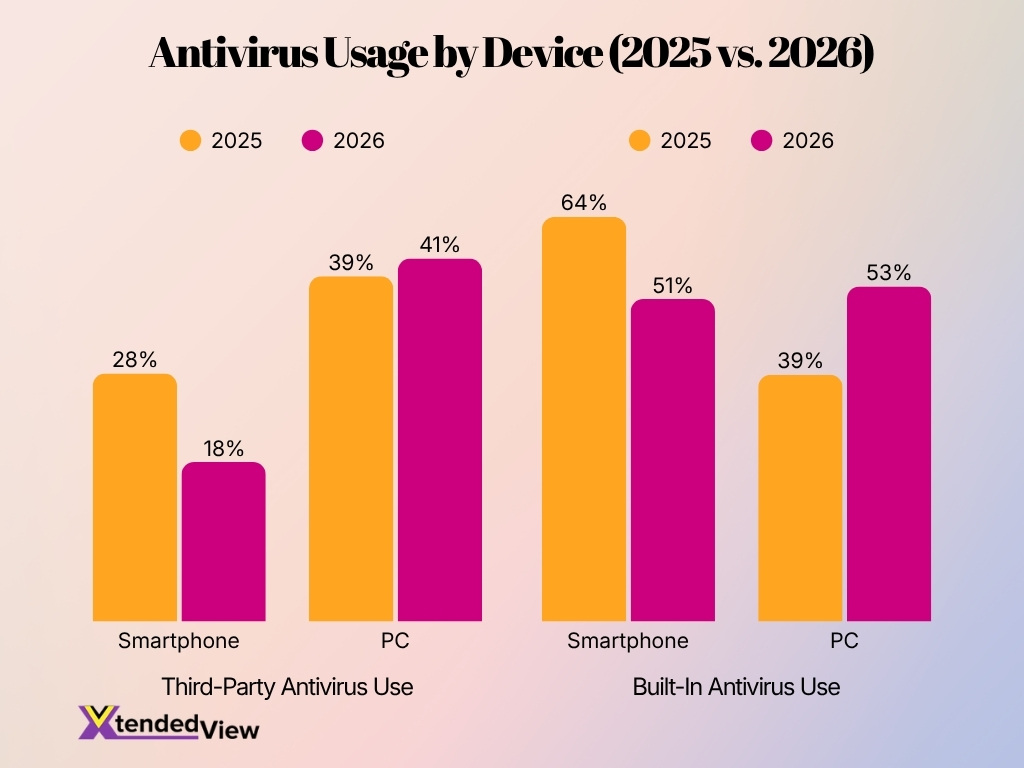

Antivirus Usage Trends by Device (2025 vs. 2026)

- Smartphone third-party antivirus usage declined from 28% in 2025 to 18% in 2026, indicating lower reliance on external security apps.

- PC third-party antivirus adoption increased slightly from 39% to 41%, showing continued demand for dedicated antivirus solutions.

- Smartphone built-in antivirus usage dropped from 64% in 2025 to 51% in 2026, a decrease of 13 percentage points.

- PC built-in antivirus usage rose significantly from 39% to 53%, making it the fastest-growing antivirus category.

- Built-in antivirus protection remained more popular than third-party antivirus software across both smartphones and PCs in 2026.

- PC users showed stronger antivirus adoption overall in 2026, with both third-party (41%) and built-in (53%) usage increasing.

- Smartphone antivirus usage declined across both categories, with the sharpest drop seen in third-party solutions (-10 percentage points).

- Built-in PC antivirus tools surpassed third-party PC antivirus software in 2026, reaching 53% compared to 41%.

Antivirus Adoption by Operating System

- Windows commands over 71% of the global desktop operating system market share.

- Microsoft Defender actively protects hundreds of millions of active devices globally.

- More than 84% of desktop computer users report having antivirus software installed.

- Mac-specific malware threats experienced significant growth throughout 2024 and 2025.

- Approximately 78% of macOS users currently rely on dedicated antivirus protection.

- Android accounts for roughly 72% of the global mobile operating system market.

- Over 90% of discovered mobile banking trojans specifically target Android devices.

- Nearly 68% of smartphone users utilize some form of mobile antivirus security.

- The global enterprise antivirus market is projected to reach $9.0 billion by 2033.

Consumer vs. Enterprise Antivirus Statistics

- The global endpoint security market is expected to grow from $27.46 billion in 2025 to approximately $38.28 billion by 2030.

- Enterprise organizations account for the vast majority of the market, representing over 70% of total cybersecurity spending worldwide.

- More than 90% of enterprises actively deploy centralized endpoint protection solutions across all of their employee devices.

- Over 50% of small and medium-sized businesses continue increasing antivirus spending as ransomware attacks become more frequent.

- Consumer antivirus adoption in the U.S. currently stands at approximately 66% of the adult internet user population.

- Nearly 75% of enterprise security solutions increasingly include endpoint detection and response (EDR) capabilities alongside traditional features.

- The global consumer antivirus software market was recently valued at $4.79 billion and is anticipated to reach $6.97 billion by 2032.

- Over 36% of paid consumer antivirus subscriptions frequently bundle additional tools like VPNs, password managers, and identity theft services.

- Approximately 85% of organizations plan to increase enterprise cybersecurity budgets throughout 2025 to combat AI-assisted cyber threats.

- The services segment covering managed detection and response is projected to achieve a 55% share within large enterprises by 2035.

Key Reasons for Using Antivirus Software

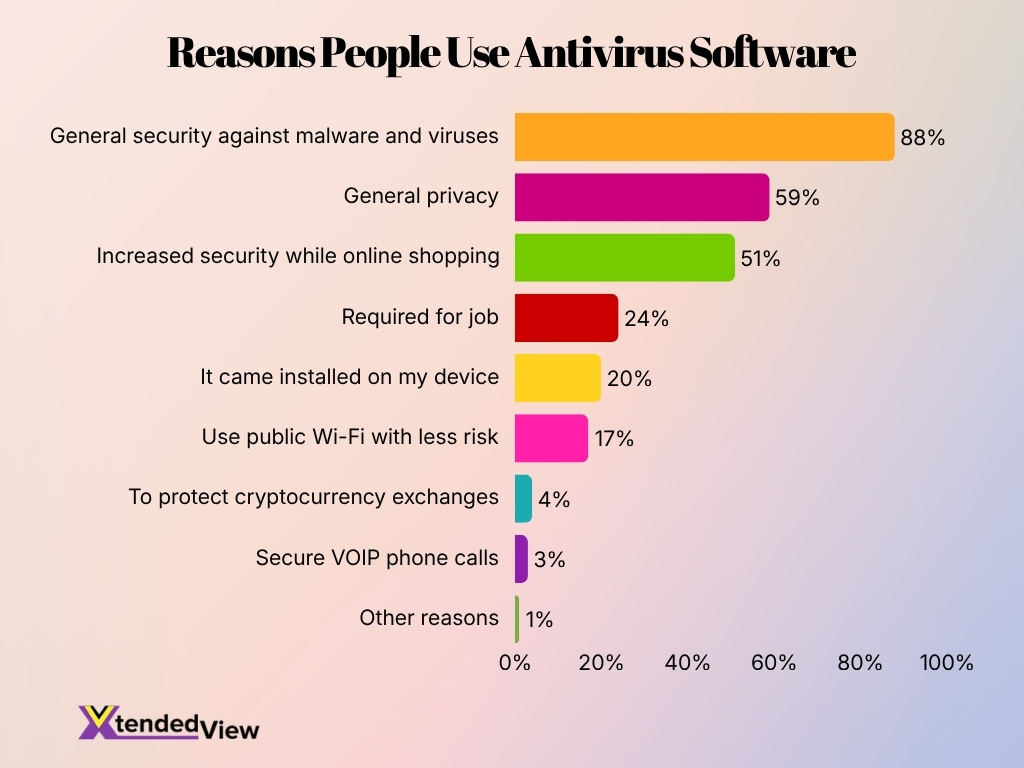

- 88% of users rely on antivirus software for protection against malware and viruses, making it the leading reason for adoption.

- 59% of respondents use antivirus tools to enhance their general privacy and data security.

- 51% install antivirus software for safer online shopping and protection against digital threats.

- 24% use antivirus software because it is required for their job or workplace policies.

- 20% continue using antivirus software because it came preinstalled on their device.

- 17% value antivirus protection for safer use of public Wi-Fi networks.

- Only 4% use antivirus software to protect cryptocurrency-related activities and exchanges.

- Just 3% of users rely on antivirus tools to help secure VoIP phone calls.

- A minimal 1% cited other reasons for using antivirus software.

Antivirus Effectiveness and Threat Detection Rates

- Top-tier security solutions consistently achieve a 99.7% detection rate for widespread malware with minimal false positives.

- Advanced behavioral analysis engines deliver a 99.5% detection rate against emerging and unknown zero-day threats.

- Approximately 80% of zero-day vulnerabilities are actively exploited before software vendors can release a protective patch.

- Traditional signature-based antivirus solutions initially detect only 18% of new malware attacks on day zero.

- The detection capability of traditional signature-based methods rises to just 61.7% after 30 days of a new threat.

- Modern cloud sandboxing technologies now analyze and process over 1.2 million malware samples on a daily basis.

- Sophisticated machine learning detection models have successfully reduced the false positive rate to under 0.03%.

- Unpatched zero-day vulnerabilities remain completely undetected for an average of 312 days before public disclosure.

- The average operational gap between discovering a zero-day vulnerability and releasing a patch is exactly 22 days.

- Zero-day exploits are actively utilized in over 50% of targeted attacks conducted by advanced persistent threat groups.

Malware Detection and Threat Statistics

- Security trackers identify over 450,000 new malware samples and potentially unwanted applications every day.

- The cumulative volume of known malware instances has officially surpassed 1.56 billion unique files globally.

- Digital environments experienced a staggering 6.06 billion documented malware attacks during a single year.

- Fileless and malware-free techniques now account for 82% of all threat detections in enterprise networks.

- Widespread infostealer malware campaigns recently compromised more than 16 million devices to harvest credentials.

- Mobile-focused banking trojan attacks surged by 56%, fueled by over 255,000 new malicious packages.

- Ransomware remains devastating and is a primary factor in 59% of all financially motivated cyber incidents.

- The emergence of AI-enabled adversaries has driven an 89% increase in sophisticated and automated attacks.

- Trojans dominate the traditional threat landscape by making up 58% of all deployed malware worldwide.

- Malicious email attachments and links consistently serve as the primary vector for 94% of malware delivery.

Top Anti-Virus Market Share Statistics

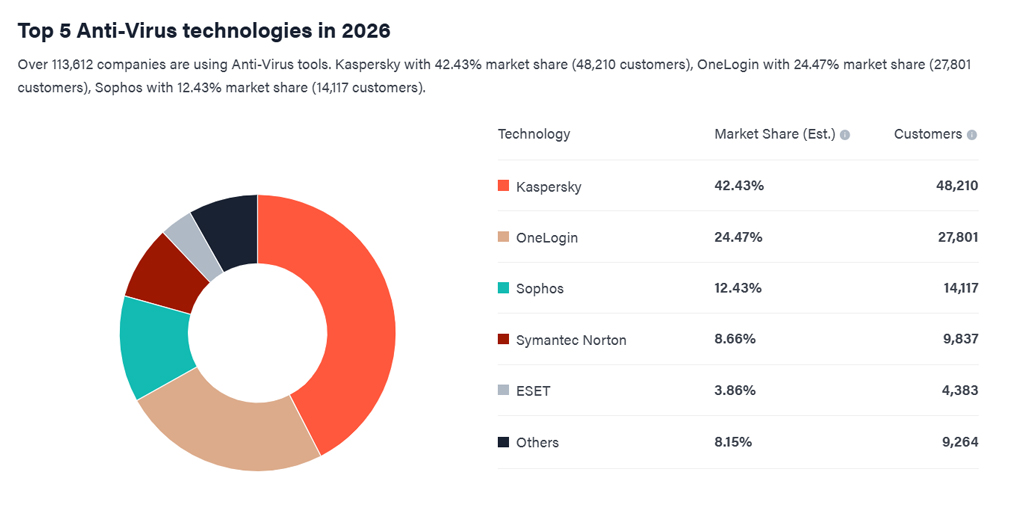

- Kaspersky dominated the anti-virus market with a 42.43% market share and 48,210 customers.

- OneLogin ranked second, capturing 24.47% market share with 27,801 customers.

- Sophos secured 12.43% of the market, serving 14,117 customers worldwide.

- Symantec Norton accounted for 8.66% market share with 9,837 customers using its solutions.

- ESET held a 3.86% market share, supported by 4,383 customers.

- The Others category represented 8.15% market share and 9,264 customers combined.

- More than 113,612 companies were actively using anti-virus technologies in 2026.

- The combined share of Kaspersky, OneLogin, and Sophos reached 79.33%, highlighting strong market concentration.

- Kaspersky’s customer base was 20,409 larger than OneLogin’s, reinforcing its market leadership.

- The top five anti-virus technologies collectively controlled 91.85% of the market in 2026.

Common Cyber Threats Blocked by Antivirus

- Ransomware currently accounts for roughly 14% of all malware attacks globally.

- Phishing schemes are projected to be involved in 42% of all global breaches.

- Trojans dominate the current threat landscape by making up 58% of all malware infections.

- Global spyware detections have recently experienced a massive 51% growth year-over-year.

- Adware continues to represent an overwhelming 62% of all mobile malware detections.

- Financial losses tied to cryptojacking incidents surged to $6.5 million in early 2026.

- Global detections for password stealers and keyloggers saw a massive 59% surge last year.

- Antivirus platforms register over 450,000 new malicious programs every single day.

- Approximately 79% of cyberattacks now utilize fileless, malware-free techniques to evade detection.

- A staggering 94% of all malware is delivered through malicious emails and infected downloads.

Antivirus Statistics by Region and Country

- North America accounted for approximately 48% of the global antivirus software market in 2025.

- The United States holds an overwhelming 85.60% of the total North American antivirus market share.

- Approximately 66% of U.S. adults reported using dedicated antivirus software on their devices in 2025.

- Organizations in the United Kingdom represent 8.55% of the world’s antivirus technology customers.

- The Asia-Pacific region is projected to see the fastest antivirus market growth, maintaining a 6% CAGR through 2034.

- Brazil currently accounts for 15.84% of global antivirus software users, dominating the Latin American region.

- Around 84% of global consumers actively maintained security software on their personal computers in 2025.

- Barely 25% of global smartphone owners utilized mobile antivirus protection in 2025.

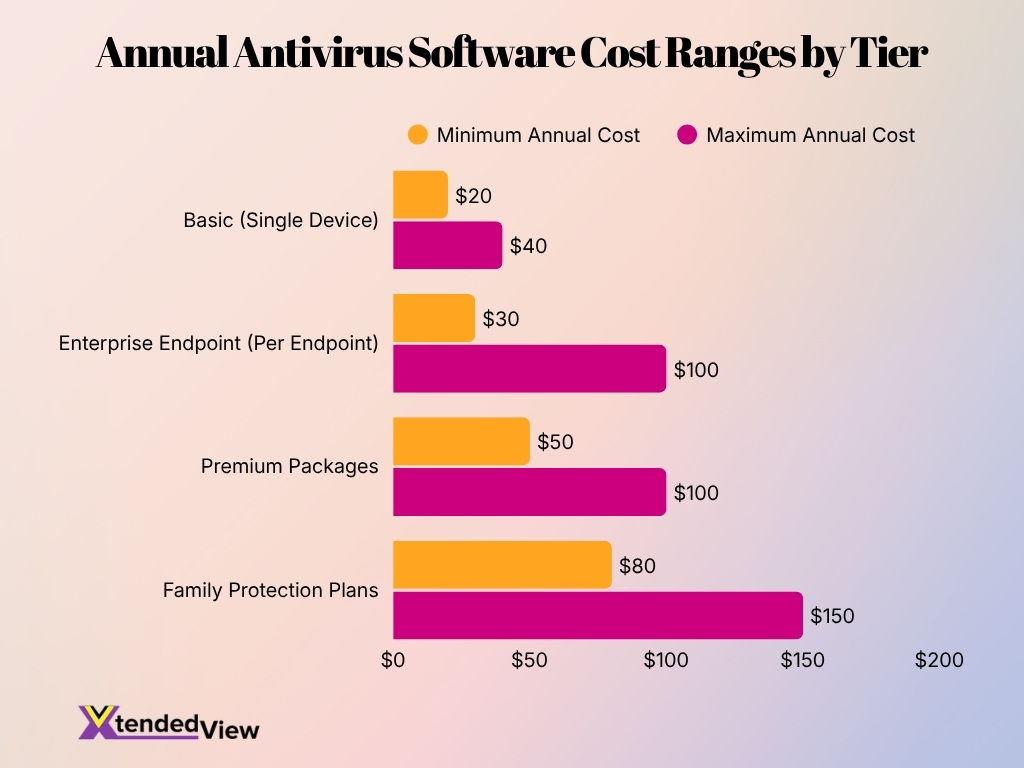

Average Cost of Antivirus Software

- Basic antivirus subscriptions typically cost between $20 and $40 per year for a single device.

- Premium antivirus packages generally range from $50 to $100 annually, depending on features and device limits.

- Family protection plans covering multiple devices often cost between $80 and $150 per year.

- Enterprise endpoint security licenses commonly range from $30 to $100 per endpoint annually.

- Cloud-managed enterprise security platforms can exceed $150 per endpoint per year when advanced threat detection is included.

- Antivirus products bundled with VPNs and identity monitoring services command higher subscription prices than standalone antivirus tools.

- Many providers offer introductory discounts of 30% to 60% during the first subscription year.

- Organizations increasingly choose subscription-based security models instead of perpetual software licenses.

- Multi-device packages continue gaining popularity because they provide lower per-device costs.

- Security spending continues to increase as businesses seek protection against ransomware and AI-powered threats.

Cloud-Based vs. Traditional Antivirus Solutions

- Over 60% of organizations utilize cloud-delivered services for endpoint protection.

- Cloud platforms distribute real-time threat updates globally in under 5 minutes.

- Transitioning to cloud-native antivirus reduces IT maintenance costs by 20%.

- Traditional antivirus consumes up to 15% more system resources than cloud agents.

- Nearly 80% of cloud security platforms integrate AI and machine learning.

- Businesses using cloud-managed endpoints report 30% faster incident response times.

- More than 70% of companies accelerated cloud antivirus adoption for remote work.

- Cloud solutions detect zero-day threats up to 40% faster than local signature databases.

Frequency of Antivirus Scans and Updates

- Over 80% of modern antivirus programs update their threat intelligence databases up to 6 to 8 times daily.

- Leading vendors typically deliver emergency malware signatures within 2 to 4 hours of identifying major threats.

- Around 95% of commercial antivirus solutions currently utilize real-time scanning over traditional manual models.

- More than 90% of consumer antivirus installations retain automatic updates enabled by default.

- Approximately 75% of consumer security software configures weekly full-system scans as the standard default setting.

- Nearly 85% of enterprise endpoint platforms now prioritize continuous behavioral monitoring over scheduled scanning.

- Close to 70% of organizations handling sensitive data conduct daily endpoint security assessments.

- Cloud-based antivirus systems rapidly process up to 100,000 continuous threat intelligence updates globally each day.

- Devices maintaining regular automated updates experience up to a 60% lower malware infection rate.

- Over 90% of security professionals strictly mandate automatic updates to immediately patch zero-day vulnerabilities.

Key Reasons for Avoiding Antivirus Protection

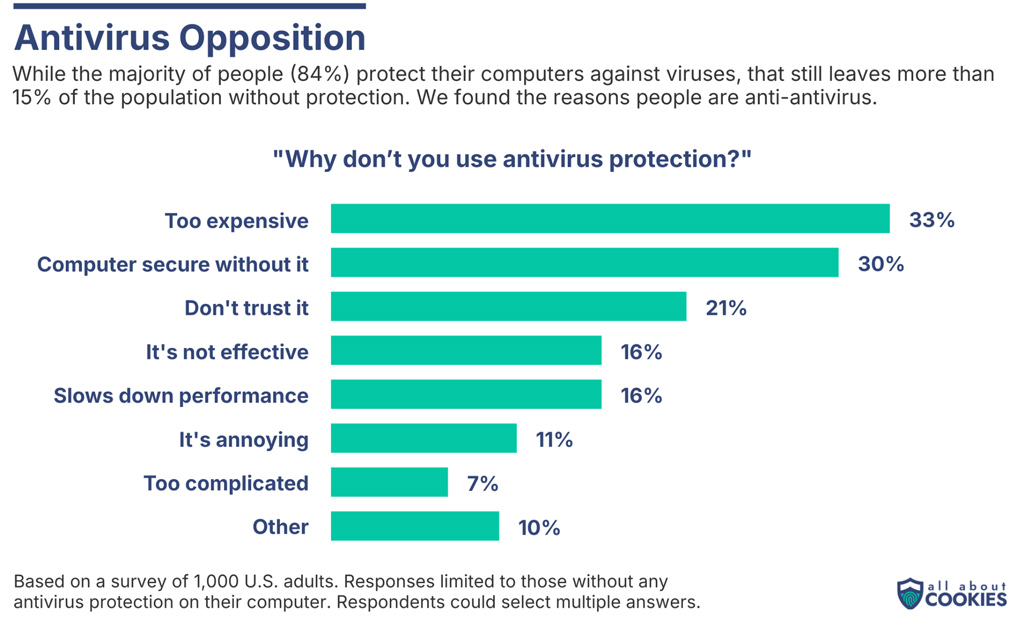

- 33% of non-users say antivirus software is too expensive, making cost the leading barrier to adoption.

- 30% believe their computer is secure without antivirus software, showing strong confidence in existing security measures.

- 21% avoid antivirus software because they do not trust it, highlighting ongoing skepticism toward security software.

- 16% think antivirus software is ineffective, suggesting doubts about its ability to prevent cyber threats.

- 16% report antivirus software slows down performance, making system speed a major concern.

- 11% consider antivirus software annoying, indicating usability and interruption issues.

- 10% selected other reasons, reflecting a variety of additional concerns not captured in the survey.

- Only 7% say antivirus is too complicated, making complexity the least cited reason for non-adoption.

- Despite concerns, 84% of people still use antivirus protection, leaving roughly 16% unprotected.

- Cost, trust, and perceived security account for the top three reasons people choose not to install antivirus software.

Future Trends and Antivirus Industry Projections

- The global antivirus software market is projected to reach $8.45 billion by 2034.

- Utilizing AI-driven security tools reduces organizational breach detection timelines by 108 days.

- The antivirus software industry is anticipated to expand at a CAGR of 7.4% through 2033.

- Approximately 169 million American adults currently utilize antivirus software for device protection.

- The adoption of free antivirus software increased significantly to capture 61% of the market in 2025.

- Connected IoT devices requiring robust security measures are projected to reach 39 billion by 2030.

- Demographic data shows users aged 60 and older have the highest PC antivirus adoption at 73%.

- Microsoft Defender maintained market dominance in 2025 with a leading 23% market share.

Frequently Asked Questions (FAQs)

Approximately 66% of U.S. adults use antivirus software, representing about 121 million Americans.

The global antivirus software market was valued at approximately $4.72 billion in 2025 and is projected to exceed $8.45 billion by 2035.

Only 18% of smartphone users pay for third-party antivirus software, while 14% use no cybersecurity tools at all.

The antivirus software market is forecast to expand at a 6% CAGR between 2026 and 2035.

North America held approximately 48.0% of the global antivirus software market share in 2025, making it the leading regional market.

Conclusion

Antivirus software remains a critical component of modern cybersecurity despite the rapid evolution of cyber threats. The data shows that both consumers and businesses continue investing in antivirus and endpoint protection technologies as ransomware, phishing, infostealers, and AI-assisted attacks become more sophisticated. While cloud-based security, behavioral analytics, and AI-powered detection are reshaping the industry, traditional antivirus solutions still play an important role in defending devices and networks.

Looking ahead, market growth, increased enterprise adoption, and continued innovation suggest that antivirus software will remain a foundational cybersecurity technology throughout the remainder of the decade.