The cloud‑gaming space has shifted rapidly into a mature technology, with players and platforms alike embracing streaming models that reduce the need for dedicated hardware. Industries ranging from entertainment to telecom are leveraging cloud gaming to reach users in new ways, for example, telecom providers bundling gaming services with 5G plans, and vehicle manufacturers embedding game streaming into infotainment systems. This article explores the key statistics shaping the future of cloud gaming and reveals what business decision‑makers and gamers need to know.

Editor’s Choice

- The global cloud‑gaming market is projected at USD 3.36 billion in 2025, up from USD 2.27 billion in 2024.

- The forecast CAGR for 2025‑2030 stands at 44.3% in one major study.

- Asia‑Pacific held over 47.9% of the market share in 2024.

- More than 53% of cloud‑gaming users in 2024 were classified as casual gamers.

- Video‑streaming‑based delivery captured about 54.8% of the technology share in 2024.

- Smartphones managed roughly 40.2% of device‑type share in 2024.

- AI, edge computing and new monetization models are identified as major growth drivers in 2025.

Recent Developments

- In 2025, the article “The Biggest Cloud Gaming Trends of 2025” noted that the global market is on track to surpass US$10 billion in the coming years.

- Several platforms upgraded their infrastructure; for example, one service rolled out support for 4 K/120 fps streaming and expanded its game library in 2025.

- Monetization models are diversifying, alongside subscriptions, pay‑as‑you‑go streaming and ad‑supported access are gaining traction.

- The rollout of 5G and improved broadband has accelerated the availability of low‑latency cloud‑gaming sessions in more markets.

- Smart‑TV manufacturers are increasingly integrating cloud‑gaming apps natively, reducing dependency on consoles.

- Edge computing and AI are being used to optimize streaming workloads and latency for cloud gaming platforms in 2025.

- More partnerships between game publishers and cloud platforms are forming to launch “game streaming first” titles in 2025.

- The trend of offering cloud gaming in non‑traditional venues (cars, smart TVs, public kiosks) is gaining early adoption in 2025.

Global Cloud Gaming Market Overview

- One major research firm estimates the market at USD 2.7059 billion in 2024, with a projection to reach USD 77.7119 billion by 2033, at a CAGR of 39.9% from 2025 to 2033.

- Another source puts the 2025 market size at USD 3.36 billion and forecasts USD 21.04 billion by 2030.

- A further estimate shows 2024 = USD 13.65 billion, 2025 = USD 19.29 billion (CAGR ~41.3%).

- Region‑wise, Asia‑Pacific held approximately 47.9% of the market in 2024.

- The market is segmented by streaming type, device type, gamer type and region, showing diversified growth across segments.

- Supply‑chain factors (data‑centres, edge servers, latency reduction) are increasingly key to market expansion globally.

- Forecasts vary widely, reflecting differing methodologies and definitions of “cloud gaming” across reports.

- The global market is still relatively small compared to the broader gaming industry, but it is one of the fastest‑growing sub‑segments.

Key Market Growth Drivers

- The expansion of high‑speed internet and 5G networks lowers the barrier to entry for cloud gaming.

- Increasing smartphone and smart‑device penetration in emerging markets enables access to cloud gaming without expensive consoles.

- The shift from hardware ownership to subscription/streaming models appeals to cost‑sensitive consumers.

- Developers and publishers are partnering with cloud platforms to deliver “play anywhere” experiences, expanding reach.

- Device fragmentation (consoles, smart TVs, PCs, mobiles) encourages cloud delivery to simplify user experiences.

- Advances in edge computing and AI‑driven stream optimisation reduce latency and improve quality of experience.

- Monetisation innovations (hourly‑pay, ad‑supported tiers, bundled services) attract new user segments.

- Global expansion of platform availability (new markets, languages, devices) enlarges total addressable market.

Cloud Gaming Market Size and Forecast

- As noted, the market is projected to reach USD 21.04 billion by 2030, growing from USD 3.36 billion in 2025.

- One estimate shows growth from USD 2.7059 billion in 2024 to USD 77.7119 billion by 2033.

- A separate forecast suggests the market will hit USD 11.1 billion in 2025 (from USD 7.0 billion in 2024) with a ~46.9% CAGR.

- Another forecast estimates USD 96.67 billion by 2034, with a CAGR of ~45.5% from 2025.

- Yet another view places 2025 = US $5.6 billion and 2034 = US $33.27 billion (indicative of variance in research).

- The wide divergence in forecast values underscores differences in definition (consumer vs enterprise use), geographic scope, and segmentation.

- For U.S.‑centric purposes, estimates suggest single‐digit billions by 2025, with rapid escalation post‑2026 as infrastructure improves.

- Businesses should interpret forecast figures as directional rather than exact, and focus on underlying growth drivers and market segments.

Cloud Gaming User Statistics

- The global user base for cloud gaming is forecast to reach ~501 million users by 2029.

- In 2023, the penetration rate for cloud gaming among internet users globally was around 3.8%, and expected to rise to ~5.1% in 2024.

- In 2020 the estimated number of cloud gaming users was ~62.5 million with ~0.8% penetration rate, by 2021 that rose to ~102.6 million and ~1.4% penetration.

- The average gamer spends 8.6 hours per week playing games in 2025, and cross‑platform users show ~31% higher daily return rates.

- Among gamers in Gen Z/Millennials, the average weekly play time is ~10.3 hours in 2025.

- Smartphones are becoming more widely used for cloud gaming, especially in emerging markets, helping drive user growth.

- In the U.S., the number of cloud‑gaming consumers is projected to hit ~87.2 million by 2028.

- Latency improvements, Key regions like the U.S. and Western Europe have seen cloud‑gaming latency drop to below ~40 ms.

- Many cloud gaming users engage in sessions on non‑console devices – e.g., smart TVs or PCs – signalling a shift away from hardware‑bound gaming.

- Casual gamers account for the largest share of cloud‑gaming users, given the ease of access and minimal hardware requirements.

Cloud Gaming Revenue Statistics

- Global cloud gaming revenue is estimated at ~USD 6.91 billion in 2024.

- One forecast puts the global cloud‑gaming market size at USD 9.32 billion by 2025.

- In 2025, the global cloud‑gaming market is expected to be ~USD 19.29 billion under one scenario.

- According to another source, the value stood at USD 2.27 billion in 2024 and will grow at ~44.3% CAGR from 2025‑2030.

- By 2029, predictions place cloud‑gaming revenue at ~USD 25.30 billion.

- In the U.S., cloud‑gaming revenue is expected to hit ~USD 2.38 billion by 2024.

- Cloud gaming still accounts for less than 5% of total video‑game industry revenue in 2025.

- The video‑streaming type segment within cloud gaming captured over 54% of market share in 2024.

- From one source, file‑streaming segment revenue in 2024 was ~USD 1,226.8 million and is expected to reach ~USD 10,939.7 million by 2030.

- The global cloud‑gaming market value is estimated at USD 9.71 billion in 2024 and projected to reach USD 15.74 billion in 2025.

Cloud Gaming by Streaming Type (Video vs File)

- The video‑streaming delivery type held a market share of over 54% in 2024.

- The file‑streaming segment (i.e., streaming by downloading chunks rather than live video) generated ~USD 1,226.8 million in revenue in 2024.

- The file‑streaming type is forecasted to reach ~USD 10,939.7 million by 2030.

- In 2025, the video streaming segment was projected to contribute ~58.8% of the market, according to a report.

- The adoption of file‑streaming is rising faster than video‑streaming, due in part to lower latency and more flexible download/render models.

- The dominance of video‑streaming delivery reflects user preference for immediate play without installation, benefiting cloud services.

- Many cloud gaming services now support both live video streaming and file streaming approaches, depending on device and network context.

- The streaming type affects infrastructure demands; video streaming requires continuous high bandwidth, while file streaming can reduce streaming load via local caching and chunk delivery.

- Analysts note that the clear majority of early cloud‑gaming revenues come from video‑streaming rather than file‑streaming models.

- As networks improve and devices diversify, the gap between video vs file streaming business models may narrow over the next 3‑5 years.

Cloud Gaming by Device (Smartphones, PCs, Consoles, Smart TVs, Tablets)

- According to one forecast, the smartphone segment is estimated to hold ~37.7% of market share in 2025.

- In another source, smartphones made up ~44.12% of the market size in 2024.

- PCs & laptops are expected to dominate with ~20.7% share by 2032 in one report.

- Smart TVs are emerging as a growth device for cloud gaming because they remove the need for a console.

- Tablets and hybrid devices contribute modestly but show higher growth rates in regions where consoles are less common.

- Device‑type fragmentation means cloud‑gaming providers must support multiple input types, controllers, keyboard/mouse, touch, and remote.

- Consoles remain relevant for cloud gaming access, especially as many services allow console streaming without the purchase of new hardware.

- In one study, device reach on cloud gaming showed smart TVs and Windows PC usage rising significantly relative to mobile in some platforms.

- The growth of smartphone and smart‑TV cloud gaming is especially strong in emerging markets due to lower entry cost (no console required).

- Device diversity also impacts latency and user experience; mobile networks may struggle more than cable/fiber to deliver consistent curves.

Cloud Gaming by Gamer Type (Casual, Avid, Hardcore)

- The casual gamer segment in cloud gaming was estimated to contribute the highest market share at 77.8% in 2025.

- The casual segment’s lead is attributed to lower hardware requirements and ease of access via smartphones or smart TVs.

- The avid/core gamers (often defined as more committed than casual) form the next tier, yet their share remains significantly lower than casual.

- Professional or hardcore gamers (competitive, high‑performance titles) have the smallest share, due largely to latency and quality requirements.

- Some reports indicate that casual gamers drive the highest growth in cloud gaming uptake because they prioritize convenience over performance.

- Hardcore gamers are more sensitive to lag, input delay, and streaming fidelity, which limits immediate cloud adoption among this group.

- Cloud gaming services are tailoring offerings: e.g., casual‑friendly titles, simpler control schemes, and multi‑device support to capture casual and avid segments.

- The growth of cloud gaming among casual players suggests a shift in the typical gamer profile, from console‑centric to multi‑device streaming access.

Regional Analysis of Cloud Gaming Market

- The global cloud gaming market shows significant regional variation in size, growth rate, and user adoption.

- The Asia‑Pacific region accounted for the largest market share globally in 2024, reflecting strong mobile and broadband penetration.

- North America is expected to dominate the cloud gaming market in 2025 in terms of revenue share.

- Europe is growing rapidly, though it still trails APAC in overall size; however, its infrastructure and disposable income suggest strong potential.

- Emerging markets such as Latin America, the Middle East & Africa present smaller current markets but high growth prospects due to improving connectivity.

- Device and network infrastructure discrepancies across regions heavily influence cloud gaming adoption and experience quality.

- Regulatory, data‑sovereignty, and content‑licensing frameworks differ by region, affecting speed and breadth of cloud gaming rollout.

- For companies planning market entry, understanding device usage, network latency, service model, and gust preference by region is critical.

North America Cloud Gaming Statistics

- The North American cloud gaming market generated a revenue of USD 348.4 million in 2023.

- It is expected to grow at a compound annual growth rate (CAGR) of 44.1% from 2024 to 2030.

- In the U.S., the market size was estimated at USD 303.8 million in 2023 and projected to reach USD 447.1 million in 2024.

- The U.S. cloud gaming market is expected to reach about USD 3,887.8 million by 2030, with a CAGR of approximately 42.7% from 2025 to 2030.

- North America is expected to hold a market share of about 47.8% in 2025, making it the leading region for cloud gaming revenue.

- Video‑streaming remains the largest revenue‑generating segment in North America’s cloud gaming market.

- Canada is expected to register one of the highest CAGRs in North America from 2024 to 2030.

- Strong infrastructure (broadband / 5G) and high device penetration contribute to North America’s leading position in cloud gaming adoption.

Europe Cloud Gaming Statistics

- The European cloud gaming market is projected to reach approximately USD 4,296.6 million by 2030, with a CAGR of about 43.7% for 2025‑30.

- By 2025, the EMEA region is predicted to generate cloud gaming revenue of ~USD 2.75 billion.

- The same source estimates that by 2029, the EMEA region will have around 94.7 million cloud gaming users with a penetration rate rising from ~3.5% in 2025 to ~3.6% in 2029.

- Country‑level user penetration in Europe: Norway ~22.7%, Finland ~21.4%, Ireland ~22.2%.

- In the U.K., penetration is ~11.6%, and in France, ~9.1% for cloud‑gaming adoption.

- The European market remains behind Asia‑Pacific in size but offers high growth potential due to strong infrastructure and high disposable income.

- Many European consumers access cloud gaming via smart TVs and PCs rather than consoles, due to licensing and cost structures in the region.

- The latency benchmarks in Western Europe for cloud streaming are reported to have dropped below ~40 ms in key urban markets in 2025.

- Regulatory and data‑sovereignty issues in Europe (such as GDPR) create unique constraints for cloud gaming operators, affecting rollout speed in some countries.

Asia‑Pacific Cloud Gaming Statistics

- The Asia‑Pacific cloud gaming market generated revenue of USD 1,034.1 million in 2024 and is expected to grow to around USD 9,994.2 million by 2030, with a CAGR of ~45.3%.

- APAC accounted for over 47.9% share of the global cloud gaming market in 2024.

- By 2025, the APAC region is predicted to have ~318.5 million cloud‑gaming users with a user penetration of ~6.7%.

- The average revenue per user (ARPU) in the APAC region is cited at ~USD 14.32.

- Countries like India are expected to register some of the highest CAGRs in the region due to rising smartphone penetration and 5G rollout.

- China is identified as dominating the APAC cloud gaming market by country as of 2024 and is expected to remain so through 2032.

- Infrastructure spend in APAC on cloud services for gaming in 2024 reached ~USD 6.6 billion (over 5% of regional game industry revenue).

- The Southeast Asia sub‑region is smaller but growing; the cloud gaming market in SEA was valued ~USD 121.29 million in 2024 and is projected to reach ~USD 698.22 million by 2030 (CAGR ~23.9%).

- Smartphone‑first markets in APAC leverage cloud gaming to bypass costly console hardware, driving adoption especially among casual gamers.

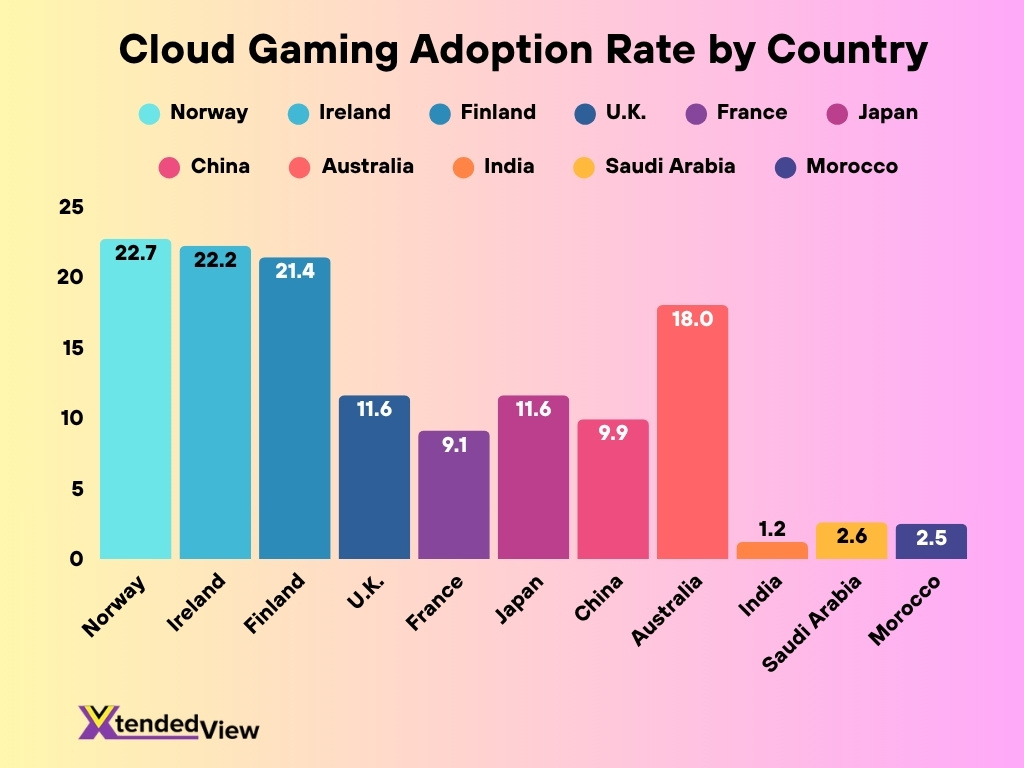

Cloud Gaming Adoption Rates by Country

- In Europe, certain countries show high cloud‑gaming adoption: Norway ~22.7%, Ireland ~22.2%, Finland ~21.4%.

- In the United Kingdom, the adoption rate is ~11.6%, in France, ~9.1%.

- In Asia, Japan is cited at ~11.6% penetration, and China ~9.9%.

- Australia reportedly shows ~18% cloud‑gaming penetration as of 2025.

- India’s rate stands much lower (~1.2%), highlighting market opportunity rather than maturity.

- Several emerging markets, such as Saudi Arabia (~2.6%) and Morocco (~2.5%), indicate early‑stage adoption.

- The wide variation in country adoption underscores infrastructure, cost, device‑ownership and network latency as key determinants.

- Countries with strong broadband and 5G networks show faster cloud‑gaming uptake, particularly Scandinavian markets.

- For the U.S. and Canada, specific country‑level adoption figures are less clearly reported, though North America is expected to lead the regional share globally.

Popular Cloud Gaming Platforms

- Xbox Cloud Gaming (Microsoft) is a leading global platform, with tens of millions of users streaming monthly.

- GeForce NOW (NVIDIA) supports over 2,000 game titles across devices as of 2025.

- Amazon Luna (Amazon) is available in 14+ countries as of 2025 and continues to expand its cloud game streaming service.

- PlayStation Plus Cloud Streaming (Sony) is part of the broader PlayStation ecosystem and contributes to cloud gaming adoption.

- Other platforms, such as Boosteroid, have emerged offering browser or TV streaming of PC games in certain regions.

- Many platforms now support smart TVs, smartphones, and PCs, enabling device‑agnostic game streaming.

- Subscription‑based access and pay‑as‑you‑go models are increasingly used by these platforms to attract casual cloud gamers.

- Partnerships between platforms and telecom or TV manufacturers (for example, smart TVs with built‑in cloud gaming apps) are boosting distribution.

- Competition among platforms is intensifying, with major players investing in latency reduction, library expansion, and higher resolution streaming (e.g., 4K/120fps).

Key Players in the Cloud Gaming Market

- Microsoft Corporation, via Xbox Cloud Gaming and its existing console or PC ecosystem, holds a leading position in subscription and streaming.

- NVIDIA Corporation, through the GeForce NOW service and GPU infrastructure, is a major cloud gaming infrastructure player.

- Sony Interactive Entertainment LLC, with PlayStation’s cloud streaming and console integration, remains a key market participant.

- Amazon Web Services, Inc. / Amazon Luna, leveraging AWS infrastructure combined with Amazon’s platform reach, gives it a sizeable cloud gaming footprint.

- Tencent Games is a dominant publisher in the Asia‑Pacific and is active in cloud gaming initiatives and partnerships.

- Ubitus Inc. provides white‑label solutions and cloud infrastructure to publishers and telecom operators.

- Many players are forming strategic alliances combining console or PC providers with global data centres to deliver low‑latency streaming.

- Mergers and acquisitions are notable as companies acquire streaming technology or studios to bolster cloud‑game libraries and exclusives.

- The market remains somewhat fragmented by region, device type, and business model, creating opportunities for niche and regional players.

Challenges and Restraints in Cloud Gaming

- Latency and network bandwidth remain major barriers; many users still experience lag or instability in cloud‑game sessions.

- Internet infrastructure in many emerging markets is insufficient for high‑quality cloud streaming, limiting adoption.

- Device and input support vary widely (smartphone vs console vs smart TV), complicating platform design and user expectations.

- Content licensing and library size constraints persist as platforms rely on third‑party titles with complex global rights.

- Monetization models are difficult to optimize, balancing subscription, ad‑supported, and pay‑as‑you‑go structures.

- Traditional console or PC gaming competition remains strong, as many gamers prefer owning hardware or games rather than streaming.

- Regional regulation and data sovereignty, especially in Europe, impose constraints on server placement and rollout.

- Hardware cost for cloud‑game providers (GPUs, edge servers) is high, meaning margins can be tight until scale is achieved.

- The user experience for cloud gaming must match or exceed local hardware play; until that is reliable, some gamers remain hesitant.

Frequently Asked Questions (FAQs)

USD 3.36 billion.

44.3% CAGR.

47.9% share.

Less than 5% of the industry.

~501 million users, with a penetration of 6.2% among internet users.

Conclusion

The cloud gaming industry is clearly in a rapid growth phase, with regional dynamics, device landscape shifts, and emerging business models all contributing to change. Across Europe and the Asia‑Pacific, adoption rates vary widely, yet strong infrastructure build‑out and rising device penetration promise major expansions ahead. Top platforms and players are racing to capture this opportunity by improving latency, broadening device support, and simplifying access. That said, infrastructure limitations, licensing complexity, and monetization challenges continue to temper adoption in certain markets. For U.S. and global stakeholders alike, cloud gaming represents a meaningful growth vector, but one that still requires execution excellence to fulfill its full potential. Explore the full article for a detailed dive into user stats, revenue breakdown,s and device‑type trends.